Inferent Market Signals - 15th June 2026.

What are the market internals telling us about risk appetite?

Weekly Market Risk Regime Summary

15th June 2026

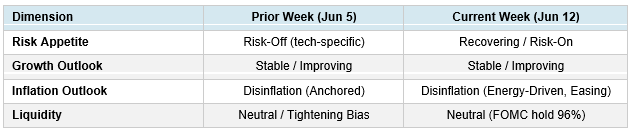

• Regime characterization — current week (Jun 12): Recovering / Risk-On (Transitioning). After the prior week’s tech-specific risk-off episode (Broadcom guidance miss, hot NFP), a broad-based V-shaped recovery emerged across nearly all asset classes, underpinned by two converging catalysts: Iran-US ceasefire deal progress and SpaceX’s record IPO debut.

• Geopolitical pivot: US and Iran negotiators reached a tentative framework (June 12) to extend the ceasefire 60 days, de-mine the Strait of Hormuz, and commence nuclear talks. President Trump cancelled planned strikes Friday, driving a sharp rally into the weekend. This framework — if signed — would remove the near-term Hormuz closure tail risk.

• Oil retreated sharply: USO -5.70% for the week (on top of +3.04% prior week during escalation), bringing USO -2.83% over two weeks from May 29. The geopolitical oil risk premium that built during the Israeli airstrikes (June 8) and Iranian retaliation is now partially priced out.

• Small-cap leadership (IWM +4.02% vs SPY +0.57%) and equal-weight premium (RSP +1.84% vs SPY +0.57%, a +127bps spread) confirm the broadest market participation in several weeks. This is a structurally constructive signal, reversing the concentrated large-cap leadership of recent weeks.

• Semiconductors rebounded sharply: SMH +8.83% — the largest single-week gain in recent data. SpaceX’s $2.1T debut on Nasdaq (SPCX +19.34%), combined with hyperscaler capex commitments of $750B for 2026, helped offset the Broadcom guidance overhang from the prior week.

• May CPI (released June 10): Headline +4.17% YoY, Core +2.9% YoY. Energy-driven. Markets interpreted the print as potentially transitory given oil’s subsequent retreat, with Treasury yields “largely flat after the CPI release” (Morningstar). TLT +0.85% alongside equities = bonds and stocks rallying together = genuine disinflation signal.

• VIX compressed -17.80% (21.51 → 17.68). Every 2026 VIX spike has reverted within 1-2 weeks. Pattern consistency reinforces the interpretation that corrections are episodic within a structural bull regime.

• Gold continued its two-week decline: GLD -2.44% this week (-7.32% cumulative over two weeks from May 29). Macro tail-risk hedges unwinding alongside Iran deal progress. Gold miners (GDXJ) bounced +3.66% from extremely oversold levels but remain -12.59% over two weeks, confirming real yields stay elevated.

• FOMC June 16-17 (this week): 96% probability of no change (Fed Funds 3.50-3.75%). Risk of a language shift toward a tightening bias in the statement, given May CPI headline at 4.17% and core PCE estimates at 2.6%.

• Inflation vs growth synthesis: The energy-inflation impulse is showing signs of unwinding as Iran de-escalation proceeds. Core PCE at 2.6% YoY and core CPI at 2.9% YoY remain above the 2% target but are not accelerating. The twin signal of TLT > TIP for two consecutive weeks confirms breakeven inflation is falling — a disinflation signal that would be consistent with equity multiple expansion.

• Primary economic distance analog: Q1-Q2 1991 Gulf War Resolution — ceasefire removing oil premium, broad equity rally with small caps leading. Currently in the early re-rating phase. From the equivalent phase (late January 1991), the S&P 500 advanced approximately 18% over 6 months, with cyclicals and small caps leading.

• Primary equity implication: Constructive near-term under the primary scenario. A re-test of ATH could be consistent with continued Iran deal execution, FOMC hold, and VIX remaining below 20.

• Key alternative scenario: Capital supply overhang materialises — SpaceX’s $75B debut was only the first wave of an estimated $285B AI mega-IPO pipeline. OpenAI (~$70B, September) and Anthropic (~$60B, Q4) create further institutional liquidation of existing AI/tech holdings to fund allocations. This, combined with a FOMC tightening bias shift, could cap AI/tech performance. An unexpected sharp tightening bias shift by the Fed could resume the de-rating witnessed last week.

4-Dimension Regime Determination

Let me introduce you to Inferent Analyst. This is a new and unique AI investment research analyst platform being developed right now. Inferent Analyst is designed to be your agentic equity research assistant. No more pages and pages of raw numbers without context like traditional data terminals. Inferent Analyst actually interprets and analyzes the data automatically, as events unfold, to help you discover more ideas and make better investment decisions. Pre-register today for early access benefits.

This report was generated with the Equity Risk Regime research workflow from the INFERENTIAL INVESTOR.

Important Disclaimer: This analysis is subject to The Inferential Investor’s Disclaimer. It is for informational and educational purposes only and does not constitute investment advice, a recommendation to buy or sell any security, an offer or solicitation, or a guarantee of future performance. The information is derived from sources believed to be reliable but no representation or warranty is made as to its accuracy or completeness. Scenario descriptions are not forecasts but explorations of the implications of a set of described conditions and are subjetc to risk and uncertainty. Past performance is not indicative of future results. Readers should consult their own advisers before making any investment decision. AI can make mistakes.

All comments or feedback appreciated on this report format.

Andy West

The Inferential Investor