Early Detection of Newly Emerging Market Narratives and the Opportunities that Arise

How to detect new market themes early and connect them to opportunities.

By accessing this article, readers acknowledge the terms of our full legal disclaimer. The information provided herein is for educational and general informational purposes only and does not constitute professional financial or investment advice nor a recommendation to trade in any stock mentioned.

The Importance of Emerging Narratives and Introducing Our New Workflow

In equity markets, some of the biggest winners and losers are shaped by new narratives that begin to change how investors interpret the forward outlook for particular stocks. To see these impacts in action you only have to look at how the “AI eating software / SaaSpocalypse” narrative emerged in 2025 and de-rated the entire software sector globally.

The challenge is that the most important narratives rarely arrive fully formed. They emerge first as fragments across news flow, company commentary, analyst notes, industry reporting, geopolitical developments and specialist market discussion, often before consensus has clearly recognized their significance. For investors, identifying these shifts early matters because these narratives can alter the market’s view of growth durability, margins and valuation multiples well before the full earnings impact is visible in reported results. By the time a theme is universally understood, much of the repricing has often already occurred.

I have introduced a new workflow into the Inferential Investor AI-assisted Research Library which is designed to improve that early detection process by using live web research and AI-assisted synthesis to separate genuinely new narrative formation from stale consensus thinking. This workflow is designed for investors to run every week to scan for new weak or emerging narrative signals that may provide opportunity.

Rather than relying on internal training data to recycle familiar market stories, the workflow strictly imposes a live research regime upon the AI model to scan recent reporting for fresh signals, test whether a theme is truly emerging, and then map the transmission mechanism from the narrative to sectors, industries and individual stocks. AI is especially useful in this context because it can rapidly consolidate dispersed evidence, clarify where the primary and secondary impacts are likely to fall, and draw on historical analogies to frame how similar episodes have propagated through markets in the past. The result is a more structured, forward-looking process that helps investors move from vague macro or thematic noise to a clearer view of which stock groups may benefit, which may be exposed, and why.

In the example below which has been run using the Emerging Narrative Workflow, I have redacted individual stock names as to not provide financial advice. Premium Subscribers can access and simply run the workflow themselves in their chosen model to surface such potential ideas. These represent jumping off points for further, deeper investigation. Too often, I remember thinking a month or two into a new market narrative theme, “I should have thought of that connection”. This workflow is designed to help you get there earlier.

As with any AI research workflow that is broad in scope and involves web RAG, it is up to individual investors to verify information and check sources that are cited. In running this example, I noted stale prices had been included by the model that had clearly been drawn from internal memory rather than live sources (future workflow updates may be able to resolve this as I optimize it). This is typical of the risks of using AI without strictly provided source documents, however does not nullify the value of the workflow in helping resolve uncertain new environments into a clear path for further research and opportunity analysis.

After all, getting to new opportunities early is the name of the game…

Access the Emerging Market Narratives Workflow here

Example Emerging Market Narratives Scanner

Coverage window: February 27, 2026 – March 13, 2026

Geographic scope: Global

Objective: Identify newly emerging narratives from the last 14 days with potential outsized impact on groups of stocks or sectors

Important Note: The following report is drawn from AI news and analyst report scans and should be considered a preliminary and indicative screen of new themes emerging in the market that individually require investor verification and further research. No recommendations are provided relating to individual securities and this report is not to be considered financial advice. Identification of specific and individual risks associated with sectors and securities have not been considered in the scope of this report. Investing in ETFs or stocks connected to rapidly changing new information is inherently risky and includes the risk of loss of capital, that information may be incorrect or incomplete and that the identified theme may prove to be temporary and reverse as conditions evolve. AI can make mistakes. Past performance is not a reliable indicator of future performance.

Executive Summary

Over the past 14 days, the macro and equity market landscape has been violently reordered by three distinct shocks spanning geopolitics, regulatory shifts, and energy supply. The dominant narrative of early 2026—a “Goldilocks” environment defined by imminent rate cuts and unconstrained AI infrastructure spending—is being aggressively tested.

We have identified four new, early-stage narratives emerging from the noise:

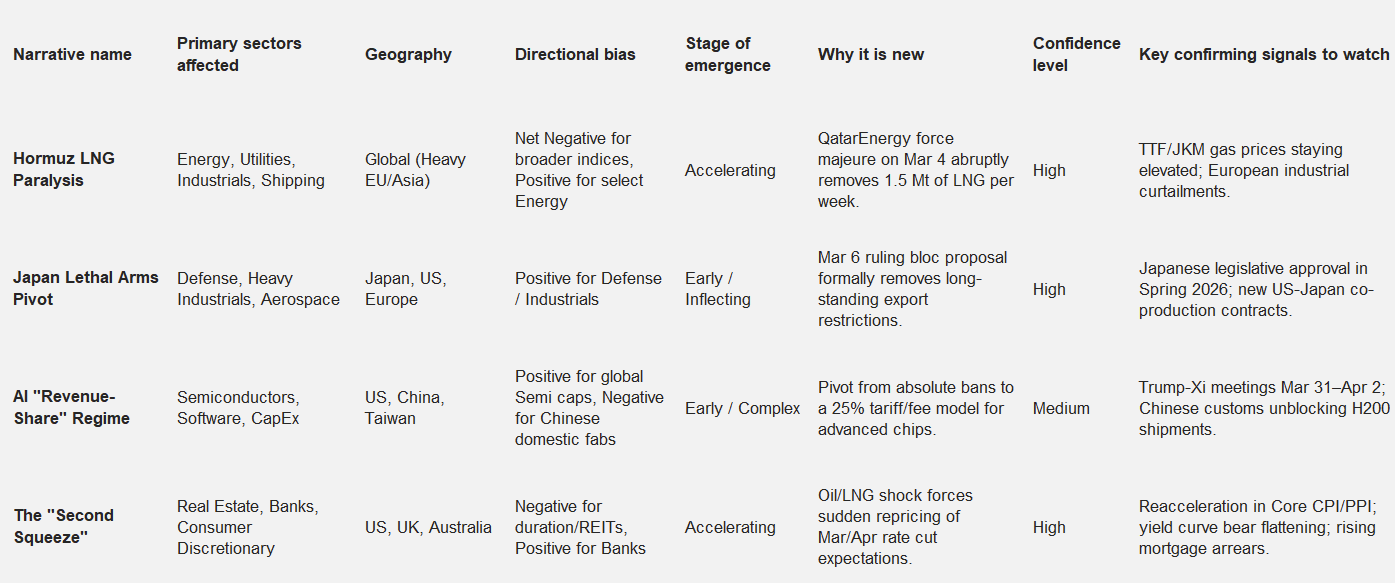

The Hormuz LNG Paralysis: Following a major geopolitical escalation in the Middle East, QatarEnergy declared force majeure on March 4, effectively halting 20% of global LNG shipments. This is not a standard oil disruption; it is a structural supply shock to European and Asian power markets that fundamentally alters the utility and industrial cost curve.

Japan’s Lethal Arms Export Pivot: On March 6, Japan’s ruling coalition proposed a historic revision to its postwar pacifist export laws, clearing the path for lethal arms exports. This integrates Japan’s heavy industrial base directly into the strained Western defense supply chain, unlocking an entirely new global profit pool for domestic manufacturers.

The AI “Revenue-Share” Trade Regime: The US-China “tech war” is quietly pivoting from an absolute embargo to a transactional framework. New US Commerce policies reported in early March allow conditional exports of advanced AI chips (like Nvidia’s H200) subject to a 25% tariff/revenue-share model. This shifts the semiconductor narrative from “total decoupling” to “taxed co-dependence.”

The Central Bank “Second Squeeze”: The immediate inflationary pass-through from the Hormuz closure has shattered Q1 rate-cut pricing. Broker notes across the UK, US, and Australia are suddenly discussing the possibility of a “second squeeze” (and even rate hikes), dramatically altering the outlook for real estate, banks, and long-duration equities.

Narrative Dashboard

Full Narrative Write-Ups

The Hormuz LNG Paralysis

Why this is emerging now

On March 2, 2026, military strikes in the Middle East led to the effective closure of the Strait of Hormuz. On March 4, QatarEnergy—responsible for a fifth of global LNG supply—declared force majeure on all LNG shipments (Gibson Dunn Alert, Mar 4, 2026). This instantly removed roughly 1.5 million tonnes (2.2 bcm) of LNG per week from the global market.

Where the narrative is coming from

The narrative is surfacing rapidly across commodities trading desks and maritime legal circles. Wood Mackenzie published an urgent note (Mar 12, 2026) warning of sustained European power price volatility. Maritime lawyers and insurers are reporting a total withdrawal of war-risk cover for the Gulf, while Asian LNG benchmarks (JKM) and European gas (TTF) spiked over 50% in the immediate aftermath.

Why this is not just an old narrative recycled

Consensus has long priced in “Middle East tension” via a crude oil risk premium. However, the market had not priced in a total, physical halt of Qatari LNG. Europe’s transition away from Russian pipeline gas left it structurally dependent on seaborne LNG. The narrative twist is the transmission into European power markets, where gas still sets the marginal price.

Market transmission mechanism

Supply: 20% of global LNG is trapped.

Pricing: TTF day-ahead prices soared past €55/MWh.

Margins: European industrial margins (chemicals, fertilizers, heavy manufacturing) will compress violently.

Substitution: Forces immediate pivot back to coal/nuclear baseloads where available.

Sector and industry implications

Energy: Massive windfall for non-Middle East LNG exporters (US Gulf Coast, Australia).

Utilities: Margin expansion for unhedged nuclear/coal generators; severe stress for gas-dependent utilities.

Shipping: Freight rates skyrocket as vessels reroute around the Cape of Good Hope.

Industrials: European chemicals and fertilizers face forced production curtailments.

Potential positive stock exposures

[Stock name redacted by publisher]: US - Direct beneficiary of desperate European/Asian spot buying. (Confidence: High)

[Stock name redacted by publisher]: Norway - Europe’s premier pipeline gas alternative. (Confidence: High)

[Stock name redacted by publisher]: Israel/Global - Highly levered to spot freight rates and rerouting congestion. (Confidence: Medium)

[Stock name redacted by publisher]: US - Coal substitution demand spikes as gas becomes prohibitively expensive. (Confidence: Medium)

Potential negative stock exposures

[Stock name redacted by publisher]: Germany - Highly sensitive to European natural gas feedstock prices. (Confidence: High)

[Stock name redacted by publisher]: Japan - Heavy reliance on Qatari LNG; forced into the spot market right before summer demand. (Confidence: High)

Cross-market implications

Severe upward pressure on global coal prices. European carbon allowances (EUAs) may show extreme volatility as utilities switch to dirtier coal generation.

Historical analogies

The 2022 European energy shock following the Nord Stream sabotage, but with the added complexity that global LNG shipping capacity is already stretched.

What would confirm the narrative next

European industrial companies issuing profit warnings or announcing plant idling in late March. Sustained JKM pricing above $20/MMBtu.

What would invalidate it

A rapid diplomatic de-escalation that reopens the Strait of Hormuz within the next 7-10 days, allowing the backlog of Qatari LNG ships to sail.

Bottom line

The LNG shock is the most mispriced tail-risk in the market today; investors must immediately pivot away from European gas-consuming industrials and rotate into US/Australian gas exporters and alternative baseload power generators.

Japan’s Lethal Arms Export Pivot

Why this is emerging now

On March 6, 2026, Japan’s ruling Liberal Democratic Party (LDP) and its coalition partner, the Japan Innovation Party (JIP), formally submitted a proposal to revise the “three principles on defense equipment transfers” to allow the export of lethal weapons (Qazinform/Kyodo, Mar 6, 2026).

Where the narrative is coming from

Japanese political press, Asian geopolitical commentary, and defense trade publications. The move is being framed as an economic and strategic necessity to bolster Japan’s domestic defense industry and integrate with Western allies.

Why this is not just an old narrative recycled

Japan previously eased rules in 2014 and late 2023 (allowing licensed components like Patriot missiles to go to the US). But allowing the direct export of lethal arms developed domestically or jointly is a crossing of the Rubicon. It transforms Japanese heavy industry from a captive domestic supplier into a global defense exporter.

Market transmission mechanism

TAM Expansion: Japanese contractors suddenly have access to the global defense market.

Supply Chain: US and European primes, currently choked by capacity constraints, can deeply integrate Japanese manufacturing into their supply chains.

Valuation: Japanese heavy industrials will see a multiple re-rating as they are increasingly valued as defense contractors rather than low-margin civilian manufacturers.

Sector and industry implications

Defense: Easing of global ammunition and platform shortages.

Industrials (Japan): Major new revenue streams and R&D subsidization from export scale.

Potential positive stock exposures

[Stock name redacted by publisher]: Japan - Japan’s premier defense contractor; prime beneficiary of direct export licenses. (Confidence: High)

[Stock name redacted by publisher]: Japan - Aerospace and submarine capabilities now exportable. (Confidence: High)

[Stock name redacted by publisher]: UK - Partner with Japan in the Global Combat Air Programme (GCAP); export clearance is vital for project economics. (Confidence: High)

Potential negative stock exposures

South Korean Defense eg [Stock name redacted by publisher]: South Korea - Faces formidable new, high-tech competition in the Asian and European arms export markets. (Confidence: Medium)

Cross-market implications

Strengthens the JPY structurally over the medium term if Japan becomes a net exporter of high-value aerospace and defense equipment.

Historical analogies

Germany’s “Zeitenwende” in 2022, which fundamentally re-rated Rheinmetall and Hensoldt as the country abandoned decades of pacifist defense posture.

What would confirm the narrative next

Passage of the revised operational guidelines by the Japanese Diet this Spring, followed by the announcement of a direct lethal arms export contract to a European or Southeast Asian nation.

What would invalidate it

A sudden collapse of the LDP coalition government or massive domestic protests forcing Kishida’s government to abandon the revision.

Bottom line

Japanese heavy industrials are poised for a multi-year structural re-rating as they integrate into the global defense-industrial base; buy the prime contractors before the legislative change is fully formalized.

The AI “Revenue-Share” Trade Regime

Why this is emerging now

In early March 2026, details emerged regarding a structural shift in US export controls on advanced semiconductors. The administration has begun approving conditional sales of Nvidia’s H200 chips to vetted Chinese buyers, utilizing a 25% “surcharge” or revenue-sharing model (Bloomberg/Financial Times, Mar 6-14, 2026). While currently marred by Chinese customs pushback (forcing Nvidia to temporarily halt China H200 production), the policy framework has shifted.

Where the narrative is coming from

Financial Times tech reporting, US Commerce Department statements, and semiconductor supply chain checks in Taiwan and the US.

Why this is not just an old narrative recycled

For years, the consensus was “total decoupling”—a hard technological iron curtain. The revelation that the US is willing to monetize rather than simply block AI compute (trading absolute security for commercial leverage ahead of the Mar 31 Trump-Xi summit) is a profound shift from bans to tariffs.

Market transmission mechanism

Revenue: Allows Western semi-caps to legally tap the Chinese market, albeit at lower volumes and higher margins.

Geopolitics: Lowers the tail-risk of a Chinese kinetic move on Taiwan, as tech co-dependence is partially restored.

CapEx: Shifts the burden to Chinese hyperscalers, who must decide whether to pay a massive premium for US chips or rely on inferior domestic alternatives.

Sector and industry implications

Semiconductors: Reduces the risk of a bifurcated global tech standard.

Chinese Tech: Provides a lifeline for Chinese AI model training (e.g., DeepSeek, Alibaba) if trade negotiations clear customs blockages.

Potential positive stock exposures

[Stock name redacted by publisher]: US - Despite near-term production reshuffling, a legal, tariffed pathway to sell into China removes a massive regulatory overhang. (Confidence: Medium)

[Stock name redacted by publisher]: China - Access to H200s (even at a premium) keeps their cloud and AI infrastructure competitive globally. (Confidence: Medium)

[Stock name redacted by publisher]: Taiwan - Benefits from overall higher global chip volumes if decoupling risks recede. (Confidence: High)

Potential negative stock exposures

[Stock name redacted by publisher]: China - Domestic champions lose their captive monopoly if Chinese tech giants are allowed to buy superior US chips again. (Confidence: High)

Cross-market implications

Favorable for the Chinese Yuan (CNY) and broad emerging market tech indices as the existential threat of total US technology embargoes fades into quantifiable, manageable tariffs.

Historical analogies

The 1980s US-Japan semiconductor trade friction, which eventually settled into managed trade agreements and price floors rather than total market exclusion.

What would confirm the narrative next

The upcoming US-China summit (Mar 31–Apr 2, 2026) producing a formal agreement that unblocks Chinese customs for the H200 in exchange for trade concessions.

What would invalidate it

The US Commerce Department reverting to the “AI diffusion rule” and blanket bans, or China permanently banning the import of the H200 to force domestic reliance.

Bottom line

The market is misinterpreting the near-term noise of Nvidia’s production halt; the structural signal is that the US is moving to a “managed trade” model for AI, which is net-bullish for Western semi-caps and Chinese hyperscalers.

The Central Bank “Second Squeeze”

Why this is emerging now

A sudden stagflationary shock—driven by Brent crude surging toward $120 and the Hormuz LNG shutdown—has completely derailed the January/February “Goldilocks” disinflation narrative. In the second week of March 2026, swap markets aggressively priced out March/April rate cuts for the BoE, Fed, and RBA, with local Australian notes discussing a “second mortgage squeeze” (Morningstar/Australian Stock Report, Mar 9-11, 2026).

Where the narrative is coming from

Fixed income trading desks, macro strategy notes, and regional banking analysis. Analysts highlight that central banks are terrified of repeating the “transitory” mistake of 2021 and will hold or even hike rates into a slowing, energy-shocked economy.

Why this is not just an old narrative recycled

A month ago, the debate was how many cuts we would get in 2026. Now, the narrative has violently violently pivoted to “higher for much longer” and the structural vulnerability of assets that refinanced in 2024/2025 expecting lower terminal rates.

Market transmission mechanism

Yield Curve: Bear flattening as short-term rates stay anchored high while long-term growth expectations fall.

Credit Risk: Rising arrears in consumer credit and commercial real estate as the “expected relief” of 2026 cuts vanishes.

Valuations: High-multiple, long-duration equities (SaaS) and yield-proxies (REITs) face severe multiple compression.

Sector and industry implications

Banks: Short-term NIM expansion, but rapidly escalating credit risk / NPLs.

Real Estate: REITs face a devastating cost-of-capital shock just as a wall of commercial debt matures.

Consumer Discretionary: The “second squeeze” destroys middle-class discretionary spending power (especially in variable-rate mortgage markets like the UK and Australia).

Potential positive stock exposures

[Stock name redacted by publisher]: US - Fortress balance sheet capable of absorbing credit shocks while benefiting from sustained high interest rates. (Confidence: High)

[Stock name redacted by publisher]: US - P&C insurers benefit from higher yields on their massive short-duration float. (Confidence: High)

Potential negative stock exposures

[Stock name redacted by publisher] Australia - Highly levered retail REIT exposed to both higher financing costs and a crushed consumer base. (Confidence: High)

[Stock name redacted by publisher]: US - Industrial REITs, previously viewed as safe havens, will face cap-rate expansion. (Confidence: Medium)

[Stock name redacted by publisher]: UK - Aspirational luxury is highly vulnerable to the UK/European consumer stagflation shock. (Confidence: High)

Cross-market implications

A surging US Dollar (DXY) as a safe haven and high-yielder, crushing emerging market FX. [Commodity name redacted by publisher] breakout above [price level] as a stagflation hedge.

Historical analogies

The 1973 OPEC oil embargo, which forced the Arthur Burns Fed to tighten monetary policy directly into a supply-driven recession, crushing high-multiple “Nifty Fifty” stocks.

What would confirm the narrative next

March CPI/PPI prints across the US and UK showing re-accelerating core services inflation. Central bank forward guidance formally removing “easing bias.”

What would invalidate it

A rapid collapse in oil/gas prices due to peace in the Middle East, allowing central banks to resume their planned easing cycles.

Bottom line

The Q1 equity rally was built on the premise of falling discount rates; with a stagflation shock removing the central bank put, investors must violently rotate out of levered real estate and consumer discretionary into fortress balance sheet financials and energy.

Sector Theme Map

Technology & Semiconductors

The tech sector is bifurcating. The AI Revenue-Share Regime acts as a tailwind for the hardware layer (NVDA, TSM) as geopolitical catastrophic risk is replaced by quantifiable tariffs. However, software and long-duration tech are highly vulnerable to the Central Bank Second Squeeze, as discount rates stay elevated. Expect hardware to aggressively outperform SaaS.

Energy & Utilities

The focal point of global market stress. The Hormuz LNG Paralysis is creating a hyper-local crisis in European and Asian gas markets. This forces a rapid structural pivot: windfalls for US/Australian LNG exporters and desperate substitution into coal and nuclear baseloads. European gas-reliant utilities will see margins destroyed.

Industrials, Geopolitical & Defense

Japan’s Lethal Arms Export Pivot is the defining structural shift here. Global defense supply chains are heavily backlogged; integrating Japan’s high-tech industrial base provides massive relief to Western primes while rerating Japanese industrials. Concurrently, European industrials (chemicals/manufacturing) face existential threats from the LNG shock.

Financials & Real Estate

The Second Squeeze dictates play here. Commercial Real Estate (REITs) were priced for a 2026 bailout via rate cuts; that bailout is cancelled. Regional banks heavily exposed to CRE face severe distress, while mega-cap, diversified banks (JPM) and insurance companies benefit from sustained high yields on the short end of the curve.

Consumer & Retail

Trapped between the Second Squeeze (higher mortgage rates/credit costs) and the Hormuz Paralysis (higher energy/gas costs). Aspirational luxury and general consumer discretionary are uninvestable in Europe and Australia until the stagflation dynamics break.

Live Research Audit

Live web search conducted: Yes

Total number of web searches run: 4

Approximate number of distinct sources reviewed: 18

Coverage window used: February 27, 2026 – March 13, 2026

Geographies covered: US, Europe, UK, Japan, China, Australia, Middle East

Narratives rejected for failing novelty test: - AI replacing software coders (Too old, already consensus throughout 2024/2025).

Indian Pharma Patent Cliff (Lacked broad cross-sector transmission mechanism).

Biotech M&A Boom (Insufficient acute catalyst in the 14-day window; mostly a continuation of late-2025 momentum).

Confirmation that included narratives were validated using live sources from the last 14 days: Yes