Amazon (AMZN) Q4 FY25 Earnings Call Insights: AWS putting its foot on the gas.

Key Takeaways: AI investments being monetized immediately. Supply, not demand constrained. AWS margins expanding as AI investments are delivered on.

The following report was generated with the Earnings Call Transcript Analysis prompt from the professional prompt library on The INFERENTIAL INVESTOR.

Subscribe to access these tools and stock research.

Important Disclaimer: The following stock discussion and analysis is subject to The Inferential Investor’s Disclaimer. It is indicative, designed to be educational and instructive on advanced techniques for AI in investment research and is not in any respect financial advice or an investment recommendation.

Executive Summary

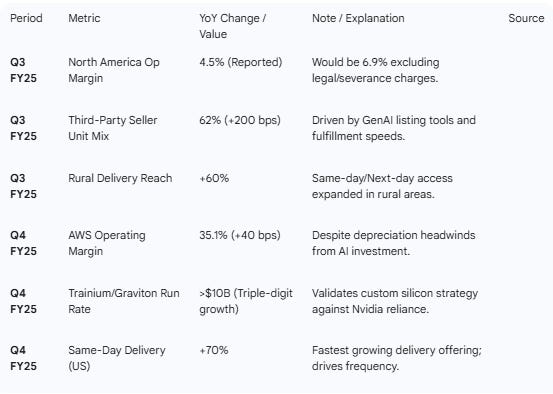

AWS Re-acceleration Thesis Confirmed: AWS revenue growth accelerated meaningfully from 20.2% in Q3 FY25 to 24% in Q4 FY25, reaching a $142 billion annualized run rate.

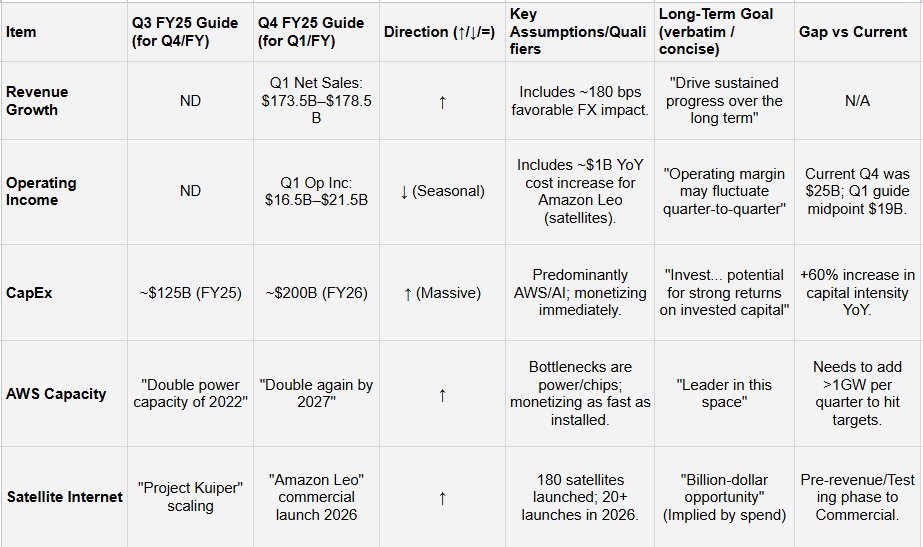

AI Capex Surge: Management guided to ~$200 billion in CapEx for 2026, a massive increase from ~$125 billion in 2025, predominantly allocated to AWS and AI infrastructure. This was ~60% above consensus expectations for FY26.

Monetization Confidence: Management aggressively defended the CapEx ramp, stating they are “monetizing [capacity] as fast as we can install it” and that AI supply is constrained relative to demand. Given the ramp in investment over 2025 and 2026 (planned), this statement (supported by 40% backlog growth) is suggestive of further revenue acceleration in AWS.

Custom Silicon Scale: The combined chips business (Trainium + Graviton) has surpassed a $10 billion annualized revenue run rate, growing triple-digits YoY, validating the vertical integration strategy.

Retail Efficiency & Speed: Delivery speeds hit records in both quarters; regionalization and robotics are driving cost-to-serve improvements, though Q1 FY26 faces a ~$1 billion cost headwind from the “Amazon Leo” satellite program.

Recurring “Special Charges”: Both quarters featured significant one-off charges (Q3: $4.3B; Q4: $2.4B) related to legal settlements, severance, and impairments, obscuring underlying GAAP operating margin expansion.

Advertising Strength: Advertising revenue maintained robust 22% YoY growth in both Q3 and Q4, driven by Prime Video ads and full-funnel capabilities.

Backlog Growth: AWS backlog grew 40% YoY to $244 billion in Q4, signaling long-term durability in the cloud re-acceleration.

Guidance Tone: Q1 FY26 operating income guidance ($16.5B–$21.5B) reflects seasonality and the “Leo” investment ramp but remains constructive on core operational efficiency.

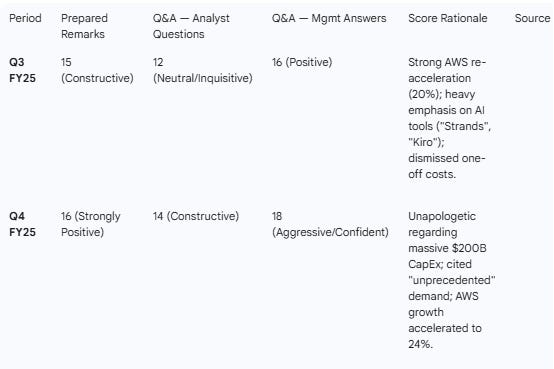

Sentiment Shift: Tone shifted from “optimistic re-acceleration” in Q3 to “aggressive AI dominance” in Q4, characterized by the massive capital commitment to capture the AI infrastructure layer.

Results & YoY Growth

For the full result and guidance analysis, refer our separate Detailed Q4 FY25 Earnings Analysis report for AMZN

Operational & Segment Metrics

Table 3 — Guidance & Goals Evolution

Key Management Quotes on Outlook:

Q4 (CapEx): “We expect to invest about $200 billion in capital expenditures across Amazon, but predominantly in AWS... we’re monetizing capacity as fast as we can install it.”

Q4 (Chips): “Trainium2 is... a multibillion-dollar annualized revenue run rate business... We expect nearly all of our Trainium3 supply of chips to be committed by mid-2026.”

Q4 (Satellites): “Within the North America segment, we do expect a year-over-year cost increase of approximately $1 billion related to Amazon Leo.”

Sentiment Scoring (0–20)

Despite the stock sell off on the disappointing OP guidance and capex shock, we note that analysts were more constructive in questioning as measured by language sentiment tracking. This potentially suggests that, on average, they will not be deterred with respect to price targets and ratings by the massive investment ramp announced.

Thematic Summary (Prepared Remarks)

Q4 FY25 Themes

Aggressive Infrastructure Investment: The headline theme was the pivot to massive capital intensity ($200B CapEx) to support Generative AI. Management framed this as a “land grab” where supply is the only constraint.

Custom Silicon Validation: Trainium and Graviton are no longer experiments but “multibillion-dollar” businesses. Trainium2 is fully subscribed; Trainium3 is effectively pre-sold.

Satellite Internet (Amazon Leo): Moved from R&D discussion to commercial launch timeline (2026) and specific financial headwinds ($1B cost in NA).

Retail Velocity: “Amazon Now” (ultrafast delivery) and the “Add to Delivery” feature are driving frequency and basket consolidation.

Key Quotes:

“We expect to invest about $200 billion in capital expenditures... predominantly in AWS.”

“AWS growth continued to accelerate to 24%, the fastest we’ve seen in 13 quarters.”

“We’ve landed over 1.4 million Trainium2 chips, our fastest ramping chip launch ever.”

Q3 FY25 Themes

AWS Re-acceleration: Revenue growth hit 20.2%, the highest in 11 quarters, driven by the end of optimization cycles and new AI workloads. Management highlighted a backlog of $200B.

AI Stack & Agents: Heavy focus on “Agentic AI.” Launched tools like “Strands” (agent creation) and “AgentCore” (infrastructure). Cited specific adoption by Ericsson and Sony.

Grocery Expansion: Pushed the narrative of perishable delivery speed. “Everyday Essentials” growing nearly 2x faster than the rest of the business.

One-off Financial Noise: Operating income was impacted by a $2.5B FTC settlement and $1.8B severance charge, creating a messy headline number but strong underlying margin story.

Key Quotes:

“AWS is growing at a pace we haven’t seen since 2022, reaccelerating to 20.2% year-over-year.”

“A lot of the future value companies will get from AI will be in the form of agents.”

“We expect to add at least another 1 gigawatt of power [in Q4].”

Changes in Commentary (Q4 vs Q3):

The most significant shift is the scale of capital commitment. In Q3, CapEx was guided to ~$125B; in Q4, this exploded to ~$200B for 2026. Management moved from discussing AI as a “feature set” (Agents, Bedrock) in Q3 to discussing it as an “infrastructure war” in Q4, necessitating massive power and chip procurement. The specific naming of “Amazon Leo” costs ($1B headwind) creates a new distinct drag on North American margins not explicitly quantified in Q3. The tone on custom silicon shifted from “gaining momentum” to “dominant differentiator” with specific revenue run rates ($10B+) provided for the first time.

Q&A Summary (Q4 FY25 Focus)

Analyst: Mark Mahaney (Evercore ISI)

Question: Questions the long-term Return on Invested Capital (ROIC) given the massive CapEx cycle. Asks for guardrails or minimum FCF levels.

Answer (Brian & Andy): We are monetizing capacity immediately upon installation. AWS operating margins expanded to 35% despite depreciation. The demand signal is strong, not speculative. Most CapEx is for AWS AI and core growth.

Analyst: Doug Anmuth (JPMorgan)

Question: Status of “Project Rainier” (Anthropic cluster)? Are there financial governors on spend?

Answer (Andy): Trainium is a multibillion-dollar business. Rainier (500k to 1M chips) is progressing well. Trainium2 is fully subscribed; Trainium3 committed by mid-2026. We will invest aggressively because it is an “unusual opportunity.”

Analyst: Ross Sandler (Barclays)

Question: Is AI spend too concentrated in a few labs? How is the OpenAI relationship evolving?

Answer (Andy): Demand is “barbelled”—Labs on one side, Enterprise apps on the other. The “middle” (enterprise production) will eventually be the largest. OpenAI is a significant partner (agreement in Nov), but the market will be thousands of companies, not just a few.

Analyst: Michael Morton (Moffett Nathanson)

Question: Impact of Agentic commerce on retail/ads? Will horizontal agents compress the funnel?

Answer (Andy): Optimistic about “Rufus” (300M users). Horizontal agents lack transaction history, trust, and accurate pricing. Retailer-specific agents (vertical) offer a better experience.

Analyst: Brian Nowak (Morgan Stanley)

Question: Sources of retail efficiency vs. investment areas in 2026?

Answer (Andy): Investments: Selection (luxury/brands), Speed (Quick commerce “Amazon Now”). Efficiency: Regionalization (now 10 regions), packaging efficiency (more units per box), and robotics (1M+ robots).

Analyst: Eric Sheridan (Goldman Sachs)

Question: State of backlog? Internal vs External AI demand balance?

Answer (Andy): Backlog is $244B (+40% YoY). Vast majority of CapEx is for external customers (Amazon internal is a small fraction). Supply is the constraint; “we could actually grow faster if we had all the supply.”

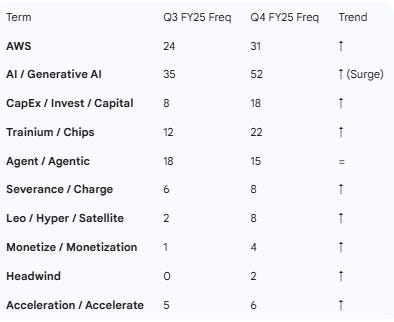

Term Frequency Tracking

TF/IDF Narrative: The term “CapEx” and “200 billion” dominates the uniqueness of the Q4 transcript compared to Q3. “Trainium” and “Chips” also see a marked increase in weighted importance, signaling the shift from software/services (Agents) in Q3 to hard infrastructure in Q4. The emergence of “Leo” (Satellites) as a specific cost center is a new distinct topic.

We recently examined the long term LEO investment case for Amazon explained here:

Amazon LEO: Adding to the Re-Acceleration of AWS & Prime Revenue Growth

·By accessing and reading this article, readers acknowledge and agree to be bound by the terms of our full legal disclaimer. The information provided herein is for educational and general informational purposes only and does not constitute professional financial or investment advice nor a recommendation to trade in any stock mentioned.

Red Flags & Open Questions

CapEx Shock: The jump to ~$200B CapEx is unprecedented. While management claims immediate monetization, the depreciation drag will be massive in future quarters if demand softens.

Serial “One-Off” Charges: The company has reported significant “special charges” for two consecutive quarters ($4.3B in Q3, $2.4B in Q4). This pattern degrades the quality of earnings and makes GAAP-to-Non-GAAP bridges crucial for valuation.

Satellite Cash Burn: The admission of a $1B cost increase for “Amazon Leo” in NA indicates the satellite internet project is entering a heavy investment phase before commercial revenue is proven.

Retail Margin Opacity: While North America margins are optically high (9%), they are heavily influenced by the mix of advertising. The underlying purity of retail margins remains obscured by the “Leo” costs and ad revenue.

Implications for the Stock

A. Performance vs. Expectations The result itself represents a beat on a normalized basis. AWS acceleration to 24% likely exceeds buy-side expectations which were pegged closer to the 20-21% trend established in Q3. The backlog growth of 40% supports potential further acceleration, particularly given indications that they are monetizing capacity as soon as commissioned and are supply, not demand, constrained. However the scale of the announced Capex and guidance of operating profit 14% below consensus for Q1 are weighing on the stock, particularly in the current risk-off market environment.

B. Areas of Outperformance / Underperformance

Outperformance: AWS Revenue (+24% YoY), Advertising (+22% YoY), Custom Silicon adoption (Trainium fully subscribed).

Underperformance: GAAP Operating Income quality is marred by recurring legal/severance charges. The $1B “Leo” drag on North America margins is a new negative distinct from core retail operations. Capex is 60% above market expectations for FY26.

C. Implications for Immediate Growth: Revenue growth near term should remain in the mid double digits and even accelerate, supported by favorable FX (180 bps tailwind in Q1) and investments already made coupled with comments regarding the “supply, not demand constraints”.

Margin dilution flagged in Q1 FY26 (and likely ongoing) due to the Q1 seasonality reset, accelerated investment program and the step-up in “Leo” costs heavily impacts the rate of earnings growth in FY26.

Below the headlines, the positive side to the story is accelerating AWS revenue growth with underlying AWS margin expansion (to 35%). This is pointing to value accretive ROIC on AI investments which is a clear concern of the market given the capex ramp. The other market concern regarding the growth gap in AWS compared to Microsoft and Google, may be narrowed in future quarters as AI investments are “immediately monetized” per management comments.