META PLATFORMS INC. Forensic Accounting and Red Flags Report

Potential further downgrades signaled for Meta from uncontrolled expense growth, off balance sheet liabilities sky-rocketing, free cashflows to fall to zero, stock buyback at risk.

The following report was generated with the Forensic Accounting Analysis prompt from the professional prompt library on The INFERENTIAL INVESTOR.

Subscribe to access these tools and stock research.

Important Note: The Inferential Investor does not provide financial advice. Any discussions on stock and market views are made from an educational standpoint and to demonstrate techniques and capabilities of AI, are indicative and may be subject to change without notice. No recommendation, either direct or implied is made with regards to the suitability of any stock mentioned for investment. It is recommended to refer to our full disclaimer here and always do your own research, but I welcome you to follow The Inferential Investor as another input into a well rounded investment process.

The $META Q3 Reaction Function

I’ve seen a lot of investors questioning the market’s brutal 11% selloff of Meta following the disclosures in its Q3 report. Some are on X saying they are wading in buying what they promote as “the deal of the century”. The following post details the reason why this may not be true at all and actually represent the exact opposite.

It’s rare to see investors truly confused as to why the market has reacted in such a way following a report. Usually, the reason is fairly clear, but this article is catalyzed by the number of traders on socials indicating true confusion as to why Meta’s stock reacted as it did. In this case, as detailed below, its a combination of factors that add up to the following conclusion:

Even after analyst downgrades overnight, there are likely further downgrades still to come.

Why? Didn’t Meta achieve 26% revenue growth in the quarter, accelerating strongly and the fastest since early 2024? Didn’t Meta beat on EPS in the quarter by nearly 9%? Isn’t Q3’s massive AI infrastructure investment positive for the future growth?

Those observations are true however it shows the problem with only focusing on the numbers achieved versus the implications inside them. This is a case of needing to delve deeper into the accounts, management language and guidance to unpack what’s going on. First a key section from our Earnings Analysis Report of Meta from yesterday:

Management Commentary & Tone: Significantly More Cautious. While the CEO remains visionary about AI, the CFO commentary shifted from “cautious” in Q2 to “alarmist” in Q3. Management warned that 2026 expense growth will be “significantly faster” than 2025 and CapEx growth “notably larger” due to expanding AI compute needs. A new material risk from U.S. “youth-related trials” was also introduced.

CFO (Outlook): The CFO’s commentary was the central focus of the report, carrying a significantly negative tone. The outlook warned that AI-driven “compute needs have continued to expand meaningfully”. This is expected to result in 2026 total expense growth being “significantly faster” than the 2025 growth rate, and 2026 capital expenditures dollar growth being “notably larger” than in 2025. Drivers include infrastructure, “incremental cloud expenses,” and AI talent. The CFO also added new legal risks, noting “a number of youth-related trials are scheduled for 2026” in the U.S. that “may ultimately result in a material loss”.

This is the benefit from conducting natural language processing when analyzing earnings reports and transcripts. The AI model we use has identified a significant tone shift from the CFO in particular, to try to reset expectations of costs, earnings and capex.

Here’s some other statistics that the headlines didn’t call out:

Total expenses grew 32% YoY in Q3 - faster than revenue, so margins are falling

Depreciation and Amortization grew a reported 27% YoY but when you normalize for a 10% tailwind from management cheekily changing depreciation useful lives of AI infrastructure this year, it was an underlying ~37% growth rate. This is the base rate that carries forward into 2026 when there will be no additional depreciation policy assistance. The growth in D&A will also escalate due to the acceleration in capex - so think of D&A potentially growing in the 40%-50% range in 2026!

Management gave a 2025 total expense guidance that implies Q4 expenses will grow 42% YoY! So expenses are accelerating upwards and total expense growth in 2026 could be even higher than the guided 42% run rate given the ramp being seen!

Capex growth was guided in 2026 to be larger in dollar terms than 2025 (+$32bn incremental) with language that indicates it will be “notably” larger. Think around $120bn total capex in 2026, up nearly $50bn! That’s the total cashflow from operations absorbed right there - before any buyback needed to offset stock based compensation.

Lets summarize those key stats, taking management’s statements into account, looking into 2026:

Expenses are likely to growth >42% YoY.

Capex will likely grow by up to ~$50bn or 69%.

Plus there’s potential revenue growth risks from youth protection social media trials and an FTC anti-trust case. See the following excerpt from ScanX on 23 September:

A Los Angeles judge has approved expert testimony about social media’s impact on youth in upcoming trials against major platforms like Meta, Snap, Google, and TikTok. The ruling allows 10 out of 11 proposed expert witnesses to testify, potentially strengthening hundreds of lawsuits alleging harm to young users. The judge rejected the companies’ Section 230 defense, stating it doesn’t apply when claims focus on platform design. Experts are prohibited from discussing the companies’ intent, focusing instead on the effects of the platforms.Implications for 2026 Earnings

Revenue: Let’s ignore the youth social media trial risks and assume revenue grows at 25% YoY. This is approximately equal to Meta’s Q3 growth rate and a full 8 percentage points ahead of consensus (+17% YoY) right now - so I’m being generous.

Expenses: lets assume they grow at Q4’s guided rate of 42%, even though there are indications from late in year hiring sprees, capex accelerations and phased depreciation that it could go higher than that.

Under this scenario, META’s EBIT goes from $82bn in 2025 to………. $82bn in 2026. Margins fall further, free cashflows go to zero or potentially negative given up to $120bn in capex in 2026.

So META in 2026 is facing zero core earnings growth, zero free cashflows, having to debt fund its buyback if it continues it (or may pause it) and we still don’t have any tangible plans for Meta to monetize hundred’s of billions in AI investment other than selling more ads and thick framed camera glasses for a population who mostly doesn’t normally wear glasses.

BTW, consensus has downgraded after the earnings report but still has Meta delivering 5% EBIT growth in 2026. As I said at the top, the “quality of earnings” analysis reveals further downside risks that will only escalate further if these youth trials enforce requirements that limit access or time and reduce ad inventory aimed at Meta’s crucial youth and young adult audience. It may sound strange, but some other countries have already implemented policies like this so its not as outlandish as it first seems.

Meta’s Hidden Debt

To fund this AI investment splurge, Meta has embarked on creative ways to move the arrangements off balance sheet. Here’s an except from our comprehensive 14 section Forensic Accounting Report that I’ve attached at the bottom for interested investors. It makes for detailed yet compelling reading, particularly the sections on management language, guidance bridge, costs and free cashflow trends.

This report is produced with The Inferential Investor’s Forensic research workflow available in the prompt library.

Excerpt from II’s Forensic Report on Meta Platforms Inc Q3 2025:

Shadow Leverage Calculation

Interpretation: A “shadow leverage” metric can be constructed by capitalizing the off-balance-sheet lease and commitment obligations to better reflect the company’s true economic leverage. A common method is to calculate the net present value (NPV) of these future payments. While the filings do not provide enough detail for a precise NPV calculation, we can use the face value of the commitments as a conservative proxy.

Reported Debt (FY24): $28,826 million

Reported Lease Liabilities (FY24): $20,234 million

Reported Total Financial Obligations: $49,060 million

Off-Balance-Sheet Commitments (as of Q3 FY25):

Leases not commenced: $58,140 million

Contractual Commitments: $81,190 million

JV Guarantee (Contingent): $28,000 million

Adjusted Total Financial Obligations (Pro Forma): ~$216,390 million

[Author Note: this figure is $216bn which is 3x EBIT and with this total continuing to grow at eye watering rates. Just the Contractual Commitments alone grew 190% QoQ - from Q2! Expect it to keep growing which will make leverage concerns the next focus by analysts given the uncertain monetization of AI by Meta.]

This adjusted figure is over 4.4 times the reported financial obligations on the balance sheet. This demonstrates a significant reliance on future commitments to secure infrastructure capacity, driven by the AI build-out.

Narrative on Hidden Leverage

Interpretation: Meta’s balance sheet, with reported neutral net debt/cash position at Q3 (incl lease liabilities in debt), appears highly conservative. However, this view is incomplete. The company is increasingly utilizing off-balance-sheet structures to finance its aggressive expansion, creating significant “shadow leverage.”

The most prominent example is the data center joint venture with Blue Owl Capital announced in October 2025. Meta contributed $4.3 billion in assets to the JV, receiving $2.6 billion in cash and a 20% equity stake. The JV is then financed primarily by the partner’s $7.0 billion cash contribution. Meta then leases back the data center capacity via a $12.3 billion initial operating lease. This structure allows Meta to build out massive data center capacity without recording the full asset and associated debt on its own balance sheet.

However, the economic substance is that Meta has committed to a long-term, debt-like payment stream. Furthermore, the residual value guarantee of up to $28 billion represents a material contingent liability. If the data centers are not renewed or their value falls below a predetermined threshold, Meta is on the hook for the shortfall. This, combined with over $81 billion in other contractual commitments for cloud and infrastructure, means the company’s true fixed obligations are vastly larger than what is reflected in its reported debt figures. This strategy reduces near-term reported leverage ratios but commits the company to substantial, multi-year cash outflows that will be a first call on future operating cash flow.

Implications for the Stock Price

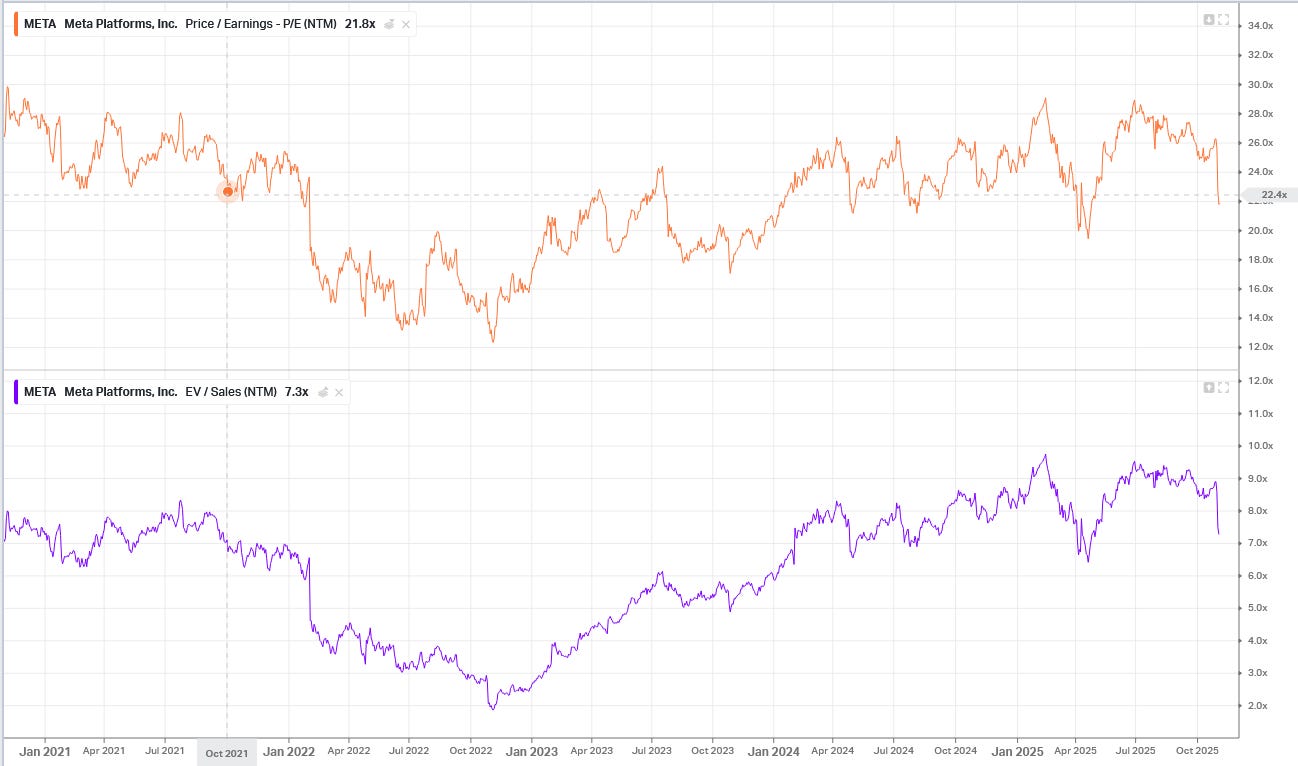

After the stock drop, and earnings downgrades, Meta remains on 23x 2026 EPS. If you overlay the earnings scenario described above, the real multiple is likely ~25x with zero earnings growth, no FCF, revenue growth risks from the legal cases/trials and likely share dilution to escalate from net (after buyback) SBC with a planned move to dividends from buybacks disclosed (no wonder with limited FCF).

What multiple then for that set of circumstances? Revenue growth is strong which is what most Meta investors focus on. But management choices as to investment and costs make that profitless growth, at least for the next couple of years.

I suggest that whenever fears regarding a business model or strategic direction appear, the multiple contracts and when those fears are accompanied by a collapse of growth, multiples contract meaningfully.

Meta has traded down to 15x-20x next twelve months EPS in growth slowdowns.

Google (Alphabet I probably should say) has traded at 17x-20x when the fears of AI cannibalization reigned.

Meta’s circumstances are wholly self-inflicted though which may temper the fall but I suggest that 20x a further downgraded EPS forecast, is a increasingly likely scenario. Q4 expense growth will likely shock investors who haven’t done the work above and catalyze further reductions in 2026 forecasts. If revenue growth is threatened during 2026 by the youth trials referred to by management, then expect a further retracement to 15x as this introduces a factor that is NOT discretionary, unlike the AI hiring and investment splurge.

Conclusion

My purely personal view is that logic and the body of evidence, unfortunately, spells potential further downside using the lens I place on share prices. The Q4 result will catalyze focus once again on trends in costs, capex and shadow leverage.

A Forensic Accounting Examination

The attached comprehensive forensic report on Meta Platforms is a tool used by investors to look for red flags in accounts, that can provide early indication of risks that ultimately affect earnings. This can be run on any company in approximately 5 minuts of processing with the ready made prompt in the prompt library. The report examines:

Accruals quality

Cash conversion and free cashflow quality

Revenue recognition

Capitalization choices

Working Capital Stress Tests

Leverage, Covenants and Liquidity

Off-balance sheet exposures

Stock based compensation trends

Segment and geographic economics

Auditor Signals

Management discussion and Analysis language

Related party transactions and governance

Provisions, contingencies and legal matters

Guidance to economics bridge

Happy Reading!

As always

Inference never stops. Neither should you.

Andy West

The Inferential Investor

I should have added that I have no long or short position in Meta at the time of publishing the report.