The Agentic Dividend: Stocks Leaning Most Aggressively into Agentic AI Labor Cost Reductions

19 case studies on agentic AI deployment across stocks encompassing over 50,000 announced headcount cuts. Which industries and companies stand to benefit the most?

By reading this article, you acknowledge the terms of our full legal disclaimer. The information provided herein is for educational and general informational purposes only and does not constitute professional financial or investment advice. Discussion of any stock within this report is only for the purposes of highlighting the company’s plans in agentic AI and does not convey any investment recommendation.

Agentic AI

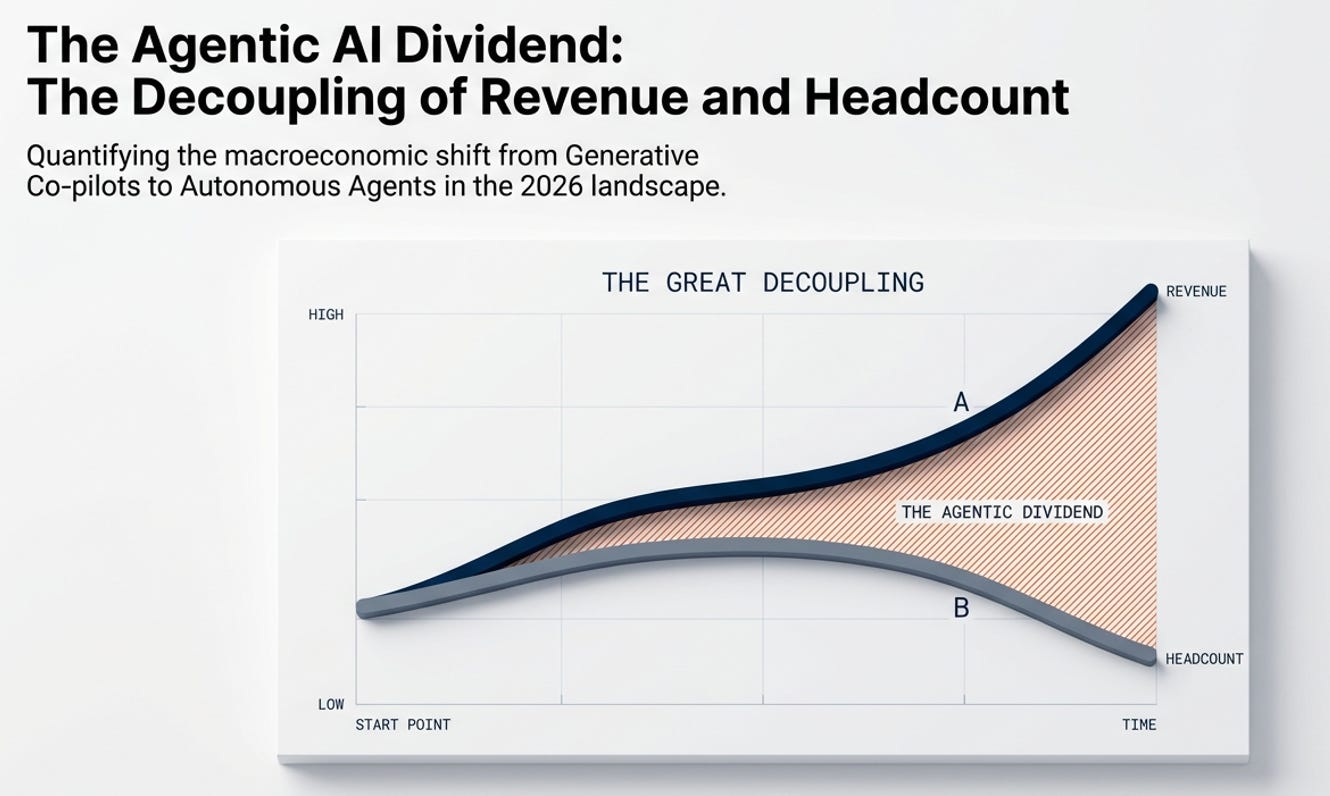

The first wave of AI changed how people worked. The next wave may change how many people are needed to do the work.

Only a few months ago, agentic AI was still an obscure term, albeit rising in frequency in company disclosures. Now with the recent earnings reports of software and fintech companies like Wisetech Global and Block, both of whom have announced 30%+ headcount reductions across their businesses linked to the technology, investors must actively get up to speed on how agentic AI may shape a company’s operating model, margins and earnings growth going forward.

The initial AI chatbot phase largely revolved around assisting employees with writing, summarizing, searching, and answering questions. Agentic AI in contrast is increasingly being deployed to take on end to end workflows within businesses. Examples include dealing with customer issues, handling back-office tasks, writing code, and undertaking multi-step processes with minimal human supervision. This recent change shifts AI from being a productivity tool used by staff to something much closer to a replacement for staff in certain functions. The strategic question for companies has become whether AI can allow the business to operate with fewer people, different people, or a fundamentally different cost base.

That is why the companies leaning hardest into agentic AI are now attracting attention. The payoff is potentially significant if companies can deploy the technology in place of 30%+ of certain workforces: lower support and administrative costs, better operating leverage, flatter headcount growth, and a more powerful translation from revenue into margin and earnings. Block rallied 20% following its announcement and Wisetch Global rallied 18% signifying at least initial positive surprise from the extent of the labor cost reduction opportunity.

At the same time, many of these companies are leading the way because they have been forced into early adoption due to threats to their traditional business models from artificial intelligence. Block had fallen 35% and Wisetech over 40% since November as the SaaSpocalypse gathered attention. Other examples in this report are down 60% from their peaks. This is the opportunity and risk for investors in stark focus: those stocks targeting the largest and most aggressive margin opportunities from agentic AI are also the ones whose share prices have often fallen the most due to the perceived AI threat. Successful execution may well see share price rebounds while botched execution could damage the stocks further.

This year, the evidence on agentic AI has become far more tangible. Public disclosures now show management teams moving beyond pilot programs and into redesign of their workforce. This trend was highlighted in the recent hyperscaler earnings calls from Microsoft, Alphabet, and Amazon who can see the rate of agentic AI adoption amongst their cloud services customers. Examples explored below show Salesforce cutting 5,000 customer service roles, Wisetech removing 2,000 staff representing 30% of their workforce and Block going even further, announcing 40% cuts across the entire organization. When companies are finding ways to remove a third or more of organizations or divisions, we are in a new paradigm.

However large scale workforce redesigns on the back of an entirely new technology brings real risks. Just as the businesses in the case studies are finding ways to remove labor, so too are their customers using agentic AI. That means that, particularly in business to business industries, many revenue models may have to evolve from proven seat-based subscriptions to more variable consumption pricing which can alienate customers, customer experience can deteriorate, internal morale can fracture as workforces are reshaped, and operational errors can rise before efficiencies actually materialize. The upside is compelling, but so is the execution risk. In the agentic era, the winners may not simply be the companies adopting AI fastest. They are more likely to be the ones that can redesign their labor model without breaking their product, their culture, or their economics.

This article is written for two audiences. First it is structured into industries to show readers with a general interest in the topic, where agentic AI pressure will appear on workforces and functions. Second, it is for investors, to demonstrate which stocks are leaning in the most, which industries have highly material margin opportunities and those where the impact may be may be more muted and longer dated. In specific cases I also attempt to highlight where these initiatives are mostly a defensive measure to offset structural headwinds.

The only way to assess progress on agentic AI adoption and benefits in the era of a new, unproven technology is to identify the adopters, specify the KPIs and monitor their progress through their earnings disclosures. The KPIs are clear: normalized (ex restructuring) labor cost / revenue ratios, gross and operating margins, revenue per employee, R&D / revenue ratio, customer review sentiment checks, net promoter score trends. These metrics are where progress will be shown or disproved.

Here are the companies that, based on the most recent public disclosures since late 2025, are targeting the most aggressive agentic AI implementations or disclosing the most tangible financial targets:

Enterprise Software / SaaS

Salesforce (NYSE: CRM)

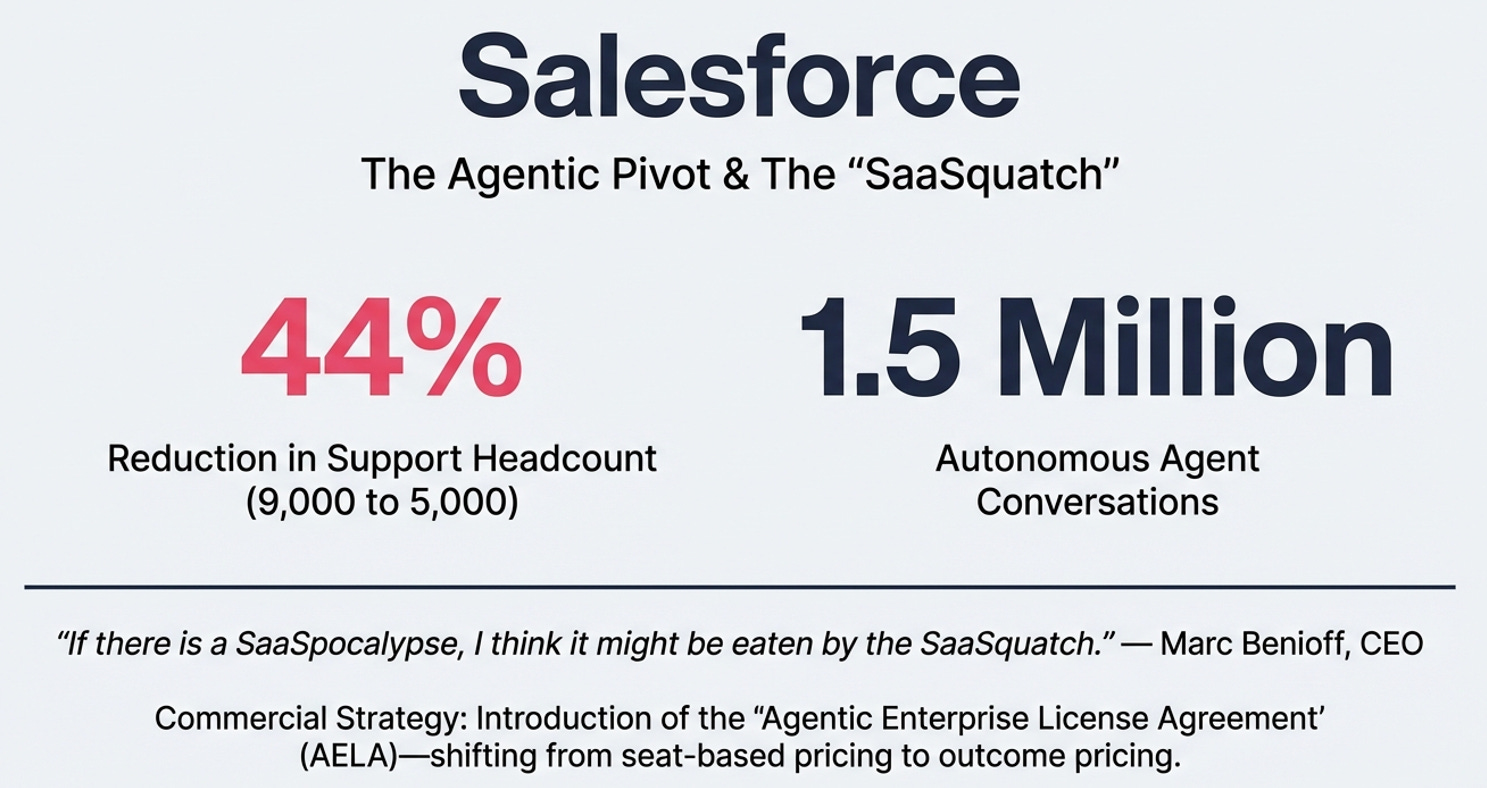

Salesforce presents itself as a clear example of a software company using agentic AI both defensively and offensively. On the defence side, it is applying Agentforce internally to reduce labor in customer support, where the company says the system is handling roughly 1.5 million incoming queries while achieving customer satisfaction levels that are “nearly identical” to human service levels. Offensively, it is using the same technology to transition its organization away from seat-based subscriptions, toward charging for autonomous digital labor. This represents a wholesale change to the way the company does business. Knowing that agentic AI allows its customers to complete the same work with fewer human seats which reduces the revenue potential for Salesforce, they are simultaneously using the technology to lower their cost base while shifting to a revenue model that is less reliant on seat based pricing.

The labor implications are already material. Recent disclosures state that Salesforce reduced its customer support workforce from 9,000 to 5,000 people, a 44% reduction with a further 1,000 job cuts across the broader company in early 2026. Management linked those changes to Agentforce-driven initiatives. For a business where internal staffing has traditionally scaled with customer count, this is a meaningful structural shift in the operating model.

The financial read-through highlights the impact on the bottom line. Company guidance projects an FY2027 non-GAAP operating margin of 34.3% up from 34.1% in FY26 and 33% in FY25. Shedding 5,000 total roles on an average assumed salary of $50,000 is a $250m tailwind which equates to a 40bps margin bump, presumably offset by 10-20bps of compute and other agentic AI operational costs such as AI engineers in replace of teams of customer service staff. Consensus is forecasting further margin gains over the following 2 years as well that accelerate in magnitude, however given more tepid revenue growth rates being achieved by Salesforce (than market expectations for an AI driven acceleration), it remains to be seen whether these targets can be achieved.

On the revenue side, the company’s introduction of their Agentic Enterprise License Agreement (AELA) is management’s strategy to underpin future revenue growth in a world where its customers may also have fewer staff, Salesforce wants to charge for agent interactions, tokens, and outcomes instead of seats. This is the shift to consumption based revenue generation, much as Adobe has implemented into its business model, in response to both the threat and opportunities presented by AI agents. However as we have seen so far with Adobe, consumption pricing has failed to deliver an acceleration in revenue growth with seat based cannibalization eating away at it from the other side. The transition may ultimately be quite protracted.

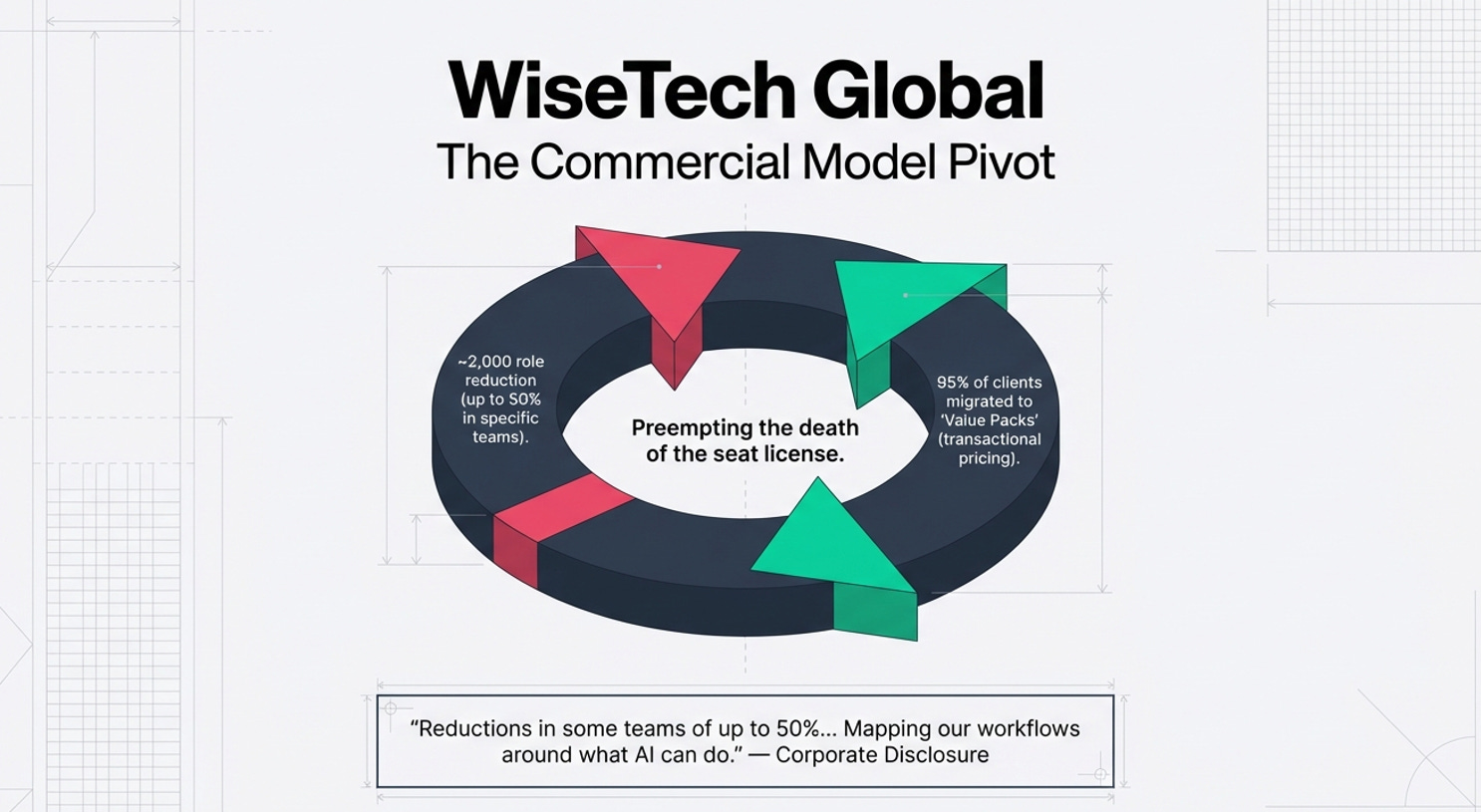

WiseTech Global (ASX: WTC)

WiseTech Global shows that the agentic threat (and opportunity) is also being recognized outside the US. Like Salesforce, Wisetech is a business to business software company focused on the logistics industry and has announced a major redesign of both its workforce structure and its revenue model for the agentic era. Internally, the company has deployed agentic AI across its business functions that traditionally employed 7,000 staff. These agents include its CargoWise Agent “ACE,” automated document handling, and AI classification assistants. Externally, it has forced 95% of its customers onto CargoWise Value Packs which abolish traditional seat and user pricing in favor of consumption-based pricing tied to logistics execution (eg container bookings) and productivity.

The parallels with Salesforce’s strategy are not accidental. Specialized process software faces an existential issue if its AI led product advancements make customer employees redundant whilst revenues are still relying on paid seats. Adobe is a much debated example of this dynamic. WiseTech’s answer is to migrate away from seat pricing before that deflation becomes particularly painful and to take advantage of the operational benefits at the same time by replacing human labor with agents. This makes WiseTech one of the most important case studies in how software companies can protect revenue while also reducing their own cost base.

On labor, the scale of the program is far more aggressive than Salesforce. The internal program targets up to 50% reductions in product, engineering, and customer service teams and is expected to result in roughly 2,000 roles being removed across FY26 and FY27. This is nearly one-third of the company’s entire workforce. Because R&D and customer support are labor heavy cost lines in SaaS, the margin implications are material. Total Selling, General and Administrative expenses plus R&D expenses run at approximately 40% of Wisetech’s revenue. These are the cost pools where Wisetech is targeting to remove over 30% of the headcount.

WiseTech therefore sits among the most assertive and far reaching AI-first cost base resets, alongside Block (see Fintech section). Few companies are simultaneously attacking internal resourcing while completely redesigning their pricing architecture to defend against the same staff cost deflation their products help create. The debate among analysts is the opportunity versus the risk. Wisetech discloses in Q&A some customer angst at consumption based pricing changes. It is also likely that workplace cultural aspects play a role in elevating the risks associated with such large scale headcount removal. However at the same time, software businesses are unique. There have been many examples of large scale redundancy programs being implemented in the industry with little interruption to customer experience. Wisetech is a key stock to watch for how agentic programs can impact operations.

C3.ai (NYSE: AI)

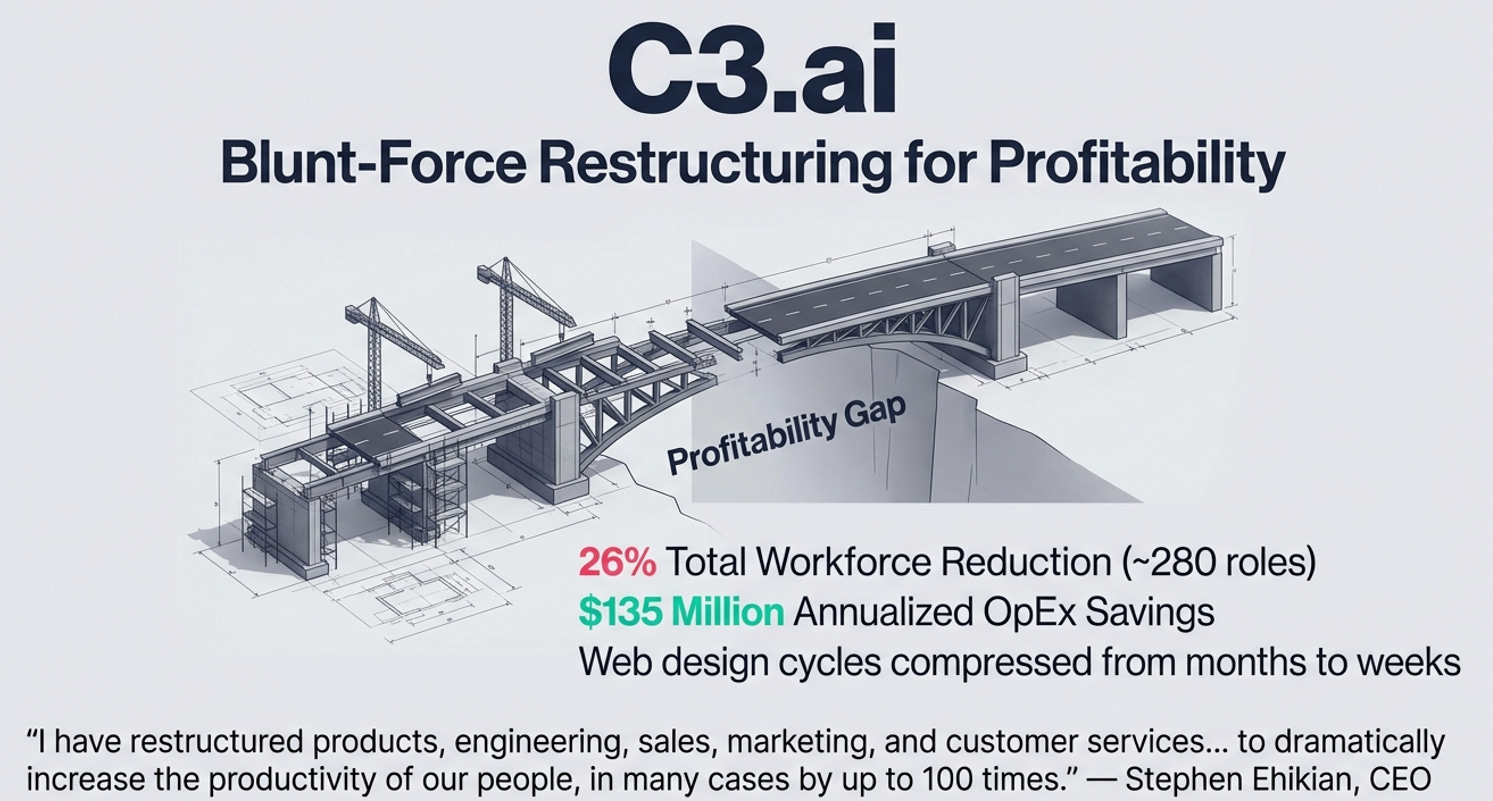

C3.ai represents one of the most financially quantified pure-play agentic restructuring cases announced so far but like many other examples here, is a company where its agentic AI push is defensive with the share price down 90%+ since its IPO. It is a company facing structural headwinds, encapsulated in a reported 46% fall in revenue, with a strategic transition to consumption based pricing proving to be insufficient to offset the loss of old, large subscription renewals. The company claims to have aggressively integrated state-of-the-art agentic AI systems, utilizing Anthropic’s Claude models, across its entire operational footprint to right-size the business. It specifically tied the company’s February 2026 reset as a direct consequence of agentic AI implementation across product development, engineering, sales, marketing, and customer service.

During the Q3 FY2026 earnings call on February 25, 2026, CEO Stephen Ehikian outlined the magnitude of the claimed AI leverage to justify the severe headcount reductions:

● “In the past five weeks, I have restructured products, engineering, sales, marketing, and customer services to leverage state-of-the-art agentic AI across these business entities to dramatically increase the productivity of our people, in many cases by up to 100 times.”

● Highlighting specific departmental efficiencies, Ehikian stated: “we are leveraging agentic AI to design, develop and redeploy our website. This process previously took 9-12 months and many millions of dollars. It will now take weeks.”

● Regarding the software engineering groups utilizing Anthropic’s Claude, he cited productivity increases “by up to two orders of magnitude.”

What makes the case useful is the granularity of the outlined cost savings from these initiatives. The company announced a 26% workforce reduction and cost cuts of $135 million, with roughly $60 million of that tied directly to headcount. Relative to FY2026 revenue guidance range of $247 million to $251 million and a projected EBIT loss of over $224m, the magnitude of the program is extremely large but also clearly necessary. Few companies in my research have articulated such a direct bridge between AI-led restructuring and a path to a materially different earnings picture.

That said, the market remains skeptical. C3’s share price has fallen a further 20% since its earnings report and it is projected to continue losing money for the next 3 years. C3 may need to find further AI led cost reduction opportunities to stem the bleeding. Full savings are only expected from 2H FY2027, reinforcing that agentic AI does not instantly convert layoffs into stable run-rate margin expansion. Workflow redesign, governance, and execution reliability remain important factors.

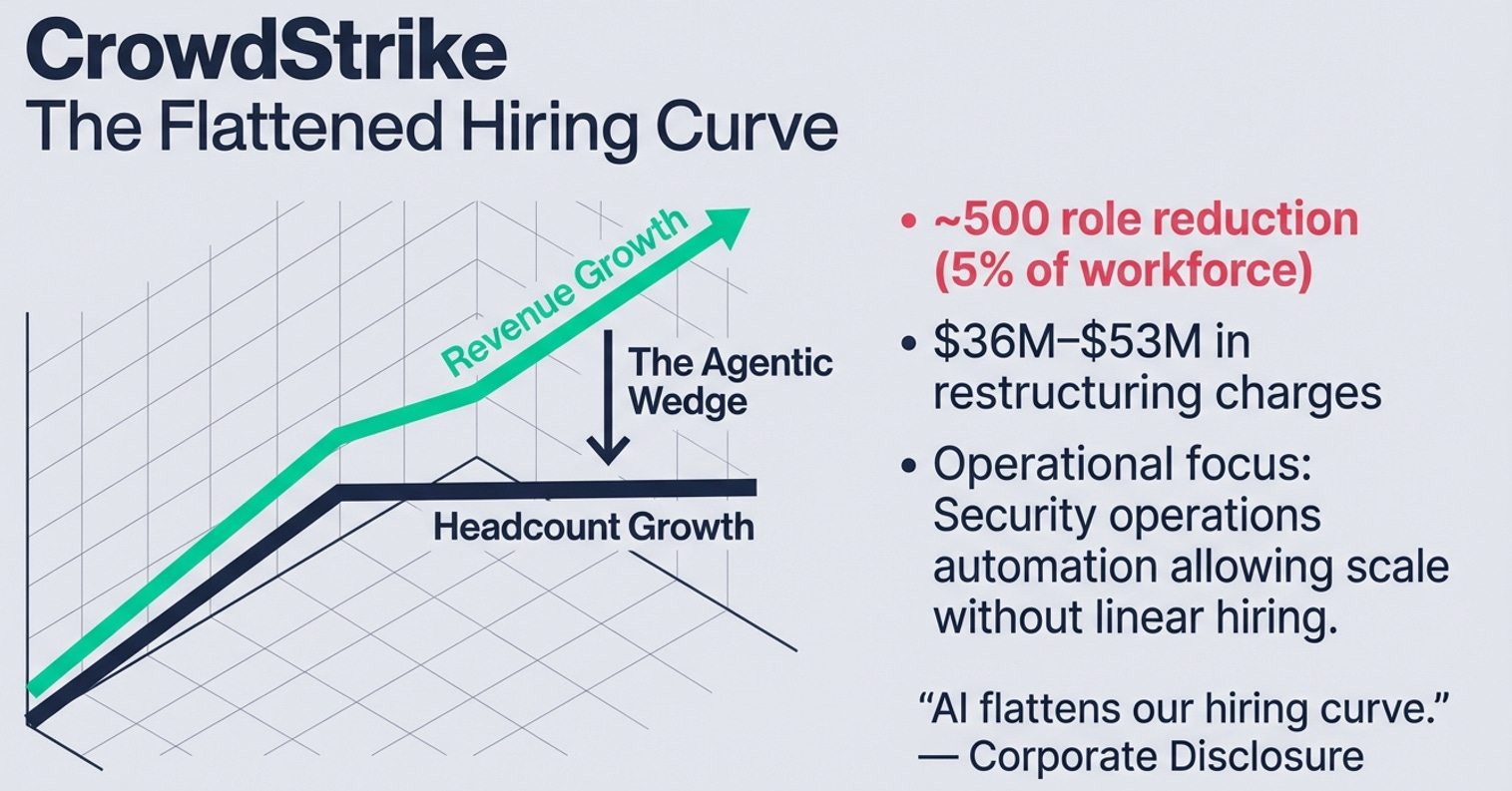

CrowdStrike (NASDAQ: CRWD)

CrowdStrike is a less dramatic but still relevant software case because of management’s characterization of the opportunity for them being a structurally flatter hiring curve rather than a one time labor reset. The company disclosed a reduction of roughly 500 roles, or about 5% of the workforce. A 5% cut is smaller than the most aggressive cases here, but it remains earnings‑material because (a) software security firms are personnel-cost heavy, and (b) management is explicitly signalling reduced future labor growth vs. historical which, if achieved, translates to a multi-year margin expansion opportunity.

While the labor reduction program is modest versus Block or WiseTech,, the underlying message, that AI can allow a fast-growing security platform to scale with lower incremental labor, points to what is likely t be a recurring message across companies as agentic AI is more widely adopted. After 3 years of flat EBIT margins around 21.5%, the market now has Crowdstrike’s operating margin growing linearly to over 27% by FY29 (3 years). This means that the company is projected to achieve an average of 30%+ EBIT growth off 20% revenue growth over that period.

Arguably, with such an elevated multiple (forward P/E of >80x) Crowdstrike needs to achieve this operating leverage and possibly find additional means to exceed it. The stock price is down over 30% since November on the back of the SaaSpocalypse. However, its agentic AI focus is just starting to generate benefits and success may see further programs announced.

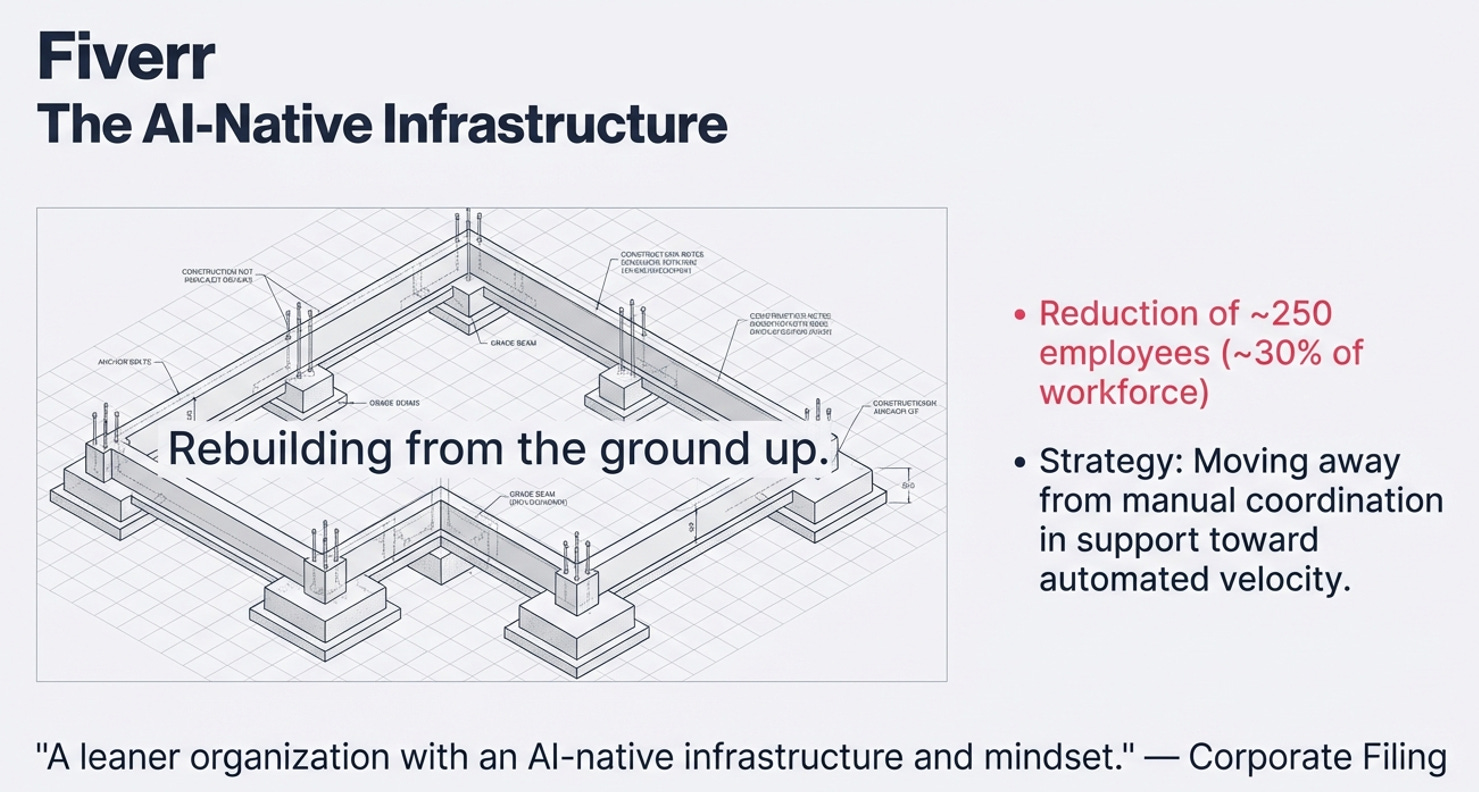

Fiverr (NYSE: FVRR)

Fiverr, a global freelance services marketplace, is another example of a company undertaking a massive transformation on the back of agentic AI automation. As an intermediary to match freelance service providers across areas such as coding, graphics and design and digital marketing with business looking to hire project talent, Fiverr has traditionally operated with a headcount concentrated in business functions such as engineering, marketplace integrity and fraud detection and customer support.

With the stock price down over 60% since mid 2025, the company recently disclosed a reduction of roughly 250 employees representing about 30% of staff. For a platform of its size, the program is bold and suggests that management is betting agentic tools can reliably reduce overhead right across its critical business functions without materially impacting the value proposition. Corporates need to be matched with pre-vetted, experienced and reliable project talent while freelancers need to trust that Fiverr’s corporate customers are trustworthy. Automating these functions successfully would mean that Fiverr can grow with less incremental overhead.

Company disclosures frame this strategy as a medium term transformation with visible benefits appearing over 4-6 quarters (to mid 2027) around their concept of “AI native infrastructure”. Savings from the headcount reductions are being partially reinvested in AI focused engineering talent to rebuild the architecture of the platform from the ground up. Analysis of job ads show aggressive hiring of AI and machine learning experienced engineers and data specialists. The CEO has likened this transformation as going back to start-up mode to completely re-envision the organization as one where AI agents, rather than human account managers, handle the orchestration of high value, more complex projects including involvement in the brokering of the contract. The last point is important. In a segment where there were traditionally many low value projects such as logo or simple website design, Fiverr is clearly seeing that these tasks are increasingly being undertaken in house using AI enabled tools. Consequently, the organization is aiming up the value curve to larger projects which are less impacted by the rise of cheap AI tools such as image generators, agentic website builders and corporate video creation.

The vision is clear for the company. Where friction can appear is when AI takes over in the matching of talent to projects in a manner that may be distinctly different to how it was done in the past. Freelancers may find that, just like when Google changes its search algorithms, their visibility on the platform and job flows, changes which can create a period of dissatisfaction. Any transformation of this magnitude will generate its share of such friction which will have to be navigated.

SAP SE (XETR:SAP)

SAP, the German multinational software company demonstrates that companies of all sizes are re-envisioning their workforces in the AI era resulting in large scale redundancy programs as organizations “reskill” for the future. While a slightly older example (2024-2025), SAP announced 9,000-10,000 layoffs, representing up to 10% of its entire global workforce as part of a strategic shift toward “Business AI.” The company explicitly stated that automation would reduce internal staffing needs, resulting in the elimination of legacy roles, though as in other examples, reduced headcount budgets would be reinvested in talent experienced in AI and machine learning.

SAP is focusing on “agentic governance” and embedding AI across its entire ERP system spanning HR, supply chain and finance. This is in recognition that as clients deploy hundreds of specialized AI agents, the software backend must be re-engineered to manage this digital workforce requiring different skill sets and a new way of engaging with clients during ERP cloud migrations and deployments.

The overarching takeaway from a review of agentic AI programs across the Software and SaaS industry is that not all companies are looking to capture the agentic dividend in the same way. Dictated by the specific business imperatives they find themselves in, some companies are undertaking blunt force resets and rebuilding whole product portfolios and operating plans while others are taking more iterative steps. Some companies, particularly those heavy in lower value roles such as customer support and back and middle office processing are finding net reductions in labor overhead as a result of AI while others are fully reinvesting that budget in more expensive AI trained talent but forecasting a future of reduced headcount growth and more visible operating leverage which can drive margins higher over time. However, supporting the fears evident in the SaaSpocalypse sell offs, it does become clear from these case studies that software vendors exposed to per-seat licensing are under pressure to pivot toward transaction, consumption, or outcome-linked pricing if their own AI enabled products reduce user counts.

Financial Technology / Digital Payments

Block (NYSE: XYZ)

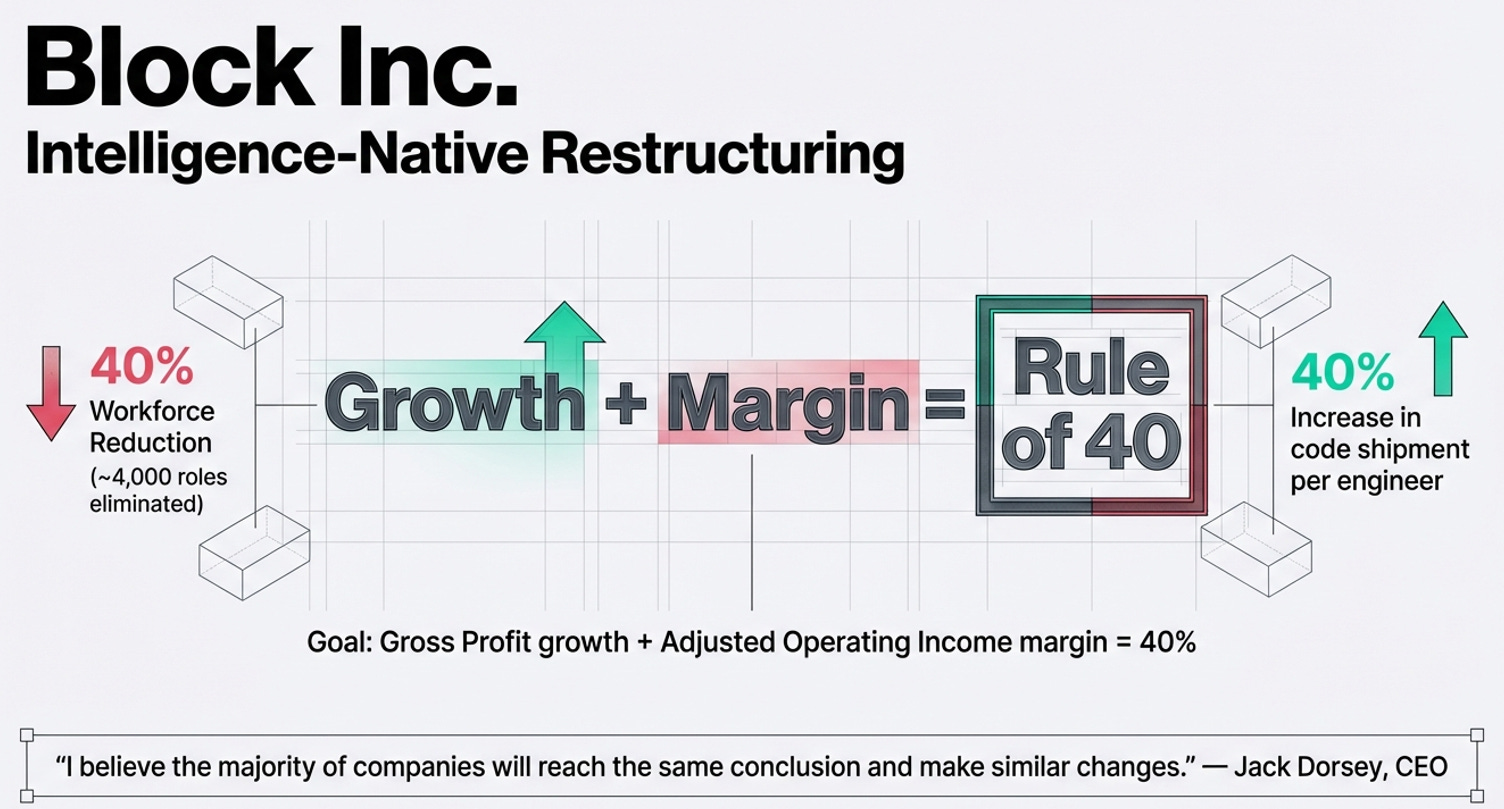

Block is another of the most aggressive agentic AI implementations I can find in my research. The company describes its 2026 restructuring as explicitly AI-led, with more than 4,000 jobs cut, representing about 40% of the workforce. Management has tied the overhaul to an “intelligence-native” operating model in which agentic coding tools, automated financial operations, and daily internal AI usage allow the company to improve their delivery of financial services with a radically smaller workforce.

From an investor perspective, Block is compelling because management have linked the initiative to higher margins and earings. The company’s strategic target is the Rule of 40 by 2026, and the labor savings are guided to drive adjusted operating income margins higher in each quarter of 2026. The company raised its 2026 gross profit target to $12.2 billion, and expanded its share repurchase program generating a 20% spike in the share price on the announcement date. But again, Block is another case of a stock that appears to be forced into extreme action due to underperformance and AI distruption risk. Block’s share price fell 30% over 2025 in the “AI disruption sell-off” and is down over 70% since its 2021 peak. This experience has led the company to consider radical strategies.

This case study also highlights where the largest agentic AI gains are being experienced. Management cited engineering tasks that now take a fraction of the prior time using agentic coding tools, and reported a 40% increase in production code shipped per engineer since September. In a fintech context, where engineering, risk operations, and support are the largest components of operating expenditures and where, absent operating constraints, there is a large addressable market to underpin future revenue growth, achieving higher margins and a more fixed overhead as you grow can become a flywheel. Added profitability can be used for accelerated customer acquisition and new product releases on a faster cadence. This is clearly the vision.

The main risk is once again the integrity of execution. Block’s cuts are so deep that a huge amount of organizational knowledge and experience scars are taken out of the business. The market will be laser focused on any signs that credit processes have been weakened or customer experience has deteriorated as such mistakes can build and potentially force rehiring to duplicate functions that are not operating as expected under new automated processes. Even so, Block appears as one of the fastest and most aggressive “AI-first cost base reset” stories in public markets.

Klarna (NYSE:KLAR)

Klarna offers another example of AI-driven labor decoupling. The company’s internal AI agents are said to perform the equivalent work of 853 full-time staff, up from 700 earlier in 2025, while the actual workforce has nearly halved over three years from 5,527 employees in 2022 to 2,907 in late 2025. Unlike Block’s blunt-force layoffs, Klarna relied heavily on a prolonged hiring freeze and normal attrition.

The results of this AI-led strategy reinforces what Block is trying to achieve. Klarna increased total revenues by 108% over this 3 year period while holding operating costs flat, pushing revenue per employee to roughly $1.1 million. This is a clear example of agentic AI changing aspects of the core unit economics of a business. We can also surmise from the fact that average compensation for remaining staff also rose materially that, like examples before this, Klarna’s workforce is distinctly different now with fewer, more technical and highly paid employees who oversee the agentic systems.

For investors, Klarna paints the best picture of the potential “agentic dividend” that we can expect more and more companies to chase: flat opex and much higher revenue productivity. However, the case also shows an aspect of potential risk. Despite reliance on agentic systems in fraud detection and credit assessment, where the company has stated that credit assessment has been “entirely handed over” to AI systems, Klarna’s provision for credit losess climbed over 100% in the last financial year. It is difficult to separate out in this figure the contribution of three potential factors, the impact of mix shift to longer term loans which require higher provisioning, a slower macroeconomic environment affecting consumers, and the potential of a systems related weakening in approved credit quality. Analysts have questioned whether AI is prioritizing volume over quality within credit assessment processes or missing the impact of a weaker consumer environment. These questions will remain until Klarna can demonstrate a normalization in loss provisions and offer a warning to investors in Block as to what to watch out for.

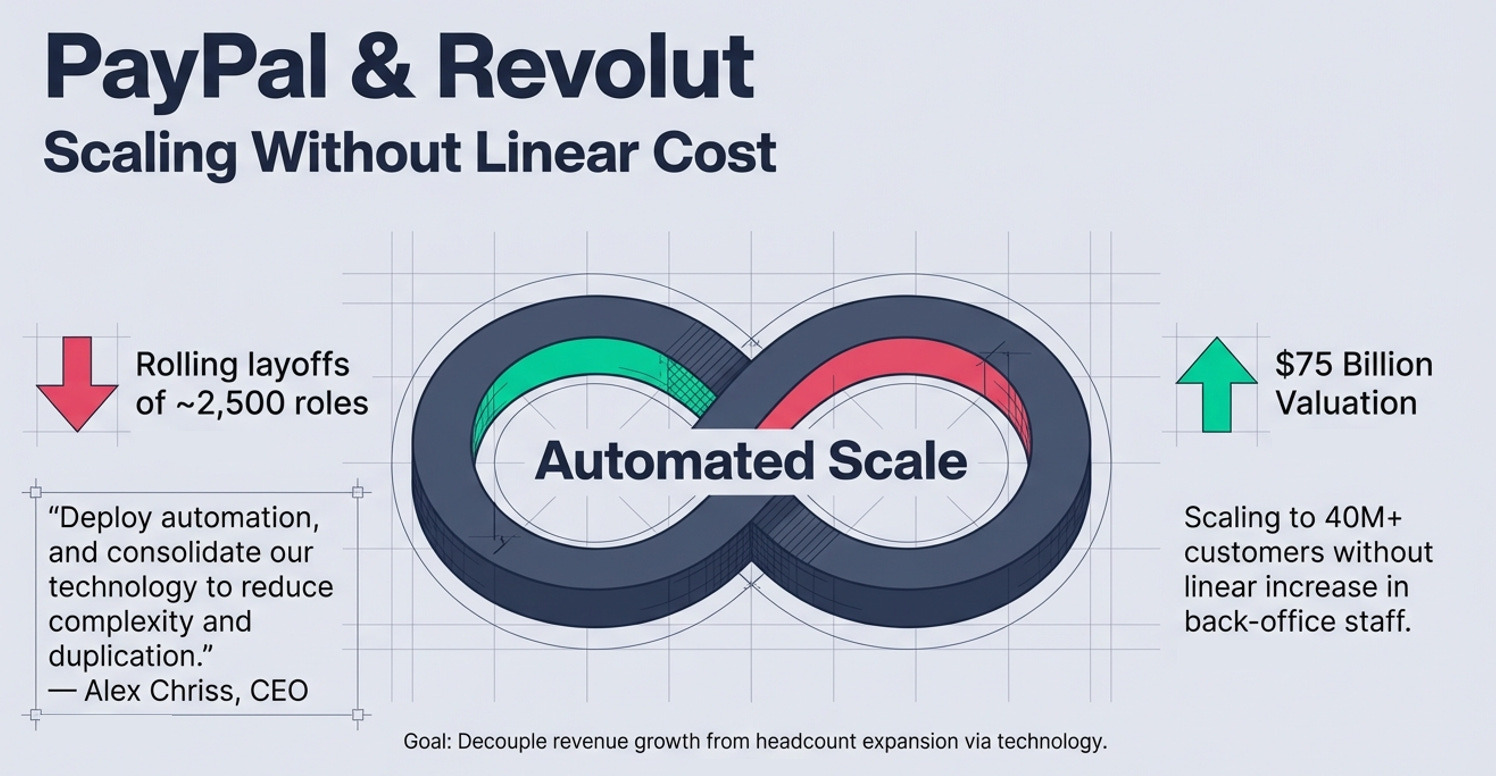

PayPal and Revolut

PayPal and Revolut are more thematic than central to this report, but they reinforce the broader fintech pattern. PayPal, like Klarna, has cut approximately 2,500 roles across 2024 and 2025 while deploying automation in fraud detection, risk management, and customer support. This shows an industry wide move towards agentic back and middle office processes. In Paypal’s case however, they have been unable to translate that efficiency into stronger revenue growth. Revolut on the other hand, while using AI in credit assessment, is more focused on customer facing AI enablement. They provide AI tools to assist users in monitoring spending habits and administrative tasks and enabled the app to provide agentic or conversation payments for ecommerce transactions. This is where users in the future complete transactions conversationally without clicking a “Buy Now” button. In doing so, the company is targeting higher growth in transaction payment volumes as ecommerce trends move to the agentic era.

The implication is that fintech may be the sector where agentic AI translates most directly into margin opportunity because the labor pools are large, and deeply embedded in variable customer servicing, risk detection and credit assessment costs and core systems are (usually) modern, integrated and therefore more readily interacted with by agents. That aligns with the broader observation that software and fintech show the strongest traction in converting AI into immediate bottom-line labor savings.

Banking / Financial Services

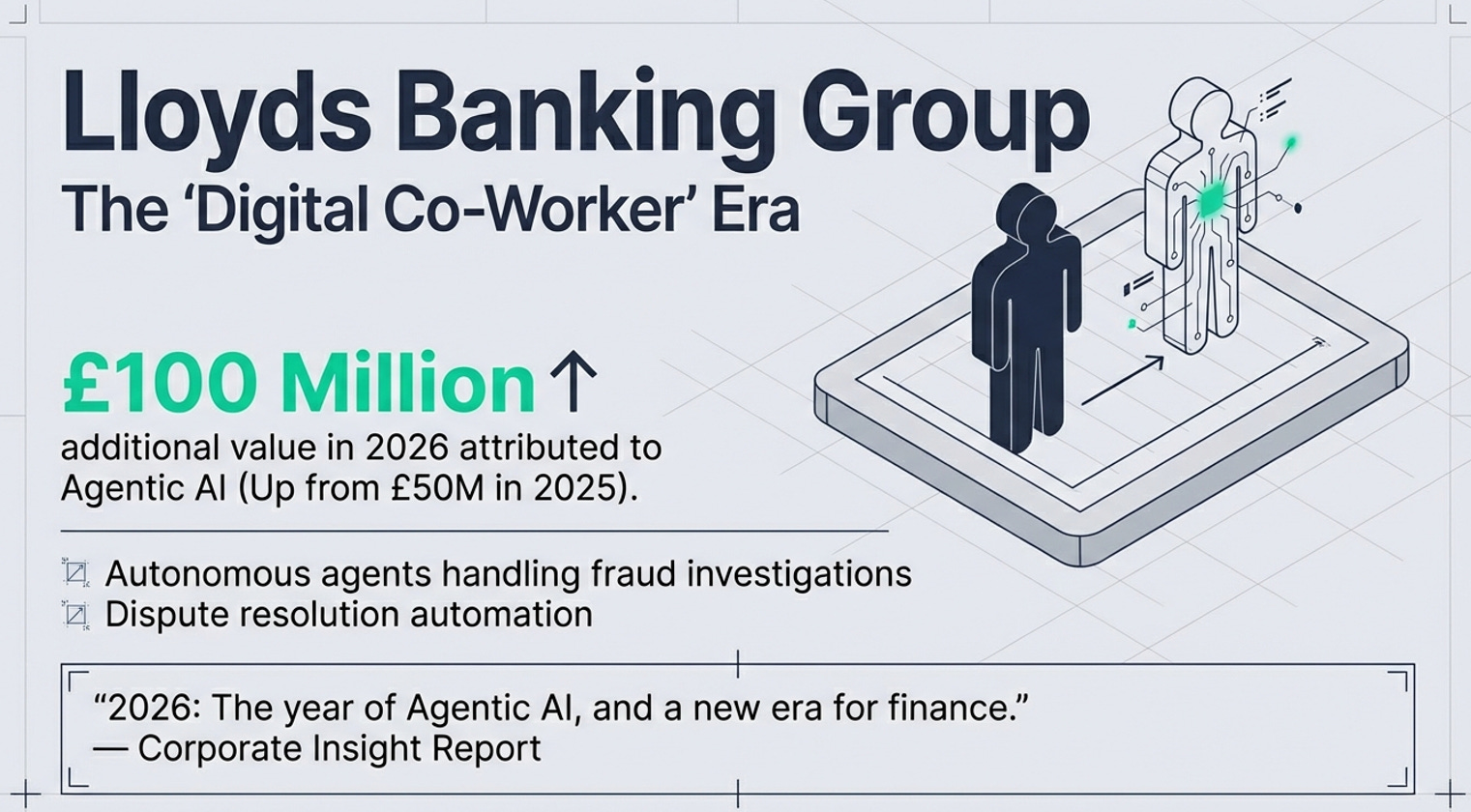

Lloyds Banking Group (LSE: LLOY)

Lloyds is an instructive case within the banking industry because the company has attached explicit value targets to agentic deployment. Management has targeted 2026 as the year of enterprise-wide deployment for agentic AI and expects these systems to generate £100 million of additional value on top of £50 million in 2025. It is, however, clear that within the highly regulated banking industry, companies are having to be more conservative with agentic labor reduction targets and the pace of deployments than in software and fintech sectors. The regulatory, reputational and remediation cost of a botched agentic implementation could be huge. Hence these companies will have to move more methodically over longer timeframes. £100 million is large in magnitude but small in materiality to Lloyd’s bottom line (~1%). The operational disclosures of Lloyds however shows where the agentic focus is within banking involving fraud investigations and complaint resolution at the current time. Agentic AI is a means of increasing throughput in back and middle office functions without scaling headcount, which has direct implications for cost-income ratios. We should expect to see similar programs being outlined across the banking sector with the potential for meaningful cost to income ratio improvements over an extended horizon.

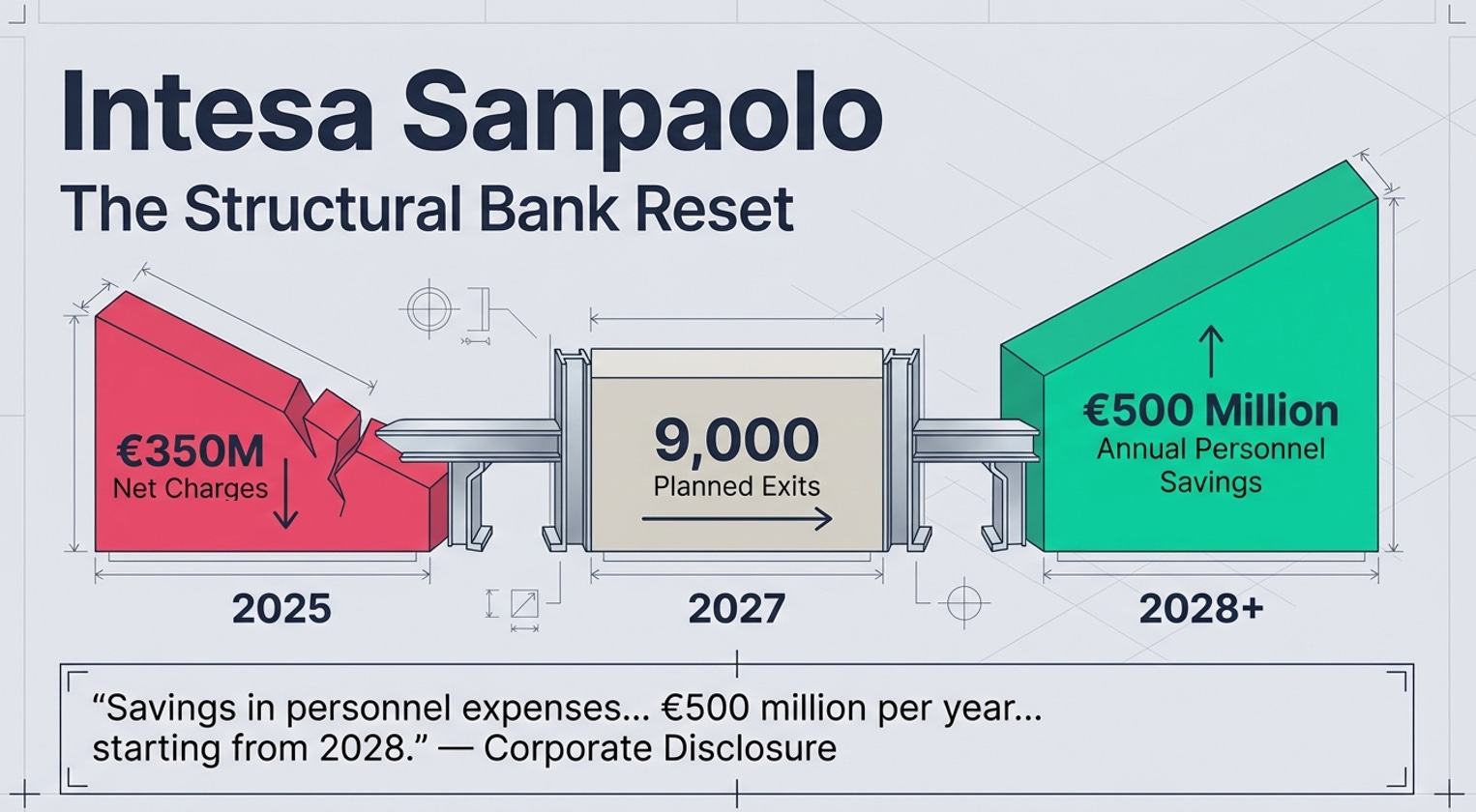

Intesa Sanpaolo (BIT: ISP)

Intesa is a bank restructuring case where explicit targets have been outlined that demonstrate a more bold program than Lloyds. The company disclosed 9,000 headcount cuts by 2027, including 7,000 in Italy and 2,000 internationally, within a digitization and AI strategy. It also disclosed €500 million of annual personnel savings beginning in 2028. The €500 million euro target represents a 2 percentage point improvement in cost to income ratio which is meaningful for the banking industry.

IT Services / Consulting / Engineering

Accenture (NYSE: ACN)

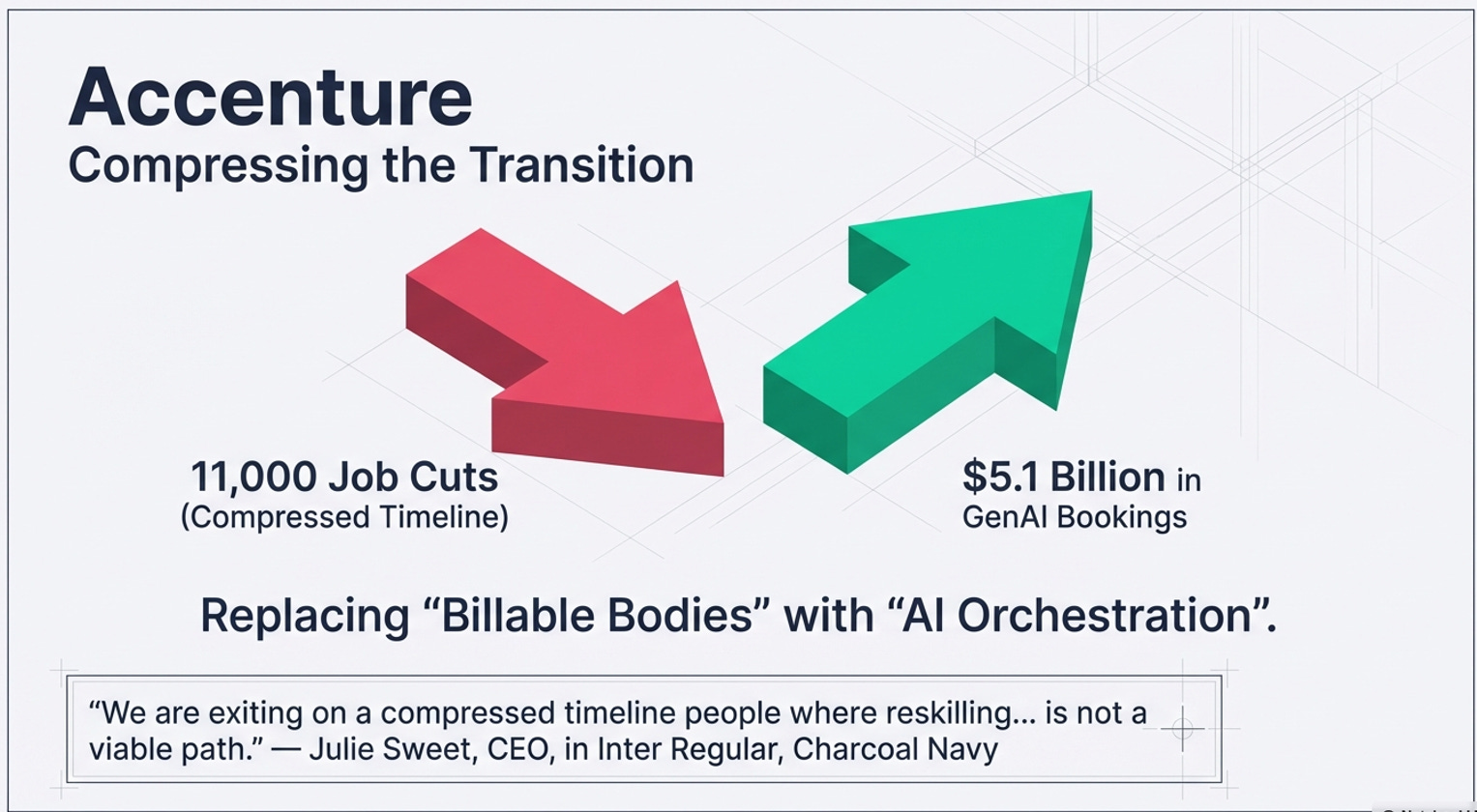

Accenture extends my review of agentic AI programs to the consulting sector and is interesting because it captures all sides of a very complex agentic transition within this industry. IT consultants in particular are facing AI related threats to demand due to agentic coding agents while also navigating internal consulting staff labor reskilling. Accenture has had to rebalance its consulting skills mix by doubling specialized AI and data professionals to 77,000. At the same time, it cut 11,000 jobs in a single quarter and recorded approximately $865 million in restructuring costs.

The strategic logic of this maps what we have seen in the preceding case studies. Legacy skills, particularly in lower value added activities are being reduced while demand is growing for AI related skills. Consulting has historically depended on a labor first model and therefore the skills mix is directly related to revenue earning potential for the business. Accenture is attempting to maintain relevance (and revenue growth) by moving away from manual consulting labor toward higher-margin AI architecture, data engineering, and agent orchestration. Management’s comment that some staff were exited on “a compressed timeline” because reskilling was not possible is informative. This is not a productivity enhancement program, but a change in the underlying skill mix required to generate revenue and stay relevant to clients in the future.

For investors, the question is whether Accenture can sustain bookings growth in the face of broader industry disruption driven by agentic AI. The IT services sector is one of the industries most threatened by this because it undermines geographic labor arbitrage. In that context, Accenture’s restructuring looks more defensive than growth oriented.

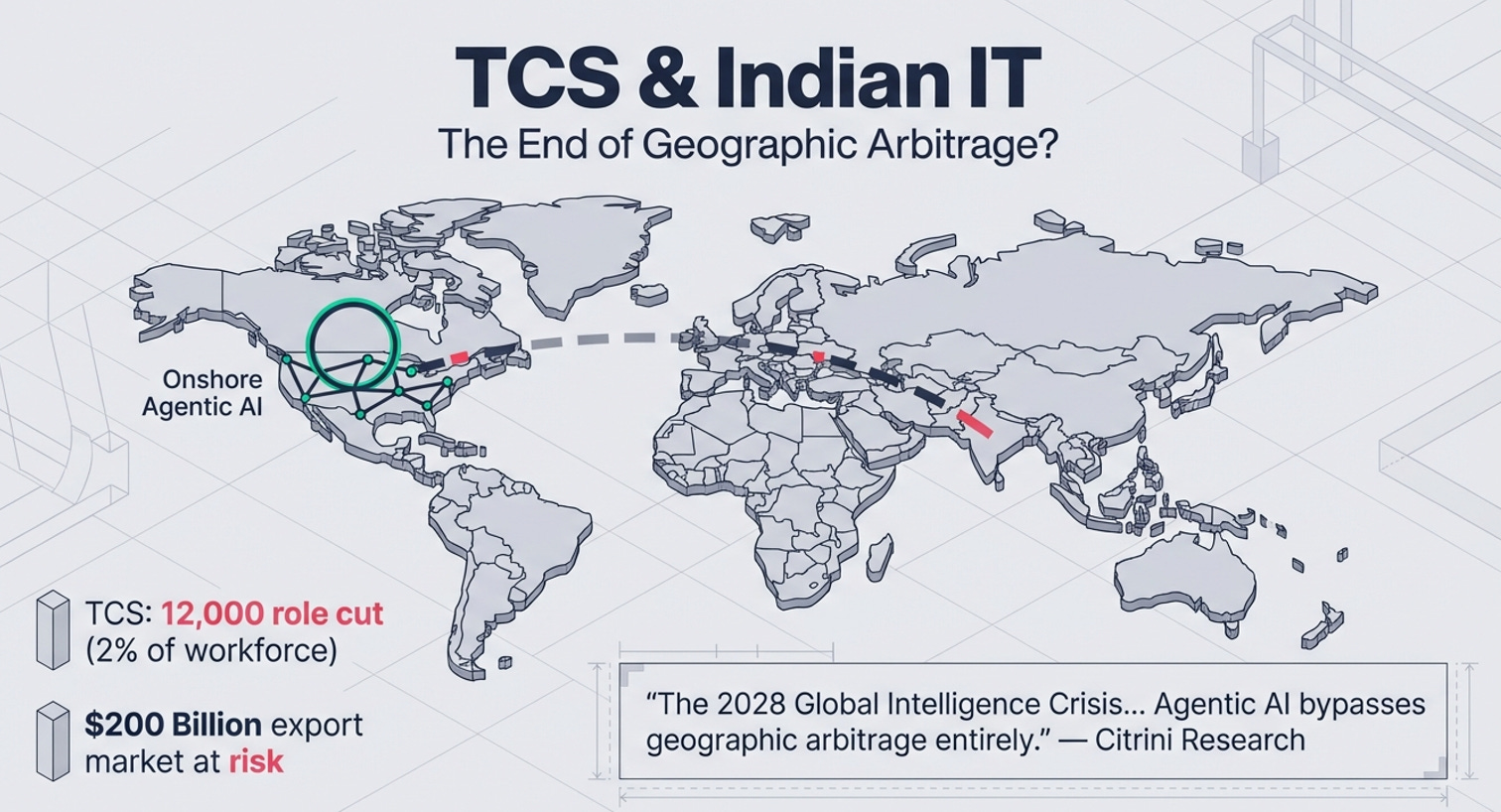

Tata Consultancy Services (NSE: TCS)

TCS, another IT consulting company based in India, also presents less as a winner and more as a company facing structural pressure from agentic AI. TCS cut around 12,000 roles in 2025, roughly 2% of its workforce, citing automation and AI productivity programs. However at the same time, its revenue growth rate collapsed from 17% 3 years ago to 5% in 2025. The entire offshore IT export model is likely vulnerable because agentic AI bypasses geographic labor arbitrage. If enterprise customers can replace outsourced coding and support work with AI agents at the marginal cost of compute, the historic value proposition of offshore billable bodies compresses materially. Effectively agentic coding agents become the lowest cost engineering talent which is a role that India particularly has played for the world for a decade plus.

That does not mean TCS cannot adapt, but it means the “agentic dividend” here may be as much about survival and business-model reinvention as opposed to margin upside. The capabilities of agentic coding agents makes clients once again reconsider the question of outsource or insource. Relative to software and fintech, the consulting/BPO sector appears to face a more urgent version of the labor reset.

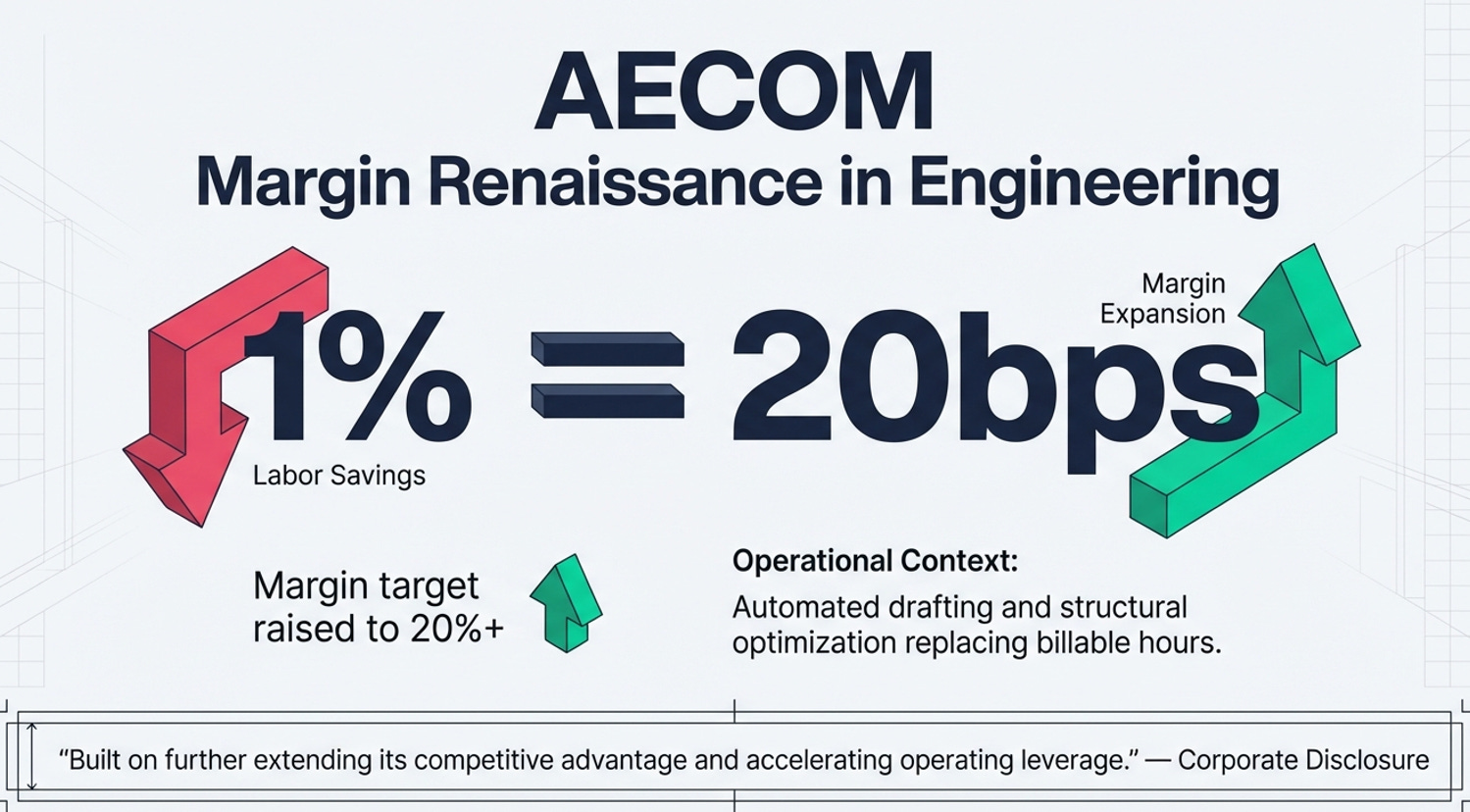

AECOM (NYSE: ACM)

AECOM is another important case because it demonstrates AI adoption within the industrial and engineering sector. The company has also made the economics of AI unusually explicit for investors. Complex engineering tasks such as CAD drafting, tender preparation, predictive maintenance scheduling, and site planning are increasingly handled by autonomous workflows in AECOM. In response, the company raised its long-term margin target to above 20% (from 17%) by fiscal 2028 and lifted its EPS CAGR guidance to above 15% for 2026 to 2029. Unfortunately, this came with a material downgrade to revenue forecasts which saw the stock down 20% back at its November earnings reporting date.

An important detail regarding AECOM is the sensitivity of its earnings to labor costs in such a traditionally labor heavy industry. Analysis suggests that each 1% of labor savings generated by AI adds roughly 20 basis points to AECOM’s operating margin. In an industry where operating margins often run in the 5-8% range (AECOM is at 6-7%), that makes agentic AI a strategic priority for management teams.

Telecom / Hardware / Communications

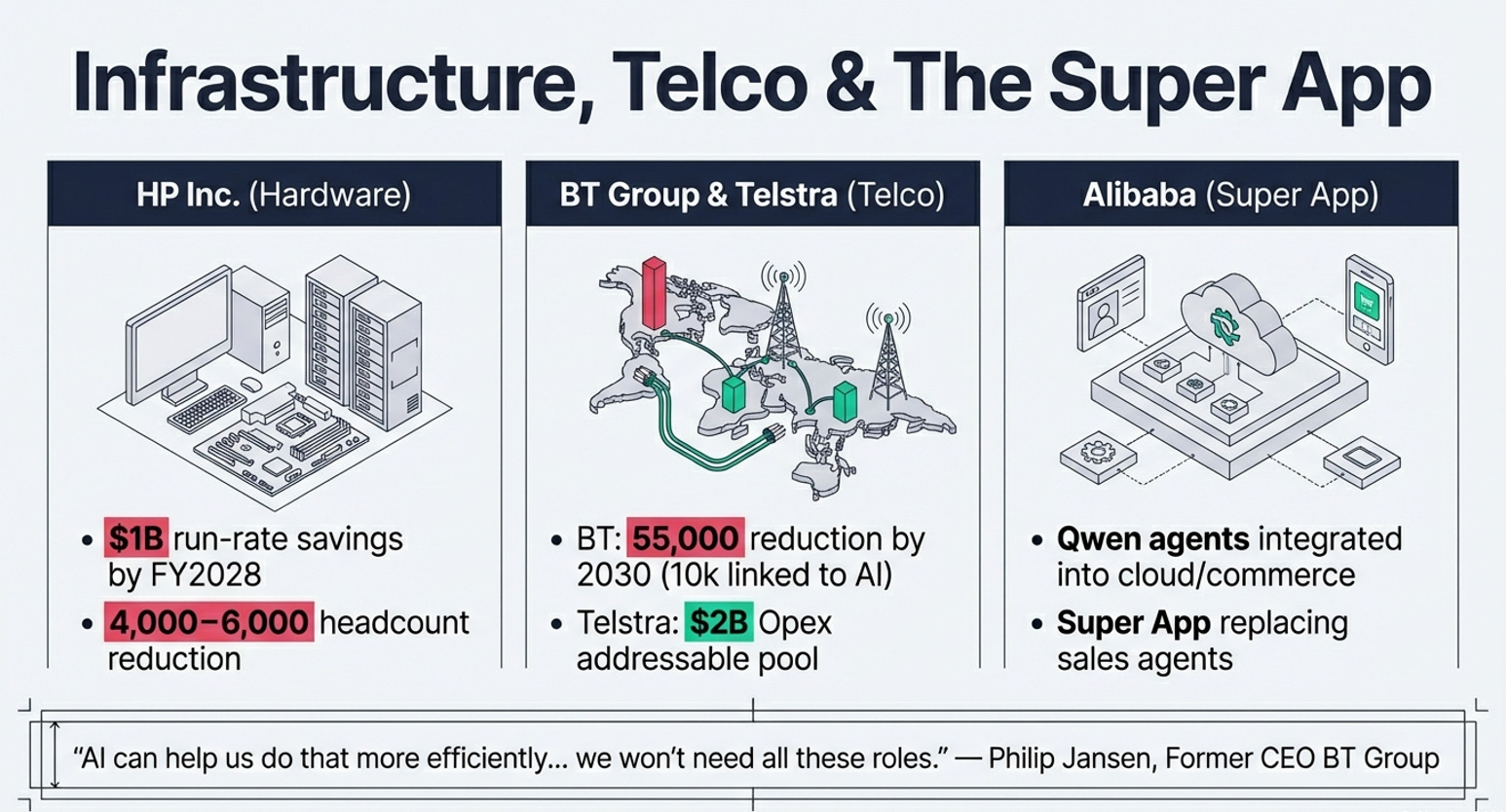

HP Inc. (NYSE: HPQ)

HP is a broad AI enablement case rather than a true agentic example, but the numbers are material enough to warrant attention. The company disclosed a fiscal 2026 plan centered on AI adoption with $1 billion of gross run-rate savings targeted by FY2028. As part of this, a gross global headcount reduction has been indicated of 4,000 to 6,000 staff. This is approximately 8%-11% of its 55,000 strong global workforce. That $1bn savings target also represents 14% of the entire company’s non-manufacturing overhead. In a highly competitive hardware industry where margin expansion is typically difficult, this program represents a step change in costs and efficiency.

BT Group (LSE: BT.A)

BT represents a telecom case study with a headline catching headcount reduction plan. The company disclosed plans to reduce labor resources by up to 35,000 out of ~110,000 employees (or over 30%) by 2030, with around 10,000 roles linked to AI, digitization, and automation. The operational focus of this program includes customer call handling, diagnostics, and network management which are all areas where agentic systems can automate processes readily. BT’s plan encompasses aspects which are not related to agentic automation. For example much of the headcount reduction is related to contractor cuts following completion of 5G and fibre installations. Even so, the company popped up in my research because the absolute scale of targeted labor reduction, even when constrained to the 10,000 roles directly linked to automation initiatives, is among the largest in UK public markets.

KT Corporation (KRX: 030200)

KT’s “AICT” pivot is another example of telecom restructuring under an AI banner. They have announced reassignment of 1,700 employees into subsidiaries and a total headcount reduction of roughly 4,500. The company is attempting to reposition itself as an AI-enabled and IT-driven business rather than a conventional telco, which makes the labor program strategically important even if the margin outcomes are not yet fully outlined yet.

Proximus Group (EBR: PROX)

Proximus pops up in my research as a smaller but still interesting European telecom case study. The company has announced plans to cut 1,200 jobs by 2030 representing 15% of their workforce. This amounts to a reduction of staffing expenses of €25 million by 2028, attributed primarily to AI-driven efficiency gains. This is not among the largest agentic labor displacement cases, but alongside BT Group and KT Corp, it reinforces that telecom is becoming a meaningful vertical for agentic labor substitution.

Cross-Sectional Takeaways

This report is designed to surface details of how widespread agentic AI deployments are becoming and the labor cost (and workforce) impacts they can potentially have across companies. By highlighting 19 short case studies, certain trends and commonalities become clear.

First, it is striking how, in so many of the discussed case studies, the most aggressive agentic AI adopters at this early stage are companies facing significant potential AI disruption and falling share prices. There is a clear observation here that these deployments are actually not coming from a position of strength but that of defence. Time will tell how that strategic catalyst, being different to typical internal R&D led offensive strategies, translates into success or unanticipated operational challenges.

Second, across the researched companies, there are certain industries that appear to have larger opportunities from agentic AI than others. Some companies, mainly within software and fintech spaces, have taken a blunt force, “grab the whole opportunity” approach while others, particularly within more regulated industries like banking and financial services need to move slower and more methodically. Without doubt, the fastest and most aggressive “AI-first cost base reset” stories are currently Block and WiseTech, both because of scale and because management has explicitly tied the labor reset to a redesigned operating model. Both face material opportunities (margins and earnings) and risks (reputation, labor disputes, customer backlash and operational missteps). However, their agentic AI deployments, being market leading, starkly highlight the trend amongst companies that has only just started and is expected to get louder.

A third observation is how agentic AI is reshaping workforces, remuneration structures and unit economics. Klarna’s example adds another facet to our understanding of agentic AI where they have used the technology so far to rebuild a workforce of fewer, more highly paid employees. They have translated higher revenue per employee to a more senior, flatter structure. This same observation appeared in a number of the case studies where legacy skills are being shed and replaced by AI trained personnel. I have university age children and have pointed this out to them to highlight how the next generation needs to be more technically skilled than ours in order to align with labor demand trends.

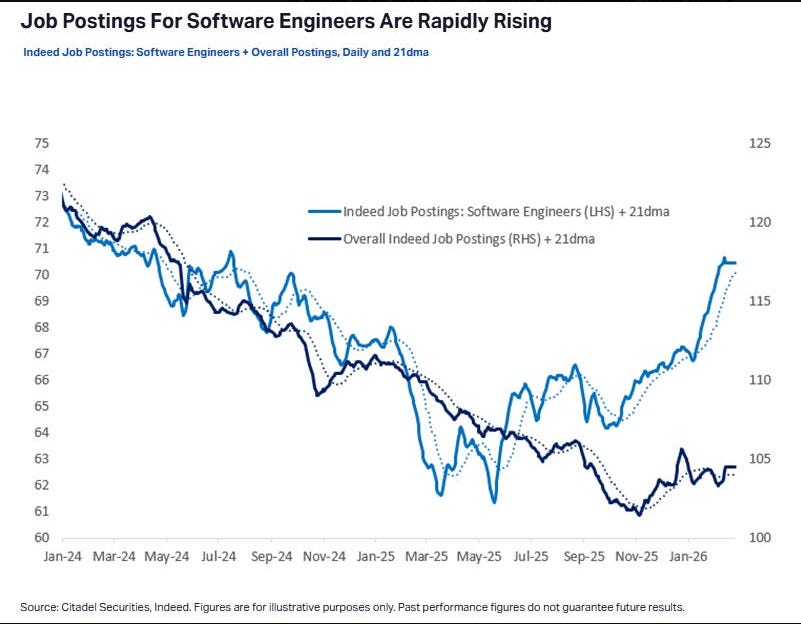

We are seeing this trend now in Indeed job stats. Software engineering job ads are actually surging on the Indeed job platform since November 2025, however the composition of those ads are vastly different than before.

They are concentrated in AI engineering roles to allow companies to push ahead with the agentic deployments. This observation is verified by a 900% surge in Agentic AI related job descriptions on the platform and Gartner and Deloitte research. That job ad trend is perhaps one of the best leading indicators suggesting that more and more announcements like those of Wisetech and Block are forthcoming across industries. Some companies have acted ahead and others are following their progress and learning from what they get right and wrong, but the expertise to deploy mass agents and restructure workforces is being strapped on by companies right now across the globe.

Lastly, agentic AI implementations are leading to equally large opportunities for both small and large businesses. Fiverr, a relatively small business, is cutting 30% of its entire workforce while BT Group, a massive telco is cutting a similar proportion of its headcount out to 2030 albeit a smaller 10% is disclosed as directly related to AI. HP Inc has announced 10% cuts, Block, 40% cuts, Wisetech 30%+ cuts and Klarna reduced its workforce by 50% over 3 years due to automation. At the same time, many of these organizations are also hiring as part of a reskilling phase. The Indeed job stats chart shows this. Overall Indeed job postings have fallen but since late 2025, jobs requiring AI skills have inflected upwards. Many of the case studies reflect this trend. Projections of high global unemployment due to AI are likely far fetched however, the complete picture from this article is a decade of labor reskilling ahead of us.

Andy West

The Inferential Investor