Inferent Market Signals - 6th July 2026.

What are the market internals telling us about trends and risk appetite?

Weekly Market Signals Summary

6th July 2026

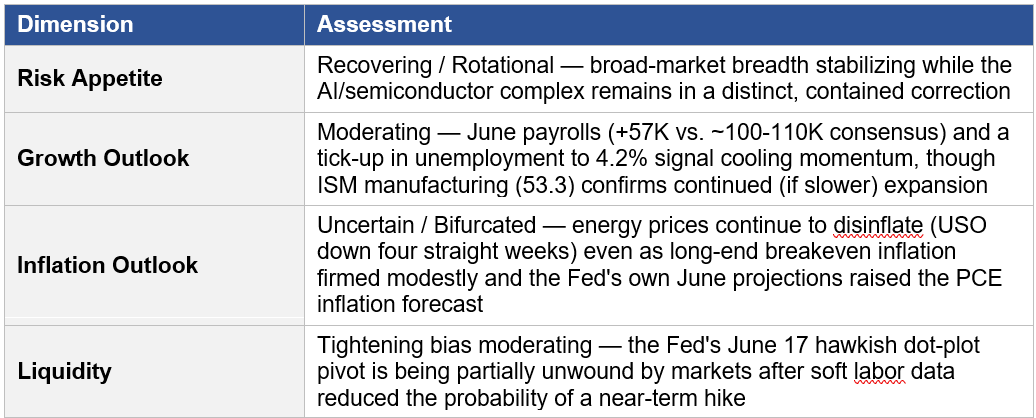

• Regime: markets settling from the acute, breadth-narrowing AI/semiconductor sell-off of the prior two weeks toward a recovering, rotational index tape — the broad market (SPY +2.17%, RSP +2.21%) rallied back essentially in line while the AI/semi complex (SMH -3.15%, IXN -1.17%) remained in its own distinct correction for a third consecutive week. The market is searching for new champions.

• VIX collapsed -14.12% to 15.81, fully reversing the prior week’s fear spike (+9.71% to 18.41) — volatility markets are pricing a contained, idiosyncratic AI correction rather than a systemic risk-off event. This is a positive signal for diversified ETFs / indices and cyclicals.

• The defining macro data point was the June nonfarm payrolls report (released July 2, ahead of the July 3 holiday close): +57,000 vs. ~100-110K consensus, unemployment ticking up to 4.2%. Short-dated Treasuries and hike-probability pricing reacted immediately; the long end, however, sold off (TLT -2.09%), producing a bear-steepening pattern that argues against a simple “soft data = dovish Fed” read. Jobs data can be highly volatile so one data print does not change the picture. The long end is pricing higher term premiums under a Warsh Fed given removal of the chair’s “dot” and shift away from forward guidance. This is keeping pressure on long duration equities.

• TIP outperformed TLT by roughly 87bps (TIP -1.22% vs. TLT -2.09%), consistent with long-end breakeven inflation firming modestly even as growth data softened — a cross-current that sits awkwardly with a pure disinflation narrative.

• Financials were the standout sector (XLF +3.86%, IAT +0.61%), likely reflecting positioning ahead of Q2 bank earnings (JPMorgan, Citigroup, Wells Fargo, Goldman Sachs, Morgan Stanley all reporting July 14-15). Healthcare (IHF +3.43%) extended a third straight constructive week.

• Factor leadership flipped: growth (VUG +3.33%) and quality (QUAL +2.25%) outperformed, while momentum (MTUM -2.82%) and value (VLUE -3.54%) both lagged — a cross-current rather than a clean single-factor rotation, likely reflecting mean-reversion after two extended factor trends.

• Breadth premium (RSP over SPY) narrowed to roughly +4bps from the prior week’s record +256bps — the market is normalizing toward more typical breadth dynamics rather than continuing to extend the narrow-vs-broad divergence.

• Small caps lagged the broad market (IWM -0.74% vs. SPY +2.17%), a reminder that “broadening” this week was concentrated in large- and mid-cap names (financials, healthcare) rather than extending to small caps.

• Gold and gold miners both bounced (GLD +1.22%, GDXJ +2.64%) after three consecutive weekly declines, with miners outperforming on the recovery — consistent with a softer USD and operational leverage working in both directions. Worth watching for further signs of a trough.

• Oil extended its decline for a fourth straight week (USO -1.39%, -8.17% the week prior) as the tentative US-Iran Hormuz framework (signed June 17, reinforced by a US Navy-backed widened shipping route announced June 27) continued to erode the geopolitical risk premium, even though Iran briefly re-closed the strait on June 20 amid Israel-Lebanon tensions.

• Primary economic distance analog: Q3 2024 AI Momentum Pause / Valuation Reset — a contained, multi-week correction in high-multiple AI/semiconductor names against a resilient broader market, awaiting a demand-validation catalyst (NVDA’s August 26 earnings remain the key gate).

• Primary equity implication: the setup may be consistent with continued index-level resilience but further rotation toward financials, healthcare, quality and low-volatility exposures, while the AI/semiconductor complex could remain range-bound-to-soft until a validating catalyst. With a bear steepening curve, index-level upside may be likely to be more measured and rotational than V-shaped.

• Key alternative scenario: if the June labor market softness marks the start of a broader growth deceleration (rather than an AI-specific valuation reset), weakness could broaden beyond semiconductors into cyclicals generally, pulling yields lower across the curve and favoring defensives more broadly rather than the current healthcare-specific pattern.

• The 4 Dimension Risk Regime and News and Event Evolution discussion follows.

Let me introduce you to Inferent Analyst - a cutting edge AI investment research platform being developed by investors - for investors. Inferent Analyst is designed to be every investor’s autonomous equity research assistant. No more pages and pages of raw numbers without context like traditional data terminals. Inferent Analyst actually interprets and analyzes the data automatically, as events unfold, presenting you with the insights you need to discover ideas and make better investment decisions. Pre-register today as subscriber seats will be limited on launch.

4-Dimension Risk Regime Determination

News and Event Evolution

Emergent / Intensified Themes (Most Recent Week)

• June nonfarm payrolls printed +57,000 versus roughly 100-110K consensus (released July 2), with unemployment ticking up to 4.2%. Average hourly earnings rose 0.3% MoM / 3.5% YoY, in line with expectations — a soft headline without an accompanying wage-inflation surprise.

• Short-end Treasury yields fell sharply on the payrolls miss (2-year yield down to roughly 4.13-4.14%) as traders pared expectations for a Fed rate hike as early as September, partially unwinding the hawkish repricing that followed the June 17 FOMC dot-plot shift.

• The long end diverged from the short end: TLT fell -2.09% over the week even as front-end yields eased, a bear-steepening pattern that argues supply/term-premium dynamics (or the Fed’s own elevated PCE forecast) may be exerting more influence on the long end than the softer jobs print.

• ISM Manufacturing PMI registered 53.3 in June, down 0.7 points from May but still signaling expansion for a 20th consecutive month — a moderating-but-not-contracting growth signal.

• Financials (XLF +3.86%) and healthcare (IHF +3.43%) emerged as the clearest sector beneficiaries, with financials plausibly building into next week’s bank earnings kickoff.

• VIX fully reverted (-14.12% to 15.81), and the RSP-over-SPY breadth premium collapsed from a record +256bps two weeks ago to essentially flat (+4bps) — both consistent with a market normalizing rather than continuing to extend either the fear spike or the narrow-vs-broad divergence.

Constant Themes (Both Weeks)

• AI/semiconductor valuation scrutiny: Nvidia, AMD, Broadcom, Micron, Intel, Applied Materials, Lam Research and KLA all traded under pressure as investors reassessed whether AI infrastructure spending remains a durable growth driver or has become a valuation risk.

• US-Iran Strait of Hormuz de-escalation, still incomplete: the 60-day ceasefire framework (signed June 17) continues to be tested — Iran briefly re-closed the strait on June 20 citing Israeli strikes in Lebanon, before a US Navy-backed widened shipping route near Oman was announced June 27.

• Fed policy uncertainty under new Chair Kevin Warsh, whose June 17 press conference reinforced a hawkish, inflation-focused stance even as the committee held rates at 3.50-3.75% for a fourth consecutive meeting.

• Approaching Q2 earnings season, with major banks (JPMorgan, Citigroup, Wells Fargo, Goldman Sachs, Morgan Stanley) scheduled to report July 14-15 — viewed as the most consequential reporting cycle of the year for testing current valuation assumptions.

Fading Themes (Most Recent Week)

• The acute AI/semiconductor panic that followed the OpenAI IPO-delay report (June 25-26) eased somewhat — SMH’s weekly decline moderated to -3.15% from -7.31% the prior week, though the complex remains in a clear multi-week correction rather than a resolved one.

• The extreme defensive-rotation and small-cap-led breadth expansion of the prior week (IWM +1.45%, IHF +6.31%, XLU +3.24%) partially faded: small caps underperformed this week (IWM -0.74%) and utilities gave back gains (XLU -0.93%), even as healthcare’s strength persisted.

• The dollar-strength narrative tied to the hawkish June FOMC softened modestly (UUP -0.46% via proxy) as rate-hike odds were pared back following the weak jobs data.

Important Disclaimer: This analysis is subject to The Inferential Investor’s Disclaimer. It is for informational and educational purposes only and does not constitute investment advice, a recommendation to buy or sell any security, an offer or solicitation, or a guarantee of future performance. The information is derived from sources believed to be reliable but no representation or warranty is made as to its accuracy or completeness. Scenario descriptions are not forecasts but explorations of the implications of a set of described conditions and are subject to risk and uncertainty. Past performance is not indicative of future results. Readers should consult their own advisers before making any investment decision. AI can make mistakes.

Andy West

The Inferential Investor