Bank of America (BAC) Q2 FY26 Earnings Analysis Report

Beats on Markets and IB performance. Improving management sentiment.

para 'Comprar' à medida que a empresa avança além das criptomoedas com ações e mercados de previsão")

The following report was generated with Inferent Analyst’s agentic intelligence workflows. Subscribe to keep informed of this unique project.

Important Disclaimer: The following stock discussion and analysis is subject to The Inferential Investor’s Disclaimer and any associated disclosures at the end of this report.

Bank of America (BAC) Earnings Report for Q2 2026

Bank of America Corporation (NYSE: BAC). Source documents: Q2 2026 and Q1 2026 press releases and investor presentations filed with the SEC (Form 8-K, Item 2.02).

Performance Highlights and Quantitative Comparison

Bank of America reported second quarter 2026 diluted earnings per share of 1.21 dollars, up 34 percent year over year and 9 percent quarter over quarter, on revenue, net of interest expense, of 31.6 billion dollars, up 15 percent year over year.

Both revenue and earnings per share came in ahead of consensus, with earnings per share beating by approximately 7 percent and revenue beating by approximately 3 percent.

Growth was broad based across all four business segments, with particular strength in Global Markets, where sales and trading revenue rose 33 percent year over year, and Global Banking, where investment banking fees rose 50 percent.

Net interest income of 16.0 billion dollars grew 9 percent year over year and 1.6 percent quarter over quarter, while non-interest income of 15.6 billion dollars grew nearly 22 percent year over year, reflecting higher asset management fees and markets revenue.

Pre-tax margin, calculated as income before income taxes divided by revenue, improved to 36.6 percent from 31.6 percent a year ago, consistent with management’s stated operating leverage of approximately 6.6 percent this quarter. Return on average tangible common equity rose to 17.03 percent from 13.61 percent a year ago.

Overall, the company’s Q2 results beat consensus expectations, with 15.0 percent revenue growth and 34.4 percent EPS growth. Growth appears to be accelerating relative to Q1’s 7 percent revenue and 25 percent EPS growth, driven by a broad based pickup in markets and investment banking activity alongside continued net interest income expansion.

Management Discussion and Analysis Comparison

Management Discussion (Current Quarter): Chair and CEO Brian Moynihan characterized the quarter as one of the company’s strongest to date, noting that every business segment delivered double digit net income growth and strong returns on equity. He pointed to disciplined expense management alongside growth investment as drivers of a roughly 360 basis point improvement in the efficiency ratio, and described near term investment banking pipelines as strong with commercial borrowing picking up.

Management Discussion (Prior Quarter): In the Q1 2026 release, management framed the quarter as a strong start to the year, with earnings per share up 25 percent year over year and net interest income that came in better than expected, up 9 percent. Management noted it remained watchful of evolving risks even as client activity, consumer spending and asset quality appeared resilient.

Compared to Q1, management’s tone in Q2 became more confidently growth oriented, shifting from a cautious watchfulness on risk toward explicit emphasis on strong pipelines and picked up commercial borrowing, which may suggest increased management confidence in near term demand, though the recurring reference to a resilient but closely watched economic backdrop was maintained across both quarters.

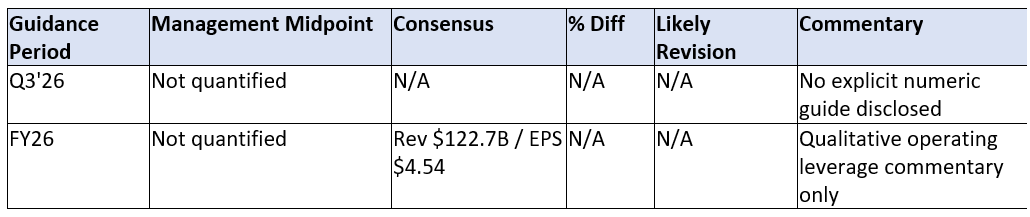

Guidance Evaluation and Consensus Implications

Neither the Q2 2026 nor the Q1 2026 press release or presentation disclosed explicit quantified revenue or EPS guidance for the next quarter or full year; Bank of America typically communicates net interest income and expense expectations qualitatively in these documents and in more specific terms on the earnings call, which was not among the source documents reviewed for this report.

Given the magnitude of this quarter’s beat and management’s more confident tone on pipelines, sell side analyst estimate revisions following the print could potentially skew modestly positive, though the absence of explicit management guidance in the reviewed documents means this assessment rests primarily on the scale of the beat and qualitative commentary rather than a directly comparable stated target.

Before the remainder of the analysis, let me introduce you to Inferent Analyst - a cutting edge AI investment research platform being developed by investors - for investors. Inferent Analyst is designed to be every investor’s autonomous equity research assistant. No more pages and pages of raw numbers without context like traditional data terminals. Inferent Analyst actually interprets and analyzes the data automatically, as events unfold, presenting you with the insights you need to discover ideas and make better investment decisions. Pre-register today as subscriber seats will be limited on launch.

What Is Missing and Emerging Risk Assessment

No explicit forward quarter or full year revenue, EPS, or net interest income guidance appears in the press release or presentation exhibits reviewed; a transcript of the earnings call, not included in this analysis, would likely be needed to assess management’s specific forward looking commentary and any guidance revisions.

Provision for credit losses of 1,366 million dollars in Q2 2026 is roughly flat versus 1,337 million dollars in Q1 2026 but below the 1,592 million dollars provisioned in Q2 2025, which may be a constructive signal on credit quality, though the source documents do not break out the drivers of this change by portfolio segment in detail.

The strength in Global Markets and Global Banking segment revenue, up 33 percent and driven partly by a 50 percent rise in investment banking fees, reflects a market and deal environment that could prove more cyclical than the steadier consumer and wealth management segments, a potential source of variability in future quarters that was not addressed in the source documents.

Average loans and leases of 1,203 billion dollars for the six months grew meaningfully versus 1,111 billion dollars a year earlier; the documents reviewed do not provide granular detail on loan mix or underwriting standards behind this growth.

Conclusion

Bank of America’s second quarter 2026 results reflect broad based, accelerating growth across all four business segments, with earnings per share and revenue both beating consensus and management describing one of the company’s strongest quarters to date.

Net interest income growth, expanding fee income in wealth management, and a sharp rise in markets and investment banking activity all appear to be positive contributors, alongside continued expense discipline that management links to margin improvement.

At the same time, the more cyclical nature of the markets and investment banking revenue that drove much of the acceleration, could represent a weak signal worth monitoring for the durability of this growth rate into subsequent quarters.

Sentiment across the current and prior releases remains constructive, with a notable shift toward more confident language on near term pipelines and commercial borrowing activity.

Important Disclaimer: This analysis is subject to The Inferential Investor’s Disclaimer. It is for informational and educational purposes only and does not constitute investment advice, a recommendation to buy or sell any security, an offer or solicitation, or a guarantee of future performance. The information is derived from sources believed to be reliable but no representation or warranty is made as to its accuracy or completeness. Any forward looking or scenario descriptions are not forecasts but explorations of the implications of a set of described conditions and are subject to risk and uncertainty. Past performance is not indicative of future results. Readers should consult their own advisers before making any investment decision. This analysis is generated based on a standardized workflow. It has been prepared without taking account of your objectives, financial situation, or needs and does not constitute a recommendation on any security mentioned. You should consider the appropriateness of this information before making any investment decisions. AI can make mistakes.