The Solid State Battery Shift Part 2: The Leaders, Breakthroughs & Hard Evidence that this time its Real

By accessing and reading this article, readers acknowledge the terms of our full legal disclaimer. The information provided herein is for educational and general informational purposes only and does not constitute professional financial or investment advice nor a recommendation to trade in any stock mentioned.

Emerging Leaders in the Solid-State Race

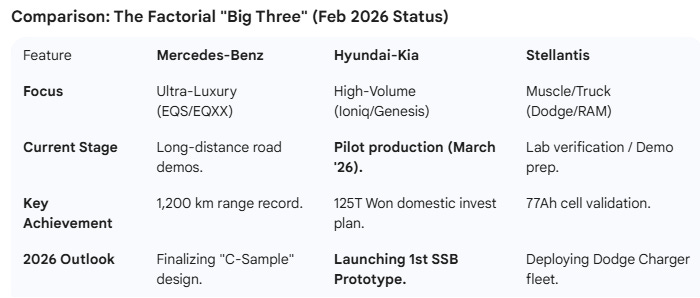

There appears to be mounting evidence that 2026 has officially marked the end of the “vaporware” era for next-generation solid state battery technology. For years, the automotive and investment worlds have viewed solid-state batteries (SSBs) with skepticism as companies missed self imposed deadlines - underscoring the technical challenges of this technology. However, as we stand in mid-February 2026, a number of developments have occurred very recently that appear to have fundamentally shifted the view. The race for the promise of solid state batteries (“SSBs”) with twice the range, one-third the charging time and 4x the lifespan is narrowing down to only a few distinct leaders, each representing a different philosophical and technical approach: I focus here on Toyota and Factorial with more in depth evidence of their progress. This builds on Part 1 of this series which you can catch up on below if you missed it. This topic appears to have stoked huge interest amongst investors with over 20x the views relative to my subscriber base!:

The Imminent Solid State Shift, aka "Toyota's Revenge"

By reading this article, readers acknowledge the terms of our full legal disclaimer. The information provided herein is for educational and general informational purposes only and does not constitute professional financial or investment advice nor a recommendation to trade in any stock mentioned.

As of today, Toyota is in the later stages of B-sample validation, having recently secured official production approval from the Japanese government and broken ground on its first large-scale electrolyte pilot facility. Factorial is arguably further ahead in the integration cycle by providing semi-solid state cells as an interim phase, with its B-sample cells already powering road-going prototypes for Mercedes-Benz and a major demonstration fleet for Stellantis scheduled to hit the road this year.

Both leaders appear to have overcome the disappointing “Dendrite and Interface” failures that set the industry back in 2021. This article takes readers through the challenges, breakthroughs and evidence that these players are progressing fast to commercialization now.

How Batteries Reach the Road

Before we dive into the specifics of these two leaders, it is critical for any investor to understand the validation process every battery must survive before it is allowed into vehicles offered to the consumer.

A-Sample (The Science Project): These are lab-built, hand-assembled cells. They aim to prove the chemistry works in a controlled environment. Challenges here are mainly chemical (e.g., Does it catch fire?, Can it be recharged repeatedly?). Solid State Batteries were stuck in the A-sample process for 15 years as they identified and sought to overcome various technical challenges. Companies missed self imposed deadlines many times over this period as new challenges presented themselves. This is the period where many investors became disillusioned with the promises.

B-Sample (Prototyping): This is the stage where Toyota and Factorial now reside. These cells are built on pilot production lines using automated machinery. They are the first cells integrated into “mules” (test vehicles).

While the A-sample proves the chemistry works, the B-sample aims to prove the manufacturing process works.

Design is Frozen: Unlike earlier stages, the cell’s dimensions, chemistry, and internal structure are now locked in. To progress to B-samples suggests most of the technical chemical challenges have been solved to the company’s satisfaction.

Process Intent: The cells are no longer hand-built by engineers in a lab; they are produced on a pilot production line using the same machines and methods intended for the final factory.

Vehicle Integration: B-samples are the first cells designed to be packed into modules and installed in actual working prototype vehicles (like Dodge Charger or Lexus mules).

C-Sample (Pre-Production): These cells are built on the final, high-volume production line. They are used for final safety certification (crash tests) and provided to media and dealers for evaluation.

S-Sample (Series Production): The final stage where the battery is sold to customers.

What Stage Has Toyota Achieved?

Like all solid state battery projects, Toyota’s path to 2026 has taken a lot longer than they anticipated. After missing its original 2020/21 launch target that was somewhat arbitrarily pushed to align with the Tokyo Olympics, the company restructured its entire “BEV Factory” unit. The subsequent 5 years has seen developments and breakthroughs that have pushed them out of the lab and into B-sample validation of manufacturing and on-road testing. This is the reason for my attention on this topic now - these are no longer lab experiments as they have been for the last 15 years.

Hard Evidence of Toyota’s Move to SSB Commercialization

As a signal that Toyota now has confidence that their technical solution is ready to be developed into the commercialized product, in late 2025, Toyota sought and secured a $841 million (117.8 billion yen) grant from Japan’s Ministry of Economy, Trade and Industry (METI) that required them to present validation data showing the technology's performance in a vehicle environment. Toyota subsequently briefed the press (documented via EEWorld and SMM) that this validation included initial testing of prototype battery packs in Lexus-branded mules. The grant also came with concrete timings for the first time:

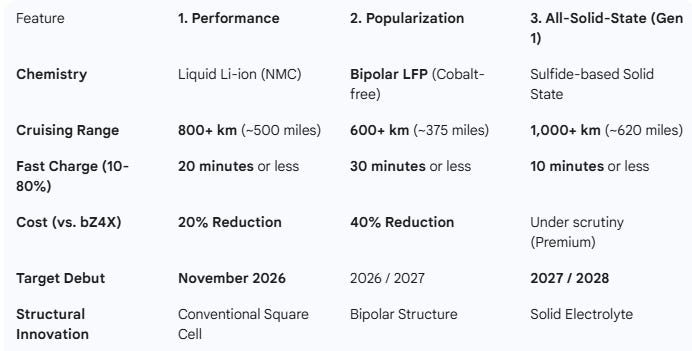

Deadline: To keep this funding, Toyota has agreed to begin the supply of its “next-generation” batteries (initially high-performance liquid cells) by November 2026. The METI grant covers 3 types of Toyota battery products from high performance liquid cells initially, to All Solid State Batteries with the latter being the primary priority for the grant.

Idemitsu Partnership: On January 29, 2026, Toyota’s partner, Idemitsu Kosan, broke ground on a Large Pilot Facility in Chiba. This plant is the backbone of the SSB strategy, designed to produce several hundred tons of sulfide electrolyte annually. Completion is slated for June 2027 (that could support tens of thousands of vehicle battery packs), aligning with the launch of the first SSB-equipped Lexus flagships after that.

While Toyota remains highly secretive about their progress, their most direct public confirmation of on-road testing came with the opening of the Shimoyama Technical Center, a $1.7 billion “development cradle” where 3,000 engineers from Lexus and Gazoo Racing “drive, break, and improve cars.” In briefings during the Japan Mobility Show, engineers confirmed that the solid-state B-samples are the primary technology being “broken” on these tracks right now.

Toyota’s Previous SSB Challenges

The primary reason Toyota missed its earlier 2020 targets was the Solid-Solid Interface.

The Challenge: In a traditional battery, liquid electrolyte flows into every nook and cranny of the electrodes, ensuring constant contact. In an SSB, you are pressing two hard solids together.

Failure Mechanism: During charging, the anode expands; during discharging, it contracts (the “breathing effect”). In a solid system, this repeated movement caused the materials to pull apart or develop microscopic cracks. Once the contact is lost, the battery’s resistance sky-rockets, and it effectively “dies.”

Moisture Sensitivity: These materials (especially sulfides) are so sensitive that even a single drop of humidity in a factory could create toxic hydrogen sulfide gas and ruin the entire batch - they require a clean room process. In 2020, Toyota simply didn’t have a manufacturing process that could handle this at scale.

Subsequent Breakthroughs

Toyota solved these challenges by announcing three specific engineering solutions between 2023 and early 2026:

Flexible Electrolyte: In late 2023, Toyota and Idemitsu Kosan announced a breakthrough in sulfide-based solid electrolytes. Unlike the brittle ceramics of the past, this new material is described as “soft, highly adhesive, and crack-resistant.” It is flexible enough to expand and contract with the battery without snapping, finally solving the durability issue that stopped the 2020 launch.

Bipolar Electrode Structure: Toyota adapted a technology from its nickel-metal hydride (NiMH) batteries. By using bipolar electrodes (where a single plate acts as both anode and cathode for adjacent cells), they can stack the solid layers more tightly. This reduces the internal resistance that previously plagued their 2020-era prototypes.

Strategic Cathode Partner (Sumitomo Metal): In October 2025, Toyota formalized a partnership with Sumitomo Metal Mining to produce a “highly durable cathode.” This material is engineered specifically to prevent the chemical degradation that occurs at the boundary where the cathode meets the solid electrolyte which was a major failure point in their early-decade tests.

The B-Sample Process

Toyota’s B-sample process involves testing these flexible electrolytes in Lexus-bodied “mules” at their Development and Technical Centers.

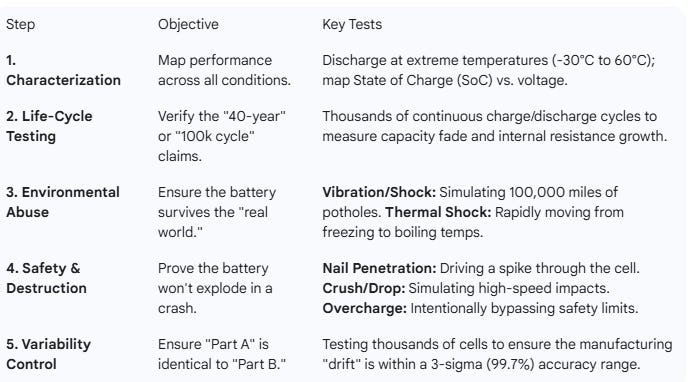

Verification Goals: They are proving the 40-year lifespan claim through accelerated aging tests involving worst-case scenario conditions: extreme thermal cycling, vibration tests, high charging and discharging rates and 100% depth of discharge while analyzing the slope of the battery degradation curve. If the B-samples maintain 90% capacity after this, Toyota would likely trigger C-sample verification in 2027.

At the 2025 Japan Mobility Show, Toyota engineers presented a graph comparing the capacity retention of their current Gen 1 Sulfide SSB against their best-performing liquid-electrolyte (NMC) cells.

Liquid-Ion Curve: Shows a traditional “logarithmic decay.” There is a sharp drop in the first 100 cycles as the SEI (Solid Electrolyte Interphase) layer forms, followed by a steady downward slope that typically hits the 80% “end of life” mark at roughly 1,500 to 2,000 cycles.

Toyota SSB Curve: The slope presented was nearly horizontal. After the initial “break-in” cycles, the capacity retention remained above 95% even after 2,500 cycles of accelerated testing.

The 40-Year Calculation: By extrapolating this linear slope, the industry math suggests it would take over 10,000 cycles (the equivalent potential of 40+ years of daily driving) to hit the 90% capacity mark.

The Risks: The primary risk is manufacturing yield (uniformity, contamination, errors). Producing a “perfect” sulfide cell in a lab is one thing; maintaining that perfection in the pilot plant without moisture contamination remains the ultimate engineering hurdle. There are also structural and mechanical risks they need to prove up (eg vibration table testing, lightweight battery pack pressure systems and interface delamination avoidance). While A-samples will have been tested for dendrite formation, this needs to be re-proven for B-samples made on production lines.

B-Sample Testing:

Toyota’s Bridge and Scale Strategy

An interesting point of Toyota’s new battery strategy, encapsulated in the grant application, is that A-SSBs are the intended end point however they are launching liquid Li-ion batteries alongside to scale up the infrastructure of their EV program and hit the METI grant financial deadlines. The clean rooms and automated stacking systems that are designed for the early batteries are modular allowing them to pivot to SSB mass production as they get the cost down. ie The METI grant is based on the SSB technology but liquid electrolyte battery plans bridge the gap, secure the funding and facilitate the infrastructure that will be used ultimately for their end goal. Their product pathway is as follows:

That strategy is at the core of getting the cost down for ASSBs (experience curve and shared infrastructure) ahead of what would otherwise be possible if they eschewed liquid batteries entirely. It also de-risks the strategy should further technical challenges be met in the SSB timeline to mass production. The last point is that Toyota has already teased further plans for a Gen 2 SSB with 1200-1500 km range.

Conclusion on Toyota

The key point here is that finally an All Solid State Battery project has exited A-sample and moved to B-sample testing with battery design being locked, pilot production lines being constructed, material capital being deployed and wide scale evidence of real world progress and testing.

Examination of Toyota hiring ads and announcements shows a focus on clean room specialists, battery manufacturing engineers “to support manufacturing trials”, production engineers for “battery manufacturing equipment” and “Quality and Root Cause” roles all of which demonstrate a move from the lab (researchers) to a mass manufacturing focus. Many of these roles are initially targeted at the high performance liquid ion battery site but are roles that will rotate experience and learnings into the later All-SSB program as it proves and scales. Setbacks can and likely will still occur, however Toyota have demonstrably moved into a entirely new phase in their plans which will accelerate from here under the published and financially motivated deadlines.

Factorial Energy

While Toyota builds its own international supply chain and battery program, the Boston-based Factorial Energy has achieved what was once thought impossible: getting a startup’s battery into programs across the world’s largest automakers simultaneously.

Factorial’s FEST vs. Solstice

Factorial’s leadership is based on a “Dual Product” strategy (akin to Toyota’s new multi-product roadmap) that allows them to be relevant today while securing the future.

FEST® (Factorial Electrolyte System Technology): A quasi-solid-state battery. It uses a very small amount of liquid electrolyte combined with a solid polymer. This is their “Near-Term” product.

Solstice™: Their all-solid-state (ASSB) program. This is a sulfide-based system that uses a proprietary dry cathode coating process, eliminating energy-intensive drying ovens and toxic solvents.

Architecture and Breakthroughs

Unlike Toyota’s focus on fairly rigid sulfide ceramics, Factorial’s FEST (semi-solid) uses a polymer-based hybrid.

The Breakthrough: They solved the “Interface Problem” Toyota also experienced by using a lithium-metal anode with a polymer bridge. This allows for a 375–391 Wh/kg energy density, nearly double that of current LFP batteries, but lower than the 450+ Wh/kg of Toyota’s ASSB program, without the brittle-cracking risks of pure ceramics.

Manufacturing Prowess: Factorial’s most significant achievement is a claimed 80% compatibility with existing lines. Their batteries can be made using (mostly) existing lithium-ion factory equipment, making them potentially the most “scalable” solution on the market.

Factorial’s “Record-Breaker” Road Test (September 2025)

The most significant result from the Mercedes B-sample validation phase on Factorial FEST systems so far is a real-world endurance drive:

The Vehicle: A “lightly modified” Mercedes-Benz EQS.

The Route: Stuttgart, Germany, to Malmö, Sweden.

The Result: The car covered 1,205 km (748 miles) on a single charge.

Efficiency: It arrived with 137 km (85 miles) of range still remaining in the pack. This performance surpassed Mercedes’ own Vision EQXX record, effectively proving that the FEST® (semi-solid) chemistry can deliver on its energy density promises in a full-sized luxury sedan.

Technical Validation Highlights (Early 2026)

Beyond the range record, Mercedes has disclosed specific technical “wins” from the B-sample torture tests:

Thermal Stability: Factorial’s cells remained stable at operating temperatures exceeding 90°C (194°F). This has allowed Mercedes to experiment with passive airflow cooling, potentially removing the weight and cost of heavy liquid-cooling pumps and radiators in future production models.

The “Floating” Carrier: To solve the “breathing” problem we discussed (expansion/contraction), Mercedes patented a pneumatic actuator system within the battery pack. This system physically adjusts the pressure on the cells as they charge and discharge, ensuring the solid-state interface never loses contact which is a key hurdle that caused earlier prototypes to fail.

OEM B-Sample Timeline

Factorial is currently managing one of the most complex validation programs in the automotive industry:

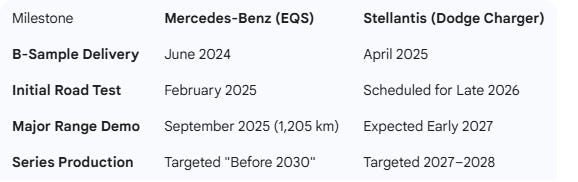

Mercedes-Benz: Seemingly a clear leader. Mercedes received B-samples in June 2024 (of the FEST semi-solid solution). With completion of the road test, Mercedes is currently finalizing the C-Sample specs for a limited series rollout in 2027.

Stellantis: B-sample validation for the Dodge Charger Daytona began in April 2025. A 20-car “demonstration fleet” is reportedly currently being built for public road testing in late 2026.

Hyundai-Kia: Following an $800M investment, Hyundai will open its Uiwang Pilot Line in March 2026 to build Factorial-designed B-samples for the Genesis flagship (initially FEST and moving to Solstice eventually).

Karma Automotive: Announced in February 2026, the Kaveya super-coupe is targeted to be be the first “retail-ready” vehicle to use FEST batteries, targeting a late 2027 customer delivery date.

As of mid-February 2026 however, the B-sample phase for the Hyundai-Kia and Factorial partnership is the nearest major event to further prove their products. Good outcomes here will support Factorial’s IPO ambitions.

Uiwang “Dream” Line: Opening March 2026

The most critical milestone is the official opening of the Next-Generation Battery Research Center in Uiwang, South Korea, scheduled for next month (March 2026).

The “Dream” Battery: Hyundai has internally branded their in-house solid-state project as “Dream” but it is based on Factorial’s technology. The Uiwang facility houses a dedicated pilot production line specifically for these cells incorporating Factorial battery IP.

Full-Scale Pilot Production: Starting in March, this line will move from “setup” to full-scale pilot production, churning out the B-samples required for vehicle integration. This advanced timing is achievable because Factorial’s technology is designed to be able to integrate with existing battery manufacturing equipment.

Global Interest: Notably, representatives from GM are expected to attend the opening ceremony, signaling that Hyundai / Factorial’s joint progress is being monitored by other major OEMs as a potential benchmark for their own “battery independence” strategies.

Factorial’s hiring spike in South Korea (managerial and senior engineering roles in Cheonan-si) seemingly indicates that B-sample validation is currently tackling high-current discharge stability.

The Goal: To move from 100 km/h cruising to “Performance” metrics. Hyundai is testing if these cells can handle the aggressive 4C discharge rates required for their N-Brand or Genesis performance models without the “breathing” issues that cause physical delamination.

Thermal Management: Spy shots from earlier this month confirmed that Hyundai is running Ioniq 9 and Genesis GV90 mules in sub-zero conditions to validate Factorial’s claim that their electrolyte maintains stability down to -30°C.

Factorial operates under a royalty, technical service fee and material supply model for this Hyundai/Kia venture.

Timeline to Commercialization

Despite the “Dream” line opening, Hyundai executives (notably Kia’s head of product planning) have cautioned that while B-sample testing is successful, mass-market commercialization is still targeted for 2030.

Phase 1 (2025-2026): Small-scale pilot production (Uiwang).

Phase 2 (2027-2028): Introduction of “First Prototypes” to the public and limited series validation.

Phase 3 (2030): Full commercial rollout.

Factorial’s Mid-2026 Planned IPO

To fund the transition from B-sample to mass production, Factorial announced in Decemeber 2025 a definitive merger with Cartesian Growth Corp. III (CGCT), a SPAC valuing the company at $1.1 billion.

Ticker: Expected to list on the Nasdaq as FAC in mid-2026.

The PIPE: The deal includes $100 million in fresh capital and $276m of trust cash (subject to any redemptions in CGCT), which will be used to scale their Methuen, MA production facility and support the Hyundai / Stellantis pilot lines.

Conclusion

I understand historical skepticism regarding SSBs given how long they have taken to move into on-road testing, however hopefully I’ve presented enough hard evidence that demonstrates that “this time its real”. Toyota and Factorial cells are both on roads and tracks racking up miles driven. Initial production facilities are rising out of the ground now. Large scale capital has been committed to production plans, not just R&D. This all changed in late 2025.

The prior delays were all in the lab. Chemical, technical challenges that together took longer to solve, reinforcing how physical constraints to energy density are real but also making the IP head start that the leaders have developed, highly valuable. From semi-solid solutions to All Solid State battery programs, particularly at Toyota and Factorial, there’s mounting hard evidence that these programs have moved into a very different phase with a much clearer path now to mass market commercialization.

Getting to the mass market will take time. For ASSBs, companies are targeting 2030 to get manufacturing costs down through the experience curve, scale, yield and further material science - but that’s only 4 years away. In the interim, semi-solid batteries will hit the road with vastly increased range and longevity and reduced charging time over LFPs. Given those aspects remain the largest impediments for EV adoption amongst consumers, it seems clear that SSBs will change the automotive landscape again in the near future.

A Note on other North American SSB Companies

I have not focused here on QuantumScape or Solid Power. Both are, in my view, arguably somewhat behind Toyota and Factorial (to differing degrees and in different ways) - this is a personal conclusion based on my research and is admittedly somewhat subjective.

QS is just generating test mule real world drive data now in passenger vehicles whereas Toyota had already submitted validation data to the Japanese government showing the technology’s performance in a vehicle environment in order to receive their massive grant. From that perspective, Toyota could be stated to be in late stage B-sample validation whereas QS might be considered to be earlier in the same stage. Factorial cells have completed a long range test drive with Mercedes albeit they are semi-solid cells with lower energy density than SSBs. QS ASSB battery specs are also below Toyota’s across the board. It is worth noting though that QS has committed to the same commercial launch timeline as Toyota (2027/28) and is shipping test cells to VW as shown in their revenue line.

Solid Power appears to still be in the A-sample to B-sample transition.

Competitive Intelligence out of China

China is not sitting out of the SSB industry as it clearly represents a huge challenge for their massive Li-ion battery manufacturing infrastructure. While progress is far more opaque, Dongfeng and FAW Group announced this month (Feb 2026) highly aggressive timeframes. They have indicated that they have already begun installing 500 Wh/kg semi-solid batteries in test vehicles with a target for mass production as early as September 2026. This puts immense pressure on the Hyundai-Factorial alliance to accelerate their B-sample to C-Sample transition while also reinforcing the lack of testing done in some Chinese companies. Of course, these are semi-solid, not ASSBs.