NVIDIA (NVDA) Q4 FY26 Earnings Call Analysis: "Compute Equals Revenue" is the new narrative

Blackwell and Vera Rubin ramps seeing accelerated revenue and earnings growth. Management trying to engineer a new narrative to get the stock price moving.

The following report was generated with the Earnings Call Transcript Analysis prompt from the professional prompt library on The INFERENTIAL INVESTOR.

Subscribe to access these tools and stock research.

Important Disclaimer: The following stock discussion and analysis is subject to The Inferential Investor’s Disclaimer. It is indicative, designed to be educational and instructive on advanced techniques for AI in investment research and is not in any respect financial advice or an investment recommendation.

Executive Summary

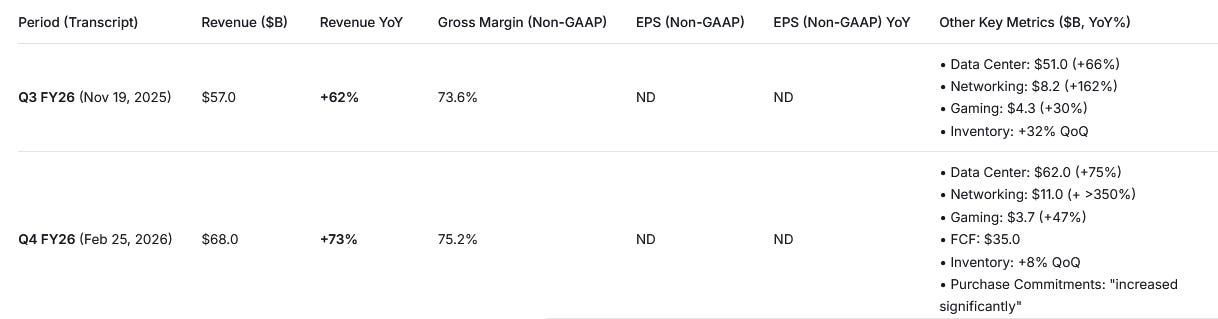

· Growth Trajectory: NVIDIA’s growth is not only sustaining but accelerating. Revenue growth re-accelerated from 62% YoY in Q3 to 73% YoY in Q4. The Data Center segment, now a $194 billion annual business, grew 68% YoY, with the Networking business more than tripling in Q4. The primary driver is the explosive demand for the new Blackwell architecture, which accounted for roughly two-thirds of Q4 Data Center revenue shortly after its ramp.

· Guidance Trajectory: The company has raised its near-term outlook significantly and extended its long-term visibility. Q1 FY27 revenue guidance of $78 billion (+2% implied) represents another ~15% sequential increase and a ~65% YoY jump. Crucially, management now sees sequential growth through all of CY26, exceeding the prior $500B Blackwell/Rubin revenue forecast, with supply secured into CY27.

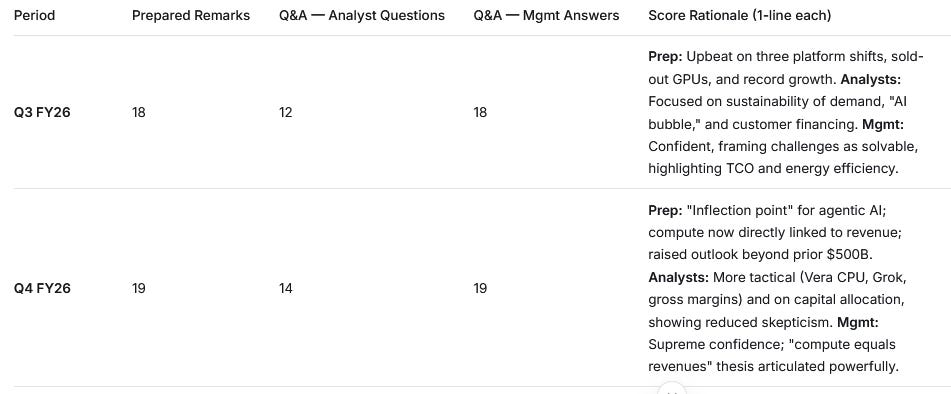

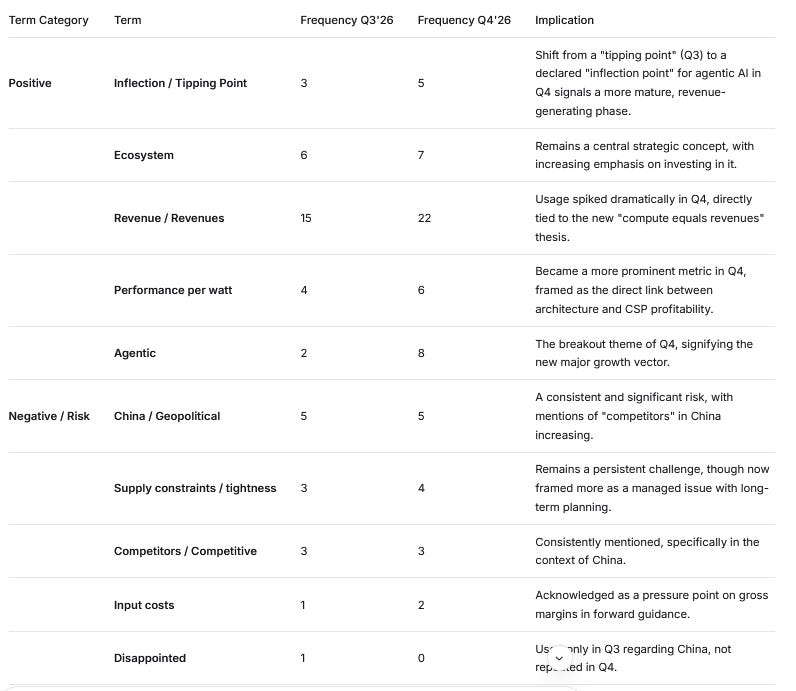

· Sentiment Evolution: Sentiment in prepared remarks has remained strongly positive, shifting from describing a “tipping point” in Q3 to declaring an “inflection point” for agentic AI in Q4. Analyst questions have evolved from concerns about an “AI bubble” and the sustainability of CapEx in Q3 to more tactical questions about specific products (Vera CPU, Grok) and capital allocation in Q4. Management’s confidence is at an all-time high, framing compute as directly equivalent to customer revenue.

· What Changed vs. Prior Call:

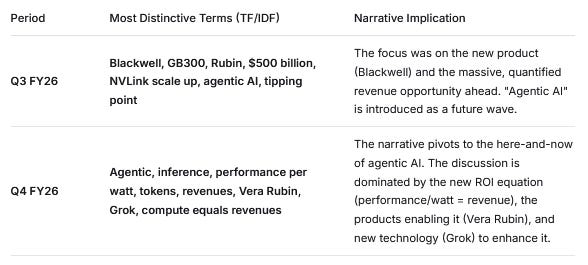

o The Narrative: Moved from the “early innings” of three platform shifts (Q3) to declaring that “agentic AI has arrived” and that “compute equals revenues” (Q4).

o Financial Scope: The $500 billion revenue opportunity (Blackwell+Rubin through CY26) is now a baseline that will be exceeded. Supply visibility has extended into CY27.

o Key Metric: Networking emerged as a standout star in Q4, with revenue more than tripling YoY to $11 billion, driven by the scale-up requirements of the new Blackwell systems.

o Strategic Positioning: The announcement of partnerships and investments with frontier model makers (OpenAI, Anthropic) and the acquisition of Grok’s technology signal a deepening moat and an intent to control more of the AI software stack.

Table 1 — Results & YoY Growth (stacked by transcript)

Table 2 - Operational & Segment Metrics

Table 3 — Guidance & Long-Term Goals Evolution

Key Forward-Looking Statements:

Q3 FY26 (Nov 19, 2025):

On Demand: “Demand for AI infrastructure continues to exceed our expectations.” (Colette Kress, p. 2)

On Revenue Visibility: “We currently have visibility to $0.5 trillion in Blackwell and Ruben revenue from the start of this year through the end of calendar year 2026.” (Colette Kress, p. 2)

On Competition: “Our competitors in China bolstered by recent IPOs are making progress and have the potential to disrupt the structure of the global AI industry over the long term.” (Colette Kress, Q4 p. 3 - *Note: This is from the Q4 call but referencing the long-term view*)

Q4 FY26 (Feb 25, 2026):

On Growth Trajectory: “We look ahead, we expect sequential revenue growth throughout calendar 2026, exceeding what was included in the $500 billion Blackwell and Rubin revenue opportunity we shared last year.” (Colette Kress, p. 2)

On Supply: “We believe we have inventory and supply commitments in place to address future demand, including shipments extending into calendar 2027.” (Colette Kress, p. 2)

On the New ROI of Compute: “In this new world of AI, compute equals revenues.” (Jensen Huang, p. 6)

Table 4 — Sentiment (0–20)

Thematic Summary (Prepared Remarks)

Q3 FY26 (November 19, 2025)

Growth Drivers: “Our customers continue to lean into 3 platform shifts, fueling exponential growth... We currently have visibility to $0.5 trillion in Blackwell and Ruben revenue.” (Colette Kress, p. 2). “Blackwell gained further momentum in Q3 as GB300 crossed over GB200 and contributed roughly 2/3 of the total Blackwell revenue.” (Colette Kress, p. 3).

Challenges: “We were disappointed in the current state that prevents us from shipping more competitive data center compute products to China.” (Colette Kress, p. 3). “Our competitors in China...are making progress and have the potential to disrupt the structure of the global AI industry.” (Colette Kress, p. 3).

Margins & Supply: “Gross margins increased sequentially due to our data center mix, improved cycle time and cost structure.” (Colette Kress, p. 5-6). “Inventory grew 32% quarter-over-quarter, while supply commitments increased 63% sequentially...preparing for significant growth ahead.” (Colette Kress, p. 6).

Strategy & Product Trends: “Our annual product cadence and extending our performance leadership through full stack design...the superior choice.” (Colette Kress, p. 2). “Thanks to CUDA, the A100 GPUs we shipped 6 years ago are still running at full utilization today.” (Colette Kress, p. 4).

Risks/Uncertainties: “There’s been a lot of talk about an AI bubble. From our vantage point, we see something very different.” (Jensen Huang, p. 6). The company actively addresses the narrative of unsustainable spending.

Q4 FY26 (February 25, 2026)

Growth Drivers: “Demand for our Blackwell architecture...continues to strengthen as inference deployments grow...Agentic and physical AI applications...are beginning to drive our financial performance.” (Colette Kress, p. 2). “We expect sequential revenue growth throughout calendar 2026, exceeding what was included in the $500 billion Blackwell and Rubin revenue opportunity.” (Colette Kress, p. 2). “Networking...was a standout...generating $11 billion in revenue, up more than 3.5x year-over-year.” (Colette Kress, p. 2-3).

Challenges: “We do not know whether any imports will be allowed into China.” (Colette Kress, p. 3). “We expect supply constraints to be the headwind to Gaming in Q1 and beyond.” (Colette Kress, p. 4). “Our competitors in China...are making progress and have the potential to disrupt the structure of the global AI industry.” (Colette Kress, p. 3).

Margins & Supply: “We have strategically secured inventory and capacity to meet demand beyond the next several quarters. This is further out in time than usual.” (Colette Kress, p. 5). For FY27, “working to hold gross margins in the mid-70s” despite input cost pressures. (Colette Kress, p. 5).

Strategy & Product Trends: “The Rubin platform...will train MOE models with 1/4 number of GPUs reduce inference token costs by up to 10x compared to Blackwell.” (Colette Kress, p. 4). “We recently entered into a nonexclusive licensing agreement with Grok for its low latency inference technology...we will extend NVIDIA’s architecture with Grok’s innovations.” (Jensen Huang, p. 6).

Risks/Uncertainties: The primary risk is no longer demand, but supply and geopolitics. The China market remains largely closed, and competitors there are gaining ground.

Q&A Summary

Q4 FY26 (Most Recent - February 25, 2026)

Topic: Sustainability of Customer CapEx (Vivek Arya, BofA): The analyst questioned if top cloud customers (~$700B CapEx) can sustain this level given cash flow compression. Management Answer: Jensen Huang introduced the core thesis that “compute equals revenues,” citing the inflection of agentic AI and its direct revenue generation for CSPs. He stated, “Without compute, there’s no way to generate tokens. Without tokens, there’s no way to grow revenues.” (p. 6-7).

Topic: Role of Strategic Investments (Joe Moore, Morgan Stanley): The analyst asked about the rationale behind investments in companies like Anthropic and potential OpenAI. Management Answer: Jensen explained these investments are “focused very squarely, strategically on expanding and deepening our ecosystem reach.” They are about ensuring the entire AI ecosystem, across all domains, is built on NVIDIA. (p. 7).

Topic: Spectrum-X Networking Momentum (Harlan Sur, JPMorgan): The analyst inquired about the current run rate of the Spectrum-X Ethernet platform. Management Answer: Jensen highlighted that networking is integral to their “AI infrastructure company” model. NVLink within the rack has “turbocharged” the business, and Spectrum-X Ethernet has been a “home run.” He claimed NVIDIA is “probably the largest Ethernet networking company in the world today.” (p. 8-9).

Topic: Future Product Roadmap (CJ Muse, Cantor Fitzgerald): The analyst asked about customized silicon (like for Grok) and the shift to a “dilate [chiplet] architecture.” Management Answer: Jensen defended architectural compatibility, stating it allows software investments to benefit all generations of GPUs, extending their useful life. He teased that Grok’s technology would be integrated as an “accelerator” similar to the Mellanox acquisition, not as a separate, incompatible product line. (p. 9-10).

Topic: Gross Margin Sustainability (Ben Reitzes, Melius): The analyst questioned the sustainability of mid-70s gross margins long-term. Management Answer: Jensen argued the “single most important lever” is delivering generational leaps in performance-per-watt and performance-per-dollar, which justifies the pricing and sustains margins. The fast product cadence and extreme co-design are key to delivering this value. (p. 12).

Q3 FY26 (November 19, 2025) - Summary of Themes

The dominant theme was the sheer scale of demand and the $500 billion revenue visibility. Analysts pressed on whether supply could ever catch up.

A significant portion of the Q&A was dedicated to addressing the “AI bubble” narrative and the ability of customers to fund such massive infrastructure builds.

Questions about inference as a percentage of the business and the specific capabilities of the Rubin platform (CPX for long context) were top of mind.

Jensen’s answers consistently steered the conversation toward the three simultaneous platform shifts (accelerated computing, generative AI, agentic/physical AI) to explain the structural, multi-layered nature of demand.

Recurring Themes Across Calls:

China: In both calls, management notes the inability to ship high-end products to China and acknowledges the rise of domestic competitors as a long-term risk.

Supply/Demand Imbalance: The persistent theme of demand outstripping supply is present in both, with Q4 providing more color on extending supply commitments into CY27.

Inference Leadership: In Q3, management hinted at it; in Q4, armed with new benchmarks (50x perf/watt), they declared victory, framing inference performance as the new key metric for customer profitability.

Term Frequency Table

*Based on a manual scan of the Q4 FY26 transcript for sentiment-bearing terms.*

TF/IDF Table (Most Distinctive Terms by Period)

Red Flags & Open Questions

Red Flag: China Market Loss & Competitor Rise. The company explicitly states that competitors in China are “making progress and have the potential to disrupt the structure of the global AI industry.” This is a significant admission of a rising long-term threat, not just a short-term revenue hole.

Source: Q4 p. 3

Red Flag: Gaming Supply Constraints. Management expects supply tightness to be a “headwind” to Gaming in Q1 and beyond. While not material to the overall business, it indicates allocation challenges persist and could leave money on the table in a profitable segment.

Source: Q4 p. 4

Red Flag: Rising Input Costs & OpEx. The company guides for gross margins to be “held” in the mid-70s despite rising input costs, and OpEx is set to grow in the “low 40s.” While driven by massive opportunity, this signals that gross margin expansion may be capped but that operating leverage at the operating margin line is still present.

Source: Q4 p. 5

Missing Disclosure/Inconsistency: China Revenue. In Q3, they said they were “not assuming any data center compute revenue from China.” In Q4, they stated “small amounts of H200 products for China-based customers were approved...we have yet to generate any revenue.” The lack of clarity on when/if this revenue will materialize and at what margins is a lingering uncertainty.

Source: Q3 p. 6; Q4 p. 3

Weak Signal: The “Grok” Acquisition. The language around Grok (”nonexclusive licensing agreement,” “welcome the team of brilliant engineers”) is reminiscent of the Mellanox acquisition. This could be a weak signal that NVIDIA sees a gap in its inference stack that it needs to fill to maintain its “Inference King” status, or it is a pre-emptive move to acquire critical talent/tech before a competitor does.

Source: Q4 p. 6

Implications for the stock

A. Does the composition of the result meet, exceed or fall short of analyst and market expectations prior to the result?

The results and, more importantly, the guidance exceeded expectations. The Q4 revenue of $68 billion and the Q1 guide of $78 billion represent a scale and growth rate that was not broadly anticipated in consensus numbers. The declaration that the $500 billion forecast will be exceeded and that sequential growth will persist through CY26 attempts to set expectations for longer term growth.B. What metrics have exceeded expectations and what areas have fallen short of expectations?

Exceeded: Data Center revenue growth (re-accelerating to 75%), Networking revenue (up >350%), and the sheer velocity of the Blackwell ramp (2/3 of Q4 DC revenue). The gross margin expansion to 75.2% in Q4 also exceeded their own outlook.

Fallen Short/Constrained: Gaming revenue, while growing 47%, is now supply-constrained, indicating potential revenue left on the table. China revenue remains at zero, a continued shortfall.

C. What are the implications for earnings growth in the immediate next period and longer term?

Immediate: The Q1 guide implies another massive sequential revenue jump, setting up another quarter of triple-digit (or near triple-digit) earnings growth, even with rising OpEx. The biggest lever remains Data Center.

Longer Term: The company’s own forecast implies a revenue base that will support continued, albeit decelerating, earnings growth for the next several quarters. The biggest long-term earnings driver will be the successful commercialization of the “physical AI” and robotics opportunity, which management has pegged as the next multi-trillion dollar wave.

D. Are there any reasons to expect the stock’s multiple to change?

Yes, but the direction is a complex debate. The positive case for multiple expansion is that the company is trying to provide visibility that removes the primary narrative overhang of “peak AI spending.” By tying compute to revenue and declaring agentic AI’s arrival, NVIDIA has made its growth look more structural and less cyclical. The negative case for multiple contraction is that the sheer size of the business ($78B quarterly revenue run-rate) makes it difficult to sustain historical growth rates, potentially attracting value-oriented multiple compression. Management are attempting to support the multiple with the new “compute equals revenue” paradigm which is designed to suggest a durable, utility-like demand for its products that was previously absent. This new narrative is primarily being echoed and relies upon OpenAI’s forecasts and narrative in its current capital raising process.