The Last AI Upgrade....Why Nvidia's result might signal the end of the AI bull market

Nvidia’s result on the 26th might be a bumper one, but it may not matter.

Is the headline of this article clickbait? I certainly don’t intend it that way. What I am seeing in the last 2 weeks is reminiscent of the end of past bull markets and I think it important to highlight the significance of these developments. I invested through both the end of the US tech boom back in 2000 and the China infrastructure boom in 2010 and there are fundamental parallels today in the AI ecosystem that are rhyming very strongly. Here I connect the disparate dots on important news that has only come to light in the last few of weeks that together paint a clear picture and warrant caution.

This is an important note. Share it around and if you haven’t already, then subscribe for further updates as developments evolve:

A couple of days ago OpenAI quietly walked away from their $1.4 trillion AI infrastructure spending plans. Whether through investor pressure in order to secure a reported $100bn equity raise or simple realization that they would never be able to fund the spending, that spending plan is now reduced to $600bn out to 2030 - a massive 57% or $800bn reduction. I suggest here that there are multiple reasons this has occurred and that taken together they are an important signal that lasting market regime change is upon us.

Here’s the thing: This could spell the end of the “seemingly endless” upgrade cycle for the AI ecosystem.

Lets pull together the pieces of the puzzle…

OpenAI - the largest AI infrastructure customer out there has cut spending plans 57% or $800bn. When they were increasing their spend they trumpeted it with fanfare, stood beside the President and proclaimed their omniscience. This massive about face has by comparison occurred very quietly. The amusing thing about this cut is that OpenAI has been at pains in their raising documents to point out the “linear” relationship between compute growth and their revenue. However, to support the valuation, they have upgraded their outer year revenues while cutting compute spending by nearly 60%. Does this sound internally consistent? I guarantee that those investing in this round have completely disregarded OpenAI’s long term revenue forecasts, as should we.

SaaS stocks, a major sectoral driver of enterprise AI demand have seen their stock prices fall 35% on average from the 2025 peak on AI fears with some down 60%. This cuts off an avenue of capital and limits their ability to spend. While the majors like Adobe have fortress balance sheets and can keep R&D spend going, the collapse in EV/Sales multiples means many smaller companies are effectively frozen out now as they would likely need to raise in a down round. Without the next raise, cash burn kills them and VC / PE freezes investment into others. That drives an eventual reduction in AI / Cloud services demand. It will take time, but the implication of this market repricing will be seen this year in the demand curve.

IGV Chart: iShares Expanded Tech Software Sector ETF

Software company debt offerings have collapsed as corporate spreads in the sector have ballooned, reflecting increased probability of default. This limits a second source of capital for AI spending and more importantly particularly impacts the developed businesses (less reliant on equity funding, more on debt) that are more material to AI demand growth.

NVIDIA, OpenAI’s major backer and key supplier, cut its original appetite for investments in OpenAI from $100bn (medium term commitment) to “up to $30bn” in this latest round, signalling unease with the concentration and duration risk inherent in OpenAI’s unfettered growth strategy and potentially also the success of their competition.

Blue Owl Capital, a major AI infrastructure financier and private credit fund manager at the center of many large scale, creative AI and software financing deals has been forced to halt redemptions in a retail private credit fund due to the illiquid nature of the collateral and escalating redemption requests. Blue Owl has seen its share price fall nearly 60% since its early 2025 peak, signaling counterparty risk that effectively prevents another source of capital to the AI ecosystem from one of the most aggressive financiers. The contagion from this has extended to KKR, Ares, Apollo and Blackstone so is affecting the main private financing ecosystem. The potential implications of this for the industry are best seen in contingent follow on events such as if Meta has to cut its JV arrangement with Blue Owl delaying its $30bn Hyperion data center project and so on with many other data center expansions.

Stargate becomes a white elephant: The $500bn Stargate project has effectively stalled only months after being expanded to an additional 5 mega data centers, with the venture reportedly remaining dormant, lacking staff, and failing to develop infrastructure as originally planned. The partners can’t agree over control and structure. SoftBank, one of the 3 major partners reportedly struggled to present a viable financial model and secure funding, and potential lenders balked at the risk. OpenAI failed to convince their lenders of their self build strategy with lenders concerned at backing a high cash burn company and Oracle’s credit position deteriorated significantly since the original announcement (Oracle CDS pricing, which insures against default, now at the highest since 2009). Now OpenAI has had to pivot to smaller scale bilateral developments with clearly lower expansion spending (hence their reduced spending “targets”). Again, the seeming absurdity of upgraded 2030 revenue forecasts when they will have less compute and data center capacity than their prior plans, stands out here clearly.

Chinese LLMs are stealing capabilities from Frontier US models at a fraction of the cost of self development. We’ve all heard of Deepseek’s success at building a low cost, high reasoning LLM. Then there was Kimi and even more recently Minimax. Now Anthropic, OpenAI and Google have all disclosed this week that the Chinese LLMs have been distilling their models as training data to support their low cost developments that offer API prices at 1/6th to 1/20th the cost of US LLMs. The press release below (link at end) from Anthropic only a day ago highlights the vulnerability and questionable long term economics of the US Frontier LLM premium infrastructure models. When competitors can seemingly just steal your data and build a replica for 1/100th the cost, is there any moat to speak of? AI startups are using models like Deepseek to build their capabilities due to its price/value offering. Companies that have chosen to partner with the high cost models will increasingly be forced to question whether the value they are extracting is sufficient when alternatives exist that are a fraction of the cost. Large corporates may not trust Chinese AI, but what if the next Deepseek actually comes out of the US? (hint: its already happening with Reflection AI). In a normal industry, massive capital requirements form a barrier to entry. Here it simply appears to be a tax on those creating the real IP that others can take advantage of. That’s not sustainable and would play out in medium term revenue growth forecasts being missed and infrastructure spend being slowed (wait - hasn’t OpenAI already “opened” that door?).

The Hyperscalers: The last domino to fall may be the AI infrastructure plans of the hyperscalers. Amazon, Alphabet, Meta and Oracle have all upsized their intended Capex plans in recent earnings reports. However, it will not surprise me to see these plans also wound back, like OpenAI’s, at some point this year. There’s 2 factors that may drive that:

a. Demand growth: There is no doubt demand growth has exceeded these companies internal projections so far. Google Cloud’s 48% revenue growth rate in their Q4 result is a case in point. However, their infrastructure plans are a 2nd derivative of their RPO growth. When capital stalls, customers can’t expand as fast and cant commit to as much future spending. Pretty quickly, RPO growth stalls as customers wind back orders and the hyperscalers would be forced to cut capital expenditures. How can they get it so wrong you ask? Just look at the e-commerce companies during COVID. They all extrapolated order growth rates into infrastructure expansions that eventually exceeded demand and had to be wound back. Amazon was a poster child for this in 2022 and 2023 with its earnings estimates having to be cut by 50% due to costs accelerating upwards as revenue growth stalled. Why does this happen? Its because large scale infrastructure takes time to develop and commission. These companies have to extrapolate today’s RPO growth into the infrastructure needs 2 years from now given development timelines. However revenue growth can evaporate quickly as the back-end of COVID showed.

b. Capital Markets: The financial markets have a way of disciplining companies they believe are overextending themselves. OpenAI didn’t just voluntarily cut its spending plans by 60% only a few months after trumpeting $1.4 trillion because they woke up on the wrong side of the bed. It was most likely forced upon them as a condition of raising the capital they need right now. This is the power of financial markets.

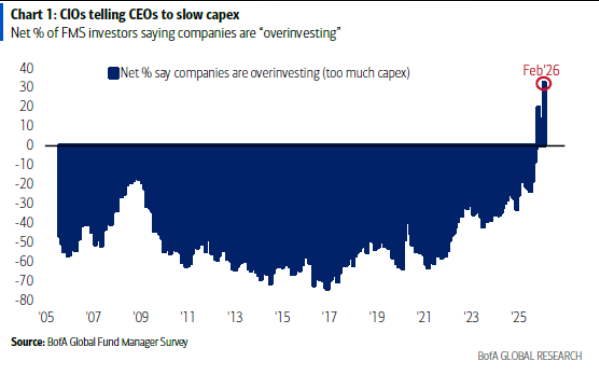

That chart above from BofA’s’s fund manager survey tells you that equity markets are now telling companies to wind back investment. For the first time in 20+ years, CIO’s are telling CEOs they are overinvesting. If the companies don’t listen their shares will be sold and that forces a decision upon the board of directors. Nine times out of ten, companies will end up reducing their spending. I see this now as THE central scenario in 2026 as the year progresses. Amazon’s $200bn capex budget will be lower by years end. Alphabet’s $180bn will be lower by years end. Meta’s $125bn will be lower by years end. Why? Because their shares will be sold until they respond. The market (as shown in the FMS chart above) has now spoken.

So what about Nvidia’s result on the 26th Feb? My personal belief is that they will beat across the board and present a very upbeat outlook. How could they not? Amazon, Google, Meta, Oracle and even OpenAI are all spending vastly more under current plans than they did in 2025 and scrambling over each other to secure Blackwell and Vera Rubin chips.

However I don’t think this will matter.

The regime change is upon us. Now, AI spending is bad, long term AI unit economics are rightly in question and a vocal and growing contingent even believe OpenAI won’t survive an industry reset. Back in 2010 with the China infrastructure boom there was a similar dynamic. Materials and mining services companies still had record order books and were beating consensus estimates and forecasting further growth. However in the background there was increasing focus on Chinese ghost cities, roads and bridges to nowhere and supply growth in critical materials catching up and exceeding demand at some future point. The result - companies, even the highest quality ones, started to de-rate. First the multiples started to contract and eventually a year or so later, real earnings downside appeared. Investors were scratching their heads - “this company is beating so why isn’t its share price going up - its cheaper than ever”. Nvidia is already showing this dynamic. Despite bumper demand growth conditions and a forecast acceleration in revenues and earnings over the next 2-3 quarters as Blackwell ramps and Vera Rubin gets launched, the stock has been a sideways bet.

This is not because Nvidia is misunderstood or being missed by the market. There couldn’t be a stock that’s more followed or better known. Its a signal of regime change that should be taken note of. Stocks can surge on headline results and then be met with a wave of selling as holders are all pre-loaded to “take advantage of the catalyst”. That is a potential scenario that must be considered. And if Nvidia starts to fall, then the entire AI ecosystem of stocks will suffer.

I do not mean to be all doom and gloom. However, I am highlighting a pattern I have seen before and cross referencing the data points that have recently arisen that suggest the worm has turned.

Good luck out there.

Andy West

The Inferential Investor

References:

https://www.anthropic.com/news/detecting-and-preventing-distillation-attacks

https://mlq.ai/news/software-firms-delay-debt-issuance-as-ai-disruption-fears-elevate-lending-rates/

https://www.ft.com/content/dea24046-0a73-40b2-8246-5ac7b7a54323

https://www.theinformation.com/articles/inside-openais-scramble-get-computing-power-stargate-stalled

https://www.bloomberg.com/news/features/2026-02-22/blue-owl-redemptions-halt-intensifies-private-credit-fears