JP Morgan ($JPM) Q2 FY26 Results & Earnings Call Full Report

Record quarter and raised guidance but "as good as it gets"?

The following report was generated with Inferent Analyst’s agentic intelligence workflows. Subscribe to keep informed of this unique project as we move toward launch.

Important Disclaimer: The following stock discussion and analysis is subject to The Inferential Investor’s Disclaimer and any associated disclosures at the end of this report.

JPMorgan Chase & Co. (NYSE: JPM)

Q2 2026 Earnings Analysis Report followed by the Earnings Call Analysis

Reported July 14, 2026 | Prepared July 15, 2026

Executive Summary - Earnings Report

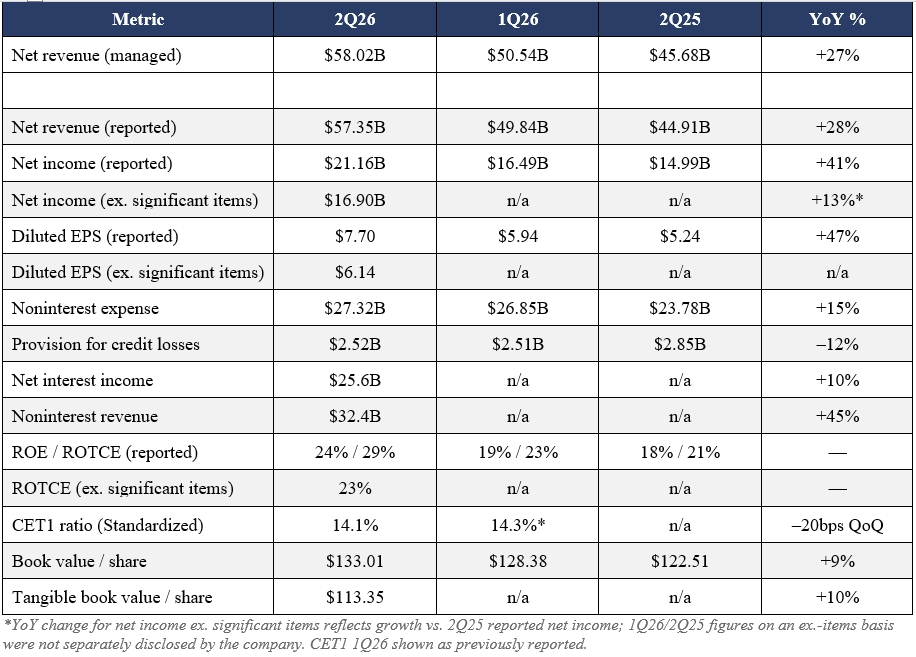

• Record quarter: net income $21.2B ($7.70/sh, reported), up 41% YoY; excluding significant items, net income was $16.9B ($6.14/sh, up 13% YoY) — the cleaner run-rate figure.

• Managed revenue $58.0B, up 27% YoY (reported revenue $57.3B, up 28% YoY); every line of business posted record revenue.

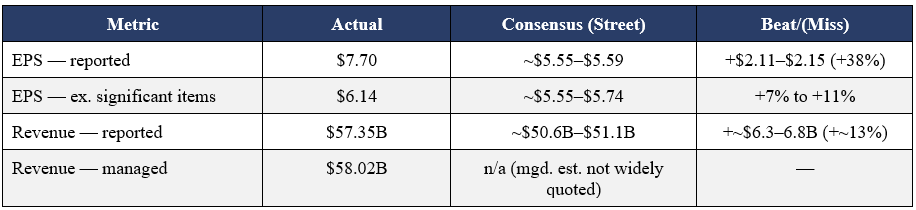

• Beat consensus decisively: adjusted EPS $6.14 vs. ~$5.55–$5.74 Street estimate (beat of ~7–11%); reported EPS $7.70 vs. same estimate (beat driven largely by the $4.6B Visa share-exchange gain plus $1.0B of equity investment gains, $5.6B combined, ~$1.56/sh).

• Markets revenue +35% YoY ($12.1B) led by Equity Markets +86% YoY; Investment Banking fees +30% YoY to $3.3B, highest since 2021; CIB net income $9.7B, up 46% YoY.

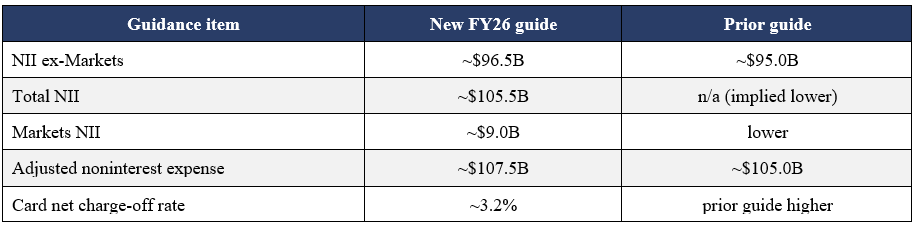

• Management raised full-year 2026 guidance: NII ex-Markets to ~$96.5B (from $95B), total NII to ~$105.5B, expense outlook up to ~$107.5B, and card net charge-off rate guided down to ~3.2%.

Headline Financial Results

Let me introduce you to Inferent Analyst - a cutting edge AI investment research platform being developed by investors - for investors. Inferent Analyst is designed to be every investor’s autonomous equity research assistant. No more pages and pages of raw numbers without context like traditional data terminals. Inferent Analyst actually interprets and analyzes the data automatically, as events unfold, presenting you with the insights you need to discover ideas and make better investment decisions. Pre-register today as subscriber seats will be limited on launch.

Net Interest Income & Margin

• Total NII was $25.6B, up 10% YoY. NII excluding Markets was $23.7B, up 4% YoY, driven by higher deposit balances, higher Card Services revolving balances and higher wholesale loan balances — partly offset by lower rates.

• Markets NII (embedded in trading revenue) rose as balance-sheet mix shifted toward more financing/less non-interest-bearing assets; management flagged this as a rare case where Markets NII moves were not fully offset in noninterest revenue.

• Average loans were $1.5T, up 10% YoY / 2% QoQ; average deposits up 7% YoY / 3% QoQ.

• Full-year 2026 guidance raised: NII ex-Markets to ~$96.5B (from $95B); total NII to ~$105.5B; Markets NII to ~$9B. CFO Jeremy Barnum attributed the increase mainly to higher deposit balances/mix, with a modest incremental effect from higher rates.

Actual vs. Consensus Estimates

• Beat was broad-based and revenue-driven (not cost-cutting): every line of business hit record revenue, led by Equity Markets (+86%) and Investment Banking fees (+30%).

• Reported-basis beat is inflated by ~$1.56/sh from the one-time Visa/equity-investment gains; the ex.-items beat (~7–11%) is the more decision-useful comparison for run-rate earnings power.

Management Guidance (Raised)

• Expense guide raised $2.5B; CFO noted $1.5B of that is already booked in 1H26 (direct consequence of the $6.5B capital-markets revenue outperformance vs. plan), with ~$1B added for 2H26.

• Q3 dividend increase to $1.65/sh confirmed, consistent with June CCAR announcement; $6.2B of net share repurchases in the quarter.

Key Surprises / Talking Points

• Equity Markets revenue +86% YoY was the single largest surprise — management explicitly said the combination of drivers (major IPOs, index rebalancing, Korean market dynamics, elevated Asia activity) is “improbable” to repeat at the same magnitude.

• Investment Banking fees +30% YoY included some pull-forward of M&A closings and large ECM deals; CFO Barnum flagged “some pull forward” but described the pipeline as “quite robust.”

• CEO Jamie Dimon on the environment: “It’s getting close to as good as it gets. We just don’t know how long it’s going to last.”

• Management-succession news: President/COO Marianne Lake is retiring; two co-Presidents were elevated in her place. Dimon said the CEO succession timetable is unchanged (“several years”).

• CET1 ratio dipped 20bps QoQ to 14.1% as RWA grew ~$103B, largely from higher CIB financing activity — capital remains well above regulatory minimums.

Q2 2026 Earnings Call — Transcript Analysis

Call held July 14, 2026, 8:30am ET | Speakers: Jamie Dimon (Chairman & CEO), Jeremy Barnum (CFO) | Prepared July 15, 2026

Executive Summary

• Tone was confident bordering on triumphant, but both Dimon and Barnum repeatedly hedged on durability — Dimon: “It’s getting close to as good as it gets. We just don’t know how long it’s going to last.”

• Biggest analyst focus areas: (1) CEO/President succession following Marianne Lake’s retirement, (2) sustainability of the Equity Markets/IB surge, (3) rising expense guidance and operating leverage optics, (4) capital deployment (buybacks vs. organic growth vs. M&A).

• Management raised FY26 NII ex-Markets guidance to ~$96.5B and total NII to ~$105.5B, but framed the $2.5B expense guidance increase as mostly a direct, healthy consequence of revenue outperformance, not scope creep.

• Dimon used the platform to press regulators on Basel III/G-SIB and short-term wholesale funding rules, arguing capital metrics are being computed “in a false way” rather than conservatively but honestly.

• No major analyst pushback on credit quality; Dimon and Barnum proactively flagged “mild” underwriting deterioration in leveraged/data-center lending as a watch item rather than a current problem.

Key Management Commentary by Theme

1. Macro backdrop / “as good as it gets”

“It’s getting close to as good as it gets. We just don’t know how long it’s going to last.”

— Jamie Dimon, in response to a question on whether results reflect peak conditions or an earlier-cycle inflection

“Several risks are shifting below the surface like tectonic plates, including geopolitical tensions and wars, sticky inflation, large global fiscal deficits and elevated asset prices.”

— Jamie Dimon, prepared remarks in the earnings release

• Dimon described the U.S. economy as showing “notable resiliency,” supported by AI-driven capital investment, fiscal stimulus, and more efficient regulation — but paired every bullish comment with a caution about tail risks.

2. Markets / Investment Banking sustainability

“The particular set of things that happened in equities this quarter, it’s a little bit hard to imagine that being repeated.”

— Jeremy Barnum, on the 86% YoY jump in Equity Markets revenue

• Barnum attributed the Equities surge to major IPOs, index rebalancing, unusual Korean equity-market dynamics, and broad Asia activity — calling it “all the headlines basically that have driven the market.”

• On Investment Banking: Barnum acknowledged “clearly there was some pull forward” from large deal closings this quarter, but said the pipeline “is actually quite robust” and that high-profile activity “is itself begetting more activity.”

• Dimon added a data point on AI capex: total U.S. capex is ~$4 trillion/year; AI-related capex rose from ~$400B to ~$700B YoY and is projected near $1 trillion+ next year, with a possible offsetting reduction in non-AI capex.

3. Expenses / operating leverage

“A rapid increase in revenue drives a big increase in operating leverage.”

— Jamie Dimon, pushing back on the framing that negative headline operating leverage is a concern

• Barnum explained the $2.5B FY26 expense guidance increase: ~$1.5B is already booked in 1H26 and is directly tied to the $6.5B of capital-markets revenue outperformance versus the original plan; only ~$1B is incremental for 2H26.

• Analyst Mike Mayo (Wells Fargo) computed an implied ~77% marginal margin on the incremental revenue and asked whether Dimon’s “as good as it gets” comment referred to the revenue environment specifically — Dimon reiterated uncertainty on durability rather than answering directly.

“The notion that somehow you can forever increase your operating leverage is a crazy notion. We don’t have that... I think it’s part of the reason why banks failed [in the past].”

— Jamie Dimon

4. Net interest income guidance drivers

• CFO Barnum: the NII ex-Markets guidance increase from $95B to $96.5B is driven mainly by higher deposit balances (both wholesale and consumer) and favorable mix shift, with a smaller contribution from modestly higher rates versus the prior forecast.

• Consumer deposit growth guidance (low single digits) is unchanged for the year; wholesale deposit growth has outperformed expectations, partly reflecting loan growth in “the MBFI space” and data-center-related lending creating deposits.

• A technical nuance flagged by Barnum: a shift of equity allocation into CIB (to support client-driven RWA growth) moved some NII from the ex-Markets line into Markets NII — a rare instance where a Markets NII change (~$150M) will not be offset elsewhere in the P&L.

5. Capital return, buybacks, and M&A

“Buying back stock is not returning money to shareholders. You’re making an investment decision, you’re not making a return-money-to-shareholders decision.”

— Jamie Dimon, responding to a question on why JPM continues buybacks at ~3x tangible book

• Dimon reiterated the firm wants to “buy back less stock as the price goes up and more as it goes down,” and said prior comments about a specific buyback figure (“$20 billion”) were a mistake to have disclosed — the firm will not pre-commit to a number.

• Framed capital deployment priorities as: (1) organic growth across every business (technology, branches, bankers), (2) opportunistic inorganic/M&A (“skunk works,” European digital banking build-out via Chase UK/Germany), with a target of deploying capital at a 17% return.

• On AI and efficiency (prompted by a comparison to Block’s workforce cuts): Dimon said AI will drive efficiency in specific areas (JPM has already cut some roles 30-40% in discrete areas, largely redeployed), but argued competitive dynamics mean “the benefit accrues to the customer,” not permanently to bank margins.

6. Regulation

“If they think we should [hold] more capital, they should ask us to hold 10% more. And I’d be happy to do that, but I’m not happy to have these numbers falsely done.”

— Jamie Dimon, on Basel III / G-SIB surcharge methodology

• Dimon called for eliminating perceived “double counting” in operational risk and market risk capital, and cited JPM’s largest-ever quarterly trading loss ($1.4B) against ~$80B of market risk capital as evidence current calibration is too conservative in a distortive way.

• Barnum added detail on short-term wholesale funding rule changes, arguing they disproportionately burden banks with combined markets/banking/consumer franchises (JPM, Bank of America) versus pure investment-bank competitors — a policy outcome he said should be stated explicitly if intended.

• Both executives expressed cautious optimism about a more stable, safety-and-soundness-focused regulatory regime going forward, referencing regulators Michelle Bowman and Kevin Hassett/Warsh-style reviews (transcript: “Mickey Bowman and Kevin Warsh”).

Analyst Q&A Highlights

Revised View / Watch Items

• Watch whether Q3/Q4 Markets and IB revenue normalize toward the “robust pipeline” management describes, or stay closer to the 2Q26 run-rate — management itself flagged the equities outperformance as unlikely to repeat, which sets up a tougher YoY compare in 2H26/1H27.

• Track the raised FY26 NII guide (~$105.5B total, ~$96.5B ex-Markets) against actual deposit-balance and rate trends; CFO’s own caveat is that deposit-beta convexity risk is unmodeled in terms of timing.

• Monitor credit underwriting commentary — Dimon flagged “mild” deterioration in covenants, revenue assumptions, and rollover/rate risk in leveraged and data-center financing; this is a leading indicator worth revisiting each quarter.

• Succession: co-Presidents (elevated from Marianne Lake’s prior role) are now the clearest internal CEO-succession signal; new CCB head’s (Troy) transition from markets/IB background into consumer banking is a franchise-risk item to watch given CCB is 34% of firm ROE base.

• Regulatory catalysts: Basel III endgame finalization and G-SIB surcharge/short-term wholesale funding rule changes remain live advocacy items for JPM; any relief could be a capital-return tailwind, while adverse changes could pressure buyback capacity.

• Capital deployment: no explicit buyback dollar guidance was given (Dimon said stating a prior $20B figure was a mistake) — treat quarter-to-quarter repurchase levels as a signal of management’s view on valuation (currently ~3x tangible book) rather than a committed program.

Appendix: Segment Performance

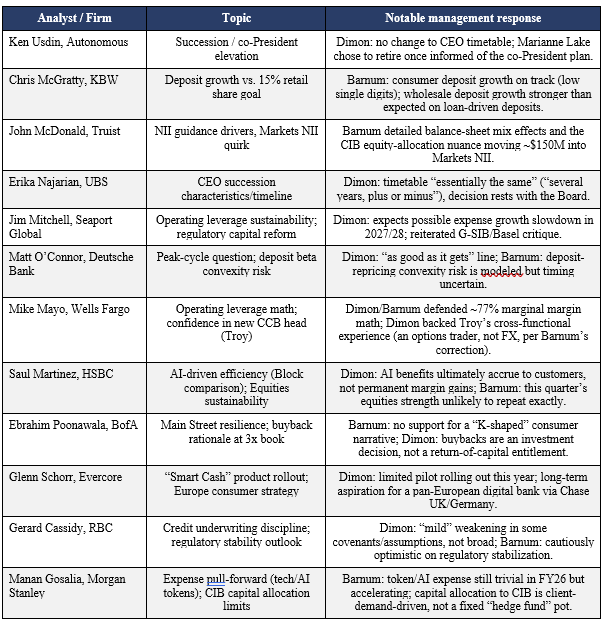

Consumer & Community Banking (CCB)

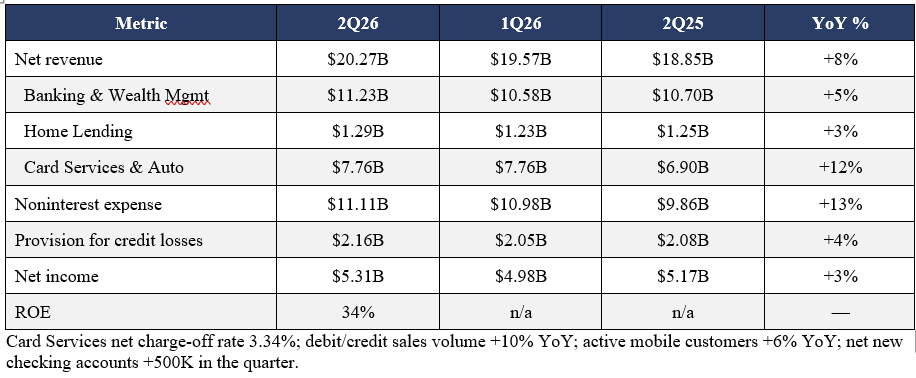

Commercial & Investment Bank (CIB)

Note: JPM’s segment structure no longer breaks out a standalone “Commercial Banking” segment — Commercial Banking was folded into CIB in the 2023 reorganization. Banking & Payments above includes the former Commercial Banking lending/payments book. #1 ranking in Global IB fees, 9.3% wallet share YTD.

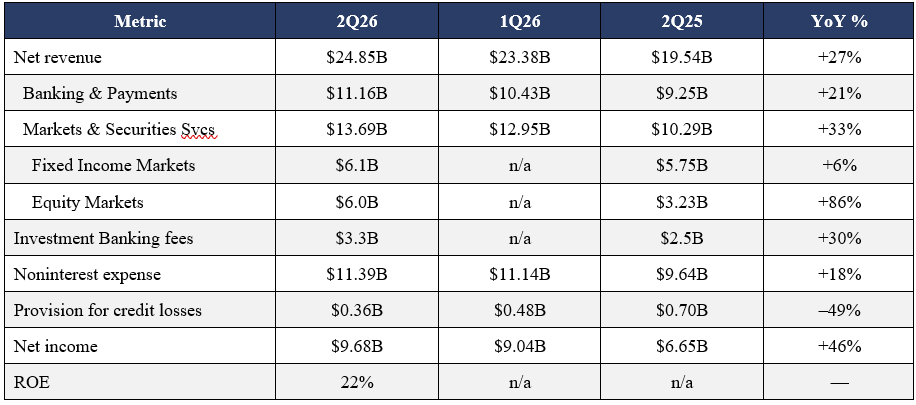

Asset & Wealth Management (AWM)

Corporate

• Net income $4.2B (vs. $1.7B in 2Q25), driven almost entirely by the $4.6B Visa Class B-2/C share-exchange gain and $763M of the $1.0B equity-investment gain booked in Corporate.

• Excluding significant items, Corporate net income was down ~$1.5B YoY, reflecting lower NII (down $667M on lower rates) and the absence of a $774M prior-year tax benefit.

Important Disclaimer: This analysis is subject to The Inferential Investor’s Disclaimer. It is for informational and educational purposes only and does not constitute investment advice, a recommendation to buy or sell any security, an offer or solicitation, or a guarantee of future performance. The information is derived from sources believed to be reliable but no representation or warranty is made as to its accuracy or completeness. Any forward looking or scenario descriptions are not forecasts but explorations of the implications of a set of described conditions and are subject to risk and uncertainty. Past performance is not indicative of future results. Readers should consult their own advisers before making any investment decision. This analysis is generated based on a standardized workflow. It has been prepared without taking account of your objectives, financial situation, or needs and does not constitute a recommendation on any security mentioned. You should consider the appropriateness of this information before making any investment decisions. AI can make mistakes.