Quantifying Google’s Structural Cost Advantage vs OpenAI in the AI Arms Race

As the market in 2026 focuses on AI unit economics - this is a must read for investors.

By reading this article, readers acknowledge and agree to be bound by the terms of our full legal disclaimer. The information provided herein is for educational and general informational purposes only and does not constitute professional financial or investment advice nor a recommendation to invest or trade in any stock mentioned.

Date: January 25, 2026

We encourage our work to be shared around. If you find this valuable, please share with your contacts to help the Inferential Investor community to keep growing.

By early 2026, the artificial intelligence narrative has shifted once again. The initial phase of the generative AI era was defined by a race for raw capability. This entailed the question of who could build the smartest, most capable model, regardless of cost and OpenAI was winning. Today, as enterprises move from experimentation to large-scale deployment requiring AI companies to massively scale their infrastructure, the defining metric is changing. With questions on cost of operation, sustainability of capex, eventual return on investment and funding the cumulative losses of market leaders, the debate for investors in 2026 is increasingly about unit economics.

It is within this investment context that I undertook to try and quantify any cost advantage Google has developed in AI and understand the implications of this for the future. The information below is truly surprising in magnitude and implications.

In this new phase of industrial AI, a significant, structural divergence has emerged between the two leading players: OpenAI and Google. While OpenAI maintains a formidable reputation for model quality and deep reasoning capabilities, Google has quietly constructed a vertical integration “full stack” advantage that is proving difficult for competitors to replicate. By decoupling its destiny from third-party hardware providers like NVIDIA, Google has achieved a structural cost leadership position that is beginning to reshape market share and business models across the sector.

This analysis examines the mechanics of Google’s cost advantage, quantifying the differences in hardware infrastructure, training expenses, and operational costs, and explores the long-term implications for investors.

1. Two Architectures: OpenAI vs Google

To understand the economic divergence, one must look at the physical infrastructure powering these AI giants.

OpenAI: Premium Hardware, Premium Pricing

OpenAI’s infrastructure, predominantly housed within Microsoft Azure’s data centers, relies on a “best-of-breed” approach. They utilize the most powerful general-purpose graphical processing units (GPUs) available, primarily supplied by NVIDIA. In 2026, this means the NVIDIA Blackwell and upcoming Vera Rubin platforms, which offer immense computational speed and networking capability.

However, this performance comes with a significant “margin stacking” problem. NVIDIA commands gross margins exceeding 70% on its hardware. Microsoft Azure then adds its own margins for hosting, power, cooling, and networking services. By the time a FLOP (floating-point operation) is executed for OpenAI, it carries a substantial cumulative markup. While this architecture is incredibly potent and flexible, it is fundamentally expensive. This gets reflected in OpenAI API pricing for enterprise customers and operating losses within the consumer segment where free and low cost subscription tiers fail to recoup the cost of token generation.

Google: Vertically Integrated, Cost Leadership

Google has taken a radically different path, pursuing total vertical integration for over a decade. They do not rely primarily on NVIDIA GPUs for their core AI workloads. Instead, they design their own specialized chips, known as Tensor Processing Units (TPUs).

The current generation, TPU v6 (Trillium) and v7 (Ironwood), are not general-purpose processors. They are application-specific integrated circuits (ASICs) designed from the ground up for one task: running the specific mathematical operations required by modern neural networks, such as Google’s Gemini models.

By designing the chip, the server rack, the data center cooling systems, and the compiler software (XLA) simultaneously, Google eliminates vendor markups and achieves efficiencies impossible in a mixed-vendor environment. They are not paying the “NVIDIA tax.”

2. Model Training Cost Comparison

The first area where this architectural difference manifests is in the massive capital expenditure required to train “frontier models”. This is the initial, months-long process of teaching an AI model using vast datasets.

Training a frontier model in 2025, such as OpenAI’s GPT-5 series or Google’s Gemini 3, requires tens of thousands of chips running synchronously for months, consuming gigawatts of energy.

Industry estimates suggest that the cost to train GPT-5.2 on NVIDIA infrastructure ran into the high hundreds of millions, potentially exceeding $1 billion when factoring in the associated Azure infrastructure costs.

Conversely, internal data and architectural analysis has been reported to suggest that Google DeepMind is able to train equivalent-scale Gemini models for approximately 20% to 30% of that cost. This is because their hardware co-design avoids the “NVIDIA tax” and allows for architectures like “Sparse Mixture-of-Experts” (MoE) to run far more efficiently. MoE activates only a small fraction of the model’s network for any given task, saving immense amounts of energy. While NVIDIA hardware can run MoE models, Google’s TPUs are purpose-built to optimize the specific communication patterns these models require.

3. Data Center Infrastructure Cost Comparison

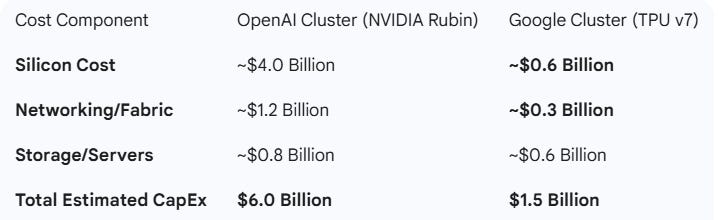

The following analysis quantifies the staggering hardware cost differences between OpenAI (leveraging Microsoft’s NVIDIA-centric data centers) and Google (using its internally designed TPU ecosystem). To understand the cost gap, one must first look at the design philosophy of the chips themselves.

NVIDIA Rubin (OpenAI’s Backbone)

NVIDIA’s 2026 flagship, the Vera Rubin (R100), is a general-purpose AI powerhouse. It is designed to be the best at everything including training, inference, and complex reasoning.

The “Margin Stack”: Because NVIDIA is a merchant silicon provider, they command gross margins of 75%. OpenAI, renting these through Azure, pays for NVIDIA’s profits plus Microsoft’s operational overhead (particularly since OpenAI’s reorganization to a for profit entity).

Complex Interconnects: To make 100,000 Rubin GPUs act as one, OpenAI relies on NVLink 6 and InfiniBand. These networking components alone can account for 20% of the total cluster cost.

Google TPU v6/v7 (Google’s In-House Engine)

Google’s Trillium (v6) and Ironwood (v7) are ASICs (Application-Specific Integrated Circuits). They are stripped of everything not related to matrix multiplication (the math of AI).

The Vertical Advantage: Google pays the marginal cost of production, estimated at less than $3,000 per chip, whereas an equivalent NVIDIA Rubin module can cost $35,000 to $50,000 on the open market.

Optical Interconnects: Google uses proprietary Optical Circuit Switching (OCS) to connect its TPUs. This is significantly cheaper to scale than the copper-and-switch-heavy InfiniBand networks OpenAI requires.

For a standardized cluster of 100,000 chips (the size required for a frontier model like Gemini 3 or GPT-5.2), the capital expenditure (CapEx) divergence is immense.

Google can build four equivalent-scale data centers for the price OpenAI pays for one. This is the "Silicon Moat".

4. Operating Costs: Inference Costs Per Token

While training is a massive one-time cost, the ongoing operational expense of “inference” is where business model sustainability is measured and return on investment lies. Every time a user asks ChatGPT or Gemini a question, the model must “infer” the answer, costing compute cycles and electricity. In the industry, this is measured in “cost per million tokens”. A large part of this cost is renting the hardware used to run the model and as discussed above, Google holds a significant cost advantage there.

Google reportedly also holds a significant advantage in operating costs for AI token generation that extends past the defrayed costs of AI hardware to power consumption.

Power Consumption: An NVIDIA Rubin rack (NVL72) can pull over 120kW. At 2026 electricity rates, running OpenAI’s clusters costs hundreds of millions per month.

TPU Efficiency: Google’s TPUs are reported to be 3x–5x more energy-efficient per TFLOPS than general-purpose GPUs. Because Google designs its own power delivery and liquid cooling systems, their “Power Usage Effectiveness” (PUE) is among the lowest in the industry.

In 2026, the market for AI APIs has become hyper-competitive. On the surface, pricing between Google and OpenAI seems comparable. For example, a standard input token might cost ~$2.00 per million across both platforms for the latest models. However, the underlying economics of output tell a different story.

A critical differentiator is the cost of output tokens including “reasoning” or “thinking” tokens. Modern models often generate thousands of internal, invisible tokens to “think through” a complex problem before presenting a final answer. Output tokens (including thinking tokens) for the latest models cost $12-$14 / 1M, up to 7x the cost of input tokens. This is because because while inputs are processed by transformer models all at once (in parallel), output tokens are produced by an autoregressive process. This means that the model predicts one token, then uses that token (and those preceding), to predict the next and so on. This decode phase effectively needs to run the entire neural network for each token produced - 1000 tokens = 1,000 times. Secondly, to avoid recalculating the entire conversation with each new token, the models use a Key-Value Cache which requires expensive High Bandwidth Memory (HBM). As the output grows, the KV Cache or memory usage grows which has a cost.

OpenAI’s Margin Pressure: Because OpenAI pays a premium for every compute cycle on NVIDIA hardware, they must pass these costs to the consumer/enterprise to generate a margin. For highly complex tasks requiring deep reasoning (like their ‘o1’ class models), pricing can surge to over $60 per million output tokens.

Google’s Margin Cushion: Google charges for thinking tokens as well, currently around $12 per million for Gemini 3 Pro. However, due to TPU efficiency, their internal cost to generate those tokens is significantly lower than OpenAI’s. This gives Google a massive “margin cushion.” They can price their premium reasoning capabilities aggressively while still maintaining profitability, whereas competitors using third-party hardware would be operating near a loss to match those prices.

Furthermore, for tasks requiring enormous context windows, such as analyzing entire books or years of financial data in one prompt, the massive memory bandwidth integrated into Google’s TPU v7 pods allows them to serve these requests with less hardware overhead than equivalent NVIDIA setups, further reducing their internal costs.

5. Where Google’s Cost Advantage Shows Up: Token Subsidies and Market Share Shift

Google is not merely pocketing this margin difference. Instead, they are weaponizing it through what can be termed “token subsidies.”

Leveraging their lower cost basis, Google Cloud is aggressively underwriting the cost of AI adoption for enterprises. In 2026, we are seeing massive credit programs entailing upwards of hundreds of thousands of dollars for startups and significant discounts for large enterprise commitments that effectively make the AI compute component nearly free for the first year of adoption. Google is taking the long term view, seeing AI compute as a commodity but Google Cloud as their real return engine.

For a CTO at a Fortune 500 company deciding where to build their generative AI infrastructure, the math becomes unavoidable. Even if they prefer OpenAI’s model nuances slightly, a 40% to 60% reduction in total cost of ownership (TCO) offered by Google Cloud, driven by TPU efficiencies and aggressive subsidies is too significant to ignore for high-volume utility workloads. Given capex and operating cost advantages, this is still profitable for Google.

An example, as best we can produce:

Let’s look at a hypothetical enterprise application processing 10 billion tokens per month (e.g., a massive customer service fleet).

The OpenAI (GPT-5.2) Bill

Estimated Cost: ~$120,000 / month.

The Reasoning Penalty: If the application requires “Thinking Tokens” for complex issues, the bill can jump to $500,000+ because OpenAI must recover the high cost of running sequential inference passes on expensive NVIDIA hardware.

The Google (Gemini 3) Bill

Estimated Cost: ~$70,000 / month.

The Subsidy Advantage: Google often waives the cost of the first 500 million tokens for enterprise cloud customers. Furthermore, their TPU-native MoE (Mixture of Experts) architecture only activates 10% of the hardware for most queries, keeping their internal cost so low that they can offer up to 50% lower prices than OpenAI while maintaining higher net margins.

This is leading to a noticeable market share shift in 2026, particularly in high-volume sectors like automated customer service, data analysis, and real-time translation, where cost-efficiency trumps marginal gains in reasoning capability. It will be interesting to try and isolate the first tangible proof of this in Google/Alphabet’s next earnings report.

6. Implications for Business Models and Investors

The structural cost advantage enjoyed by Google has profound implications for the future strategies of these competing firms.

The Divergence of Business Models

The pressure of high hardware costs is forcing OpenAI to seek immediate, high-margin revenue streams. This explains reports in late 2025 and 2026 of OpenAI exploring advertising models within its products. To justify its valuation and cover its massive compute bills, OpenAI needs revenue density that subscription models alone may not provide. They also need to focus on high-margin segments that require premium reasoning (doctors, lawyers, coders) as they cannot compete with Google in the “Low Margin Utility” segment such as basic chat, search and categorization. This suggests continued market share movement towards Gemini. OpenAI’s chase for the largest consumer user base is in this respect curious. This can only be monetized via advertising and agentic e-commerce but also shouldn’t require the premium hardware OpenAI has traditionally relied on. This last point suggests continued diversification of chip procurement away from NVIDIA towards cheaper AMD alternatives as we started to read about at the end of 2025.

Conversely, Google is under less immediate pressure to monetize the AI models themselves directly. They can afford to treat Gemini as a low-margin utility to protect their formidable search advertising business and lock customers into the broader Google Cloud ecosystem (storage, databases, analytics), where margins remain high.

The Development of a Long-Term Moat for Google

For investors, the key takeaway is that while software leads can be tenuous, hardware supply chain advantages are more durable. OpenAI broke Google’s software moat with great product velocity (ChatGPT in 2023). Google is now countering with a silicon moat that took fifteen years and billions of dollars to build and that as described above, offers an enormous and ongoing cost advantage. While Michael Burry highlights the question mark over Return on Investment for AI companies, this analysis suggests that question mark is far less relevant to Google/Alphabet.

In a world where AI becomes a commodity utility, the provider with the lowest cost of production, enabled by custom silicon, holds the ultimate strategic advantage.

As always,

Inference never stops. Neither should you.

Andy West

The Inferential Investor.

Disclosure: The author holds a long position in Alphabet.