Goldman Sachs ($GS) Q2 FY26 Results & Earnings Call Full Report

Record quarter with management flagging durable strength

The following report was generated with Inferent Analyst’s agentic intelligence workflows. Subscribe to keep informed of this unique project as we move toward launch.

Important Disclaimer: The following stock discussion and analysis is subject to The Inferential Investor’s Disclaimer and any associated disclosures at the end of this report.

Goldman Sachs Group (GS) — Q2 2026 Earnings Digest

Quarter ended June 30, 2026 · Reported July 14, 2026 · Prepared July 15, 2026

Executive Summary

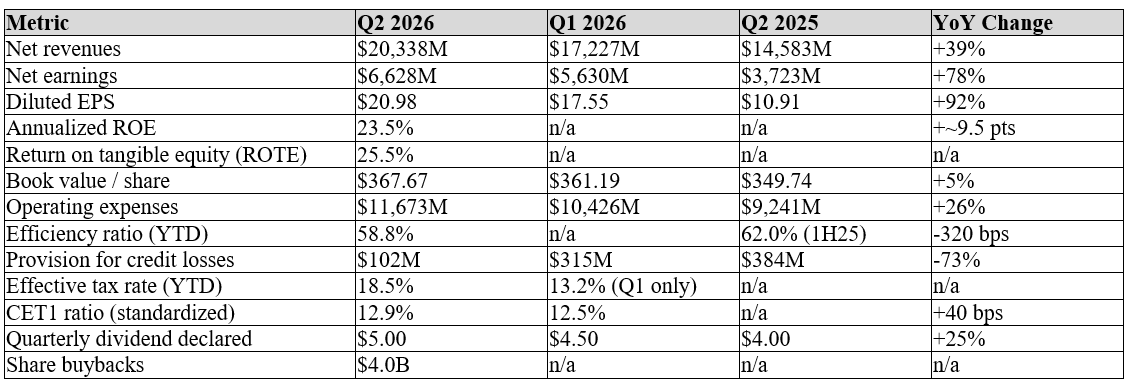

• Record quarter across the board: net revenues of $20.34B (+39% YoY, +18% QoQ) and diluted EPS of $20.98 (+92% YoY), both all-time firm records.

• Blew past consensus: EPS beat by ~46% ($20.98 vs. ~$14.38 est.) and revenue beat by ~26% ($20.34B vs. ~$16.12B est.) — one of the largest beats among major banks this cycle.

• ROE hit 23.5% (ROTE 25.5%), the highest in years, driven by Global Banking & Markets strength (record $15.52B, +53% YoY) — Equities (+72%) and Investment Banking (+55%) both surged.

• Asset & Wealth Management grew revenue 20% YoY to $4.60B; AUS crossed a record $4.0 trillion; 34th consecutive quarter of long-term net inflows.

• Capital returned to shareholders: dividend raised 25% to $5.00/share (14th straight year of increases) plus $4.0B of buybacks; CET1 ratio 12.9%, comfortably above the 11.4% requirement.

Headline Financial Results

Let me introduce you to Inferent Analyst - a cutting edge AI investment research platform being developed by investors - for investors. Inferent Analyst is designed to be every investor’s autonomous equity research assistant. No more pages and pages of raw numbers without context like traditional data terminals. Inferent Analyst actually interprets and analyzes the data automatically, as events unfold, presenting you with the insights you need to discover ideas and make better investment decisions. Pre-register today as subscriber seats will be limited on launch.

Actual vs. Consensus Estimates

Management Guidance & Forward Commentary

• AI infrastructure build-out described as still “early stages” — expected to keep driving financing, capital formation and advisory activity for several years, with possible short-term “recalibrations” over a 6-18 month horizon.

• Incentive fees in AWM expected to be “materially higher” in Q3/Q4 2026 on known/committed transactions.

• Full-year alternatives fundraising target raised to over $125B (from prior guidance), after a record $59B raised in Q2 alone ($31B in private credit).

• Platform Solutions revenue guided to stay roughly flat with Q2 levels through year-end.

• Full-year effective tax rate guided to approximately 20% (vs. 18.5% YTD).

• Capital priorities unchanged: invest in the client franchise at attractive returns first, sustainably grow the dividend, then return excess capital via buybacks.

• Investment banking backlog at its highest level in five years despite the very strong Q2 revenue print — management still “optimistic” on the IB outlook, noting sponsor/PE volumes remain below historical averages (a potential further upside lever).

Key Risks / Watch Items Noted by Management

• Supplementary leverage ratio (SLR) fell to 4.3% (from 4.7% in Q1), now the lowest among large-bank peers — a potential constraint on further balance-sheet-heavy growth (financing, prime).

• Client demand for financing reportedly exceeds what GS is willing to deploy — a self-imposed cap on some growth areas.

• Executives explicitly flagged the AI capex cycle could see “bumps and recalibrations” as real-world enterprise demand and pricing for AI infrastructure become clearer.

• Much of the quarter’s strength (equities, FICC) is tied to elevated market volatility and active capital markets — conditions management itself describes as cyclical, not guaranteed to persist.

Sources: Goldman Sachs Q2 2026 earnings press release / 8-K (SEC EDGAR, goldmansachs.com); Investing.com earnings-call transcript & beat/miss analysis (July 14, 2026); Goldman Sachs Q2 2026 earnings call (July 14, 2026).

Goldman Sachs Group (GS) — Q2 2026 Earnings Call Transcript Analysis

Call held July 14, 2026 · Speakers: David Solomon (Chairman & CEO), Denis Coleman (CFO) · Prepared July 15, 2026

Executive Summary

• Tone was confident and unusually assertive for a bank management team — Solomon repeatedly framed results as evidence of a multi-year strategic payoff (”One Goldman Sachs” cross-sell flywheel), not a one-off quarter.

• Management leaned into the AI capex cycle as a durable, multi-year revenue driver across advisory, financing and equities, while candidly acknowledging it “won’t be a straight line” and could see 6-18 month recalibrations.

• Analyst Q&A concentrated on sustainability/concentration of the equities beat, capital allocation trade-offs (buybacks vs. client deployment), and the now-lowest-among-peers SLR (4.3%) as a possible growth constraint.

• No guidance cuts or defensive hedging detected; management gave numeric forward guidance on incentive fees (materially higher 2H26), alternatives fundraising (>$125B FY target, raised), Platform Solutions (flat), and tax rate (~20% FY).

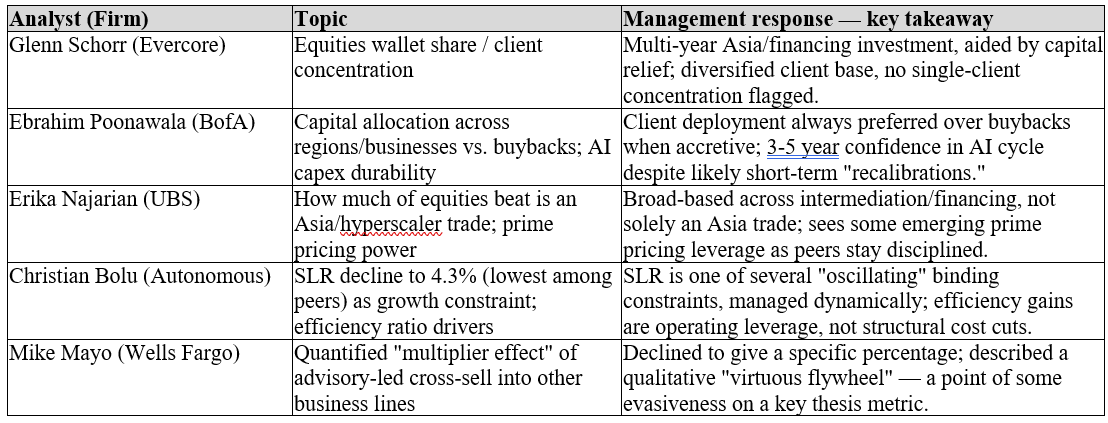

• Notable pushback: Mike Mayo (Wells Fargo) pressed for a quantified “multiplier effect” of advisory-led cross-sell; Solomon declined to give a number, offering only qualitative framing — a soft spot for a model built around that thesis.

Key Management Commentary by Theme

1. Record results as validation of strategy, not a one-off

“We delivered record results for the second quarter and year to date.” — David Solomon, CEO

“This is one of the most powerful things about our franchise... that flywheel is powerful.” — David Solomon, CEO, on cross-firm referrals

• Solomon tied the quarter to years of investment in ‘One Goldman Sachs’ connectivity — advisory mandates generating financing, wealth management and asset management follow-on work (nearly 900 IB-to-wealth-management referrals since start of 2025).

2. AI investment cycle as the central growth narrative

“The AI investment cycle is expanding capital needs beyond core technology into infrastructure, energy and data centers.” — David Solomon, CEO

“We are in the relative early innings of a very... significant AI build-out cycle.” — David Solomon, CEO

“It won’t be a straight line, and there’ll be bumps and... recalibrations.” — David Solomon, CEO

• Management explicitly framed its 3-5 year earnings confidence around the AI infrastructure buildout, while flagging near-term uncertainty on enterprise demand, chip pricing/efficiency, and token-cost economics.

3. Equities strength framed as durable, investment-driven, not a fluke

“The performance of our equities business... is the result of a number of multi-year investments.” — Denis Coleman, CFO

• CFO Coleman attributed the 72% YoY equities revenue jump to a deliberate multi-year buildout in equity financing/Asia, aided by regulatory capital relief received “at the turn of the year” that freed resources to chase Asian market share.

• Both executives pushed back on the idea this was a concentrated, client-specific windfall, describing a “highly diversified suite of clients” and disciplined portfolio-concentration management.

4. Capital allocation discipline

“It is always our desire to take our capital and allocate it toward supporting our clients... when we can do so in a way that produces... accretive returns.” — David Solomon, CEO

• Buybacks framed explicitly as the residual use of capital — deployed only when there’s insufficient opportunity to invest at attractive returns in the client franchise. This quarter saw both a capital cushion build and $4B of buybacks plus a 25% dividend hike.

5. Expense discipline / operating leverage

“Revenue grew about 40%... compensation expense rose 30%, non-compensation expense rose 22%.” — Denis Coleman, CFO (paraphrased from remarks)

• Efficiency ratio improved 320 bps YoY to 58.8% YTD, under management’s ~60% target. CEO Solomon was careful to say there has been “no structural change” to the expense base — the gains are from operating leverage on higher revenue, plus early AI/process productivity work under the “OneGS 3.0” initiative, not headcount cuts.

Analyst Q&A Highlights

Revised View / Watch Items

• Watch the SLR (now 4.3%, lowest among peers) — management concedes it is a live constraint on further balance-sheet-heavy growth (financing, prime); a binding limit could cap the equities-financing engine that drove this quarter’s beat.

• Track incentive fees in Q3/Q4 — management explicitly guided these “materially higher” on known transactions; a good near-term confirmation/disconfirmation data point for the AWM growth story.

• Sponsor/PE-led M&A volumes remain below historical averages per management — a plausible additional upside lever for IB fees if private-equity deal activity normalizes, on top of the already-strong strategic M&A backdrop.

• The AI-capex dependency cuts both ways: management’s own words (”bumps,” “recalibrations,” “early innings”) suggest this quarter’s growth engine is more macro/cycle-sensitive than the ‘One GS flywheel’ narrative implies — a single-quarter read-through should be tempered.

• Mike Mayo’s unanswered multiplier-effect question is worth revisiting each quarter — if management continues to decline quantification, treat the cross-sell/flywheel thesis as directionally supportive but not yet independently verifiable from disclosed metrics.

• No explicit change to credit-quality outlook; provision for credit losses fell sharply YoY ($102M vs. $384M), but this partly reflects the prior-year card portfolio (Apple Card, now held-for-sale) — not purely an improving underlying credit trend.

Important Disclaimer: This analysis is subject to The Inferential Investor’s Disclaimer. It is for informational and educational purposes only and does not constitute investment advice, a recommendation to buy or sell any security, an offer or solicitation, or a guarantee of future performance. The information is derived from sources believed to be reliable but no representation or warranty is made as to its accuracy or completeness. Any forward looking or scenario descriptions are not forecasts but explorations of the implications of a set of described conditions and are subject to risk and uncertainty. Past performance is not indicative of future results. Readers should consult their own advisers before making any investment decision. This analysis is generated based on a standardized workflow. It has been prepared without taking account of your objectives, financial situation, or needs and does not constitute a recommendation on any security mentioned. You should consider the appropriateness of this information before making any investment decisions. AI can make mistakes.