ADOBE (ADBE) Q1 FY26 Earnings Analysis - Acknowledging AI Disruption

In-line result to small beat but CEO announces exit, gross margin softness on back of AI disruption to Stock Image segment. Management sentiment falls.

The following report was generated with the Earnings Analysis Report workflow from the professional prompt library on The INFERENTIAL INVESTOR.

Subscribe to access these tools and stock research.

Important Disclaimer: The following stock discussion and analysis is subject to The Inferential Investor’s Disclaimer. It is indicative, designed to be educational and instructive on advanced techniques for AI in investment research and is not in any respect financial advice or an investment recommendation.

I. Performance Highlights and Quantitative Comparison

Adobe reported Q1 FY26 revenue of $6.40 billion, representing a 12% year-over-year (YoY) increase as reported (11% in constant currency). Non-GAAP EPS was $6.06, an increase of 19% YoY.

Key Business Drivers & Performance Indicators:

AI-First Adoption: ARR from AI-first applications more than tripled YoY.

User Growth: Monthly Active Users (MAU) for Acrobat, Creative Cloud, Express, and Firefly surpassed 850 million, growing 17% YoY. Creative freemium MAU crossed 80 million (up 50% YoY).

Generative Credit Consumption: Grew over 45% sequentially, skewed toward higher-value modalities like video and audio.

Enterprise Momentum: AEP & Apps and Adobe GenStudio ending ARR each grew over 30% YoY.

Structural Shifts (Weak Signals): Management noted a “greater-than-anticipated decline” in the traditional standalone Stock business. Additionally, the shift toward freemium web and mobile offerings is creating a “near-term impact on ARR”.

Performance Summary Table

Chart: Q1 FY26 Actuals vs. Consensus

Revenue (in $M)

Actual : ▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓ 6,398

Consensus : ▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓░░ 6,277

Adjusted EPS (in $)

Actual : ▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓ 6.06

Consensus : ▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓░░ 5.87

Overall, the company’s Q1 FY26 results beat consensus expectations across top and bottom lines, with 12% revenue growth and 19% EPS growth. Growth appears to be accelerating in emerging product lines due to AI monetization , offset partially by shifting dynamics in traditional legacy products.

II. Management Discussion & Analysis (MD&A) Comparison

Management Discussion (Current Quarter - Q1 FY26) Management emphasized the transition to an AI-driven business, highlighting that AI-first ARR tripled YoY. The narrative focused heavily on user acquisition, noting 850 million MAUs across core platforms. However, the quarter introduced significant structural news: CEO Shantanu Narayen announced his impending transition after 18 years. Management also acknowledged emerging headwinds, specifically a steeper-than-expected decline in the traditional Stock business and the dampening effect on short-term ARR caused by the rapid uptake of freemium offerings.

Management Discussion (Prior Quarter - Q4 FY25) The Q4 FY25 narrative was highly optimistic, capping off a record year of $23.77 billion in revenue. Management highlighted expanding generative AI model partnerships and the announcement of the $1.9 billion Semrush acquisition to bolster their agentic web capabilities. The tone was confident, pointing to a record $2.6 billion total net new ARR target for FY26 based on strong momentum across all customer groups.

Semantic Comparison & Tone Shifts

Sentiment Score Q4 FY25: 18/20 (Highly optimistic, emphasizing record execution and expanding total addressable markets).

Sentiment Score Q1 FY26: 14/20 (Positive but tempered).

Sentiment Delta: -4.0 points.

Thematic Shifts: Compared to Q4, management’s tone in Q1 became more cautious regarding revenue composition. While AI usage metrics remain a central theme, the sudden introduction of leadership transition discussions and the explicit acknowledgment of cannibalization in the Stock segment represent a regime shift. The language shifted slightly from “record growth” to “transitioning to an AI-driven business”.

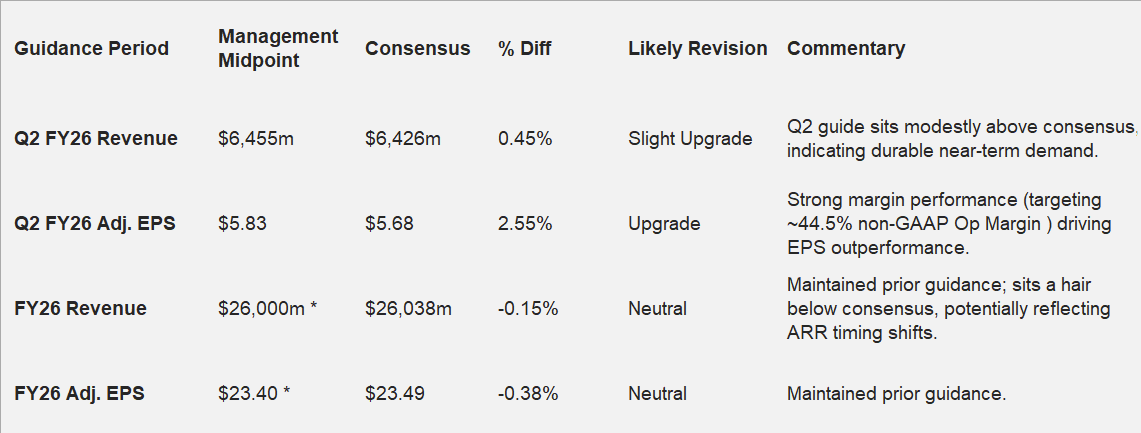

III. Guidance Evaluation and Consensus Implications

Management provided Q2 FY26 guidance and reaffirmed its full-year FY26 targets. Note that the guidance does not include any contribution from the pending Semrush acquisition.

*FY26 management midpoints are derived from the Q4 FY25 report where the full-year guide was initially issued , which was explicitly reaffirmed in Q1 FY26.

The implied QoQ revenue growth for Q2 at the midpoint is approximately 0.9% ($6,398m to $6,455m). We may see analysts lift Q2 estimates slightly, but leave full-year estimates largely unchanged as management opted not to raise the FY guidance despite the Q1 beat.

IV. What is missing and Emerging Risk Assessment?

Several areas present potential emerging risks or “weak signals” that the market may scrutinize:

Leadership Transition Uncertainty: The announcement that CEO Shantanu Narayen is transitioning out after 18 years is a major structural shift. The lack of an immediately named successor (the board is undergoing a search ) could introduce strategic uncertainty and execution risk during a critical AI pivot phase.

Cannibalization of Legacy Businesses: Management explicitly noted that the “traditional Stock business saw a steeper decline than we expected”. This is a critical weak signal. It suggests that Adobe’s own generative AI tools (Firefly) and third-party models may be cannibalizing legacy high-margin revenue streams faster than modeled.

Freemium Drag on ARR: The company is driving massive MAU growth via freemium offerings (crossing 80 million ), but admitted this approach has a “near-term impact on ARR”. The market may require more clarity on the exact conversion timeline and lifetime value (LTV) of these freemium cohorts to ensure this isn’t masking a deceleration in core paid seat growth.

Semrush Integration Updates: While the Semrush acquisition was mentioned as pending (expected to close in Q2 ), deeper details on integration costs or immediate synergy realization timelines were largely absent.

V. Conclusion

Adobe’s Q1 FY26 results demonstrate strong fundamental execution, characterized by top-line and bottom-line beats alongside explosive growth in AI-first ARR (tripling YoY). However, the quarter marks a pivotal regime change for the company. The impending departure of long-time CEO Shantanu Narayen introduces executive transition risk, while the unexpectedly rapid decline in the traditional Stock business highlights the double-edged sword of generative AI. While the company’s aggressive freemium user acquisition strategy could secure the next generation of creators, it may also alter the predictability and timing of short-term ARR growth. Investors must weigh the impressive momentum of Adobe’s new agentic and generative tools against the friction of cannibalization and leadership turnover in the coming quarters.